Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Authority To Sell Blank TemplateDocument1 pageAuthority To Sell Blank TemplateJaimee Ruth LiganPas encore d'évaluation

- MyExcelSkillsStartDocument1 516 pagesMyExcelSkillsStartvenom_ftwPas encore d'évaluation

- Jonsay vs. Solidbank Corporation (Now MetropolitanBank and Trust Company)Document26 pagesJonsay vs. Solidbank Corporation (Now MetropolitanBank and Trust Company)Vincent OngPas encore d'évaluation

- Gonzales vs. Commission On ElectionsDocument30 pagesGonzales vs. Commission On ElectionsVincent OngPas encore d'évaluation

- Letter Complaint of Merlita B. Fabiana Against Presiding Justice Andres B. Reyes, JR., Et Al.Document13 pagesLetter Complaint of Merlita B. Fabiana Against Presiding Justice Andres B. Reyes, JR., Et Al.Vincent OngPas encore d'évaluation

- Pasco vs. Heirs of Filomena de GuzmanDocument10 pagesPasco vs. Heirs of Filomena de GuzmanVincent OngPas encore d'évaluation

- De Liano vs. Court of AppealsDocument18 pagesDe Liano vs. Court of AppealsVincent Ong100% (1)

- Republic vs. Bisaya Land Transportation Co., Inc.Document25 pagesRepublic vs. Bisaya Land Transportation Co., Inc.Vincent OngPas encore d'évaluation

- Fukuzumi vs. Sanritsu Great International CorporationDocument6 pagesFukuzumi vs. Sanritsu Great International CorporationVincent OngPas encore d'évaluation

- Philippine Ports Authority vs. William GothongDocument5 pagesPhilippine Ports Authority vs. William GothongVincent OngPas encore d'évaluation

- Catmon Sales International Corporation Vs Atty YngsonDocument6 pagesCatmon Sales International Corporation Vs Atty YngsonVincent OngPas encore d'évaluation

- Gagoomal vs. Spouses VillacortaDocument11 pagesGagoomal vs. Spouses VillacortaVincent Ong100% (1)

- Planters Development Bank vs. ChandumalDocument10 pagesPlanters Development Bank vs. ChandumalVincent OngPas encore d'évaluation

- Esso Standard Eastern, Inc. vs. Comm'r. of Internal RevenueDocument8 pagesEsso Standard Eastern, Inc. vs. Comm'r. of Internal RevenueVincent OngPas encore d'évaluation

- Commissioner of Internal Revenue vs. PalancaDocument7 pagesCommissioner of Internal Revenue vs. PalancaVincent OngPas encore d'évaluation

- Gonzales vs. BugaayDocument5 pagesGonzales vs. BugaayVincent OngPas encore d'évaluation

- Kuenzle & Streiff, Inc., vs. The Collector of Internal RevenueDocument7 pagesKuenzle & Streiff, Inc., vs. The Collector of Internal RevenueVincent OngPas encore d'évaluation

- Go Tong Electrical Supply Co., Inc. vs. BPIDocument12 pagesGo Tong Electrical Supply Co., Inc. vs. BPIVincent OngPas encore d'évaluation

- Sps. Pascual Vs First Consolidated Rural BankDocument5 pagesSps. Pascual Vs First Consolidated Rural BankVincent Ong0% (1)

- Penta Pacific Realty Corp Vs Ley Construction and Development CorpDocument15 pagesPenta Pacific Realty Corp Vs Ley Construction and Development CorpVincent OngPas encore d'évaluation

- Umale Vs Canoga Park Development CorpDocument7 pagesUmale Vs Canoga Park Development CorpVincent OngPas encore d'évaluation

- Salenga vs. Court of AppealsDocument24 pagesSalenga vs. Court of AppealsVincent OngPas encore d'évaluation

- 25 - Sps. Nilo and Stella Cha Vs CADocument5 pages25 - Sps. Nilo and Stella Cha Vs CAVincent OngPas encore d'évaluation

- 19 - Development Bank of The Phils. Vs CADocument7 pages19 - Development Bank of The Phils. Vs CAVincent OngPas encore d'évaluation

- Philamcare Health Systems Inc Vs CA and Julita TrinosDocument6 pagesPhilamcare Health Systems Inc Vs CA and Julita TrinosVincent OngPas encore d'évaluation

- Mangubat Vs Morga-SevaDocument11 pagesMangubat Vs Morga-SevaVincent OngPas encore d'évaluation

- Garcia Vs Ferro Chemicals IncDocument16 pagesGarcia Vs Ferro Chemicals IncVincent OngPas encore d'évaluation

- 20 - Virginia Perez Vs CADocument7 pages20 - Virginia Perez Vs CAVincent OngPas encore d'évaluation

- 21 - Malaya Insurance Co. Inc Vs CADocument9 pages21 - Malaya Insurance Co. Inc Vs CAVincent OngPas encore d'évaluation

- Sun Life Assurance Co of Canada Vs CADocument4 pagesSun Life Assurance Co of Canada Vs CAVincent OngPas encore d'évaluation

- Thelma Vda. de Camiling Vs CADocument6 pagesThelma Vda. de Camiling Vs CAVincent OngPas encore d'évaluation

- 15 - Country Bankers Insurance Corp Vs Lianga BayDocument8 pages15 - Country Bankers Insurance Corp Vs Lianga BayVincent OngPas encore d'évaluation

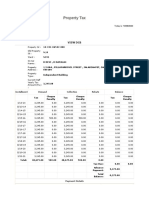

- House Tax ReceiptDocument2 pagesHouse Tax ReceiptAkshaya Raman RamPas encore d'évaluation

- 2011 Pub 4491WDocument208 pages2011 Pub 4491WRefundOhioPas encore d'évaluation

- Certificate of Donation: ABS-CBN Lingkod Kapamilya Foundation, IncDocument2 pagesCertificate of Donation: ABS-CBN Lingkod Kapamilya Foundation, IncGuile Gabriel AlogPas encore d'évaluation

- Cambridge International AS & A Level: Economics 9708/32Document12 pagesCambridge International AS & A Level: Economics 9708/32PRIYANK RAWATPas encore d'évaluation

- Marilou B. Franco San Francisco, Agusan Del Sur: (In Philippine Pesos)Document6 pagesMarilou B. Franco San Francisco, Agusan Del Sur: (In Philippine Pesos)ATRIYO ENTERPRISESPas encore d'évaluation

- BIR Form 2307Document1 pageBIR Form 2307Aizhel Villegas ArcipePas encore d'évaluation

- Transfer Deed Government of PakistanDocument3 pagesTransfer Deed Government of Pakistanapi-3803246Pas encore d'évaluation

- CD - 1. Lorenzo v. PosadasDocument4 pagesCD - 1. Lorenzo v. PosadasCzarina CidPas encore d'évaluation

- Acc 423 Advanced TaxationDocument50 pagesAcc 423 Advanced Taxationkajojo joyPas encore d'évaluation

- Cta Eb CV 02543 D 2023may11 AssDocument11 pagesCta Eb CV 02543 D 2023may11 AssErlinda SantiagoPas encore d'évaluation

- HT2329I005080200Document4 pagesHT2329I005080200Aakash VyshnavPas encore d'évaluation

- DT CTFP 1 - Basic Concepts ExtendedDocument22 pagesDT CTFP 1 - Basic Concepts ExtendedMonalisa BagdePas encore d'évaluation

- Slides - SARSDocument191 pagesSlides - SARSCedric PoolPas encore d'évaluation

- Invoice No. 10002467299 Invoice Date 28.05.2022Document2 pagesInvoice No. 10002467299 Invoice Date 28.05.2022Ishu BansalPas encore d'évaluation

- FFA QA Addendum Presentation HardDocument170 pagesFFA QA Addendum Presentation HardKevinOhlandtPas encore d'évaluation

- Section 194C: TDS On ContractDocument5 pagesSection 194C: TDS On ContractwaghulePas encore d'évaluation

- How Can You Describe The Global Marketplace of A Multinational CompanyDocument16 pagesHow Can You Describe The Global Marketplace of A Multinational CompanytseguPas encore d'évaluation

- 9347 Single CustomsDocument8 pages9347 Single CustomsKalpesh RathodPas encore d'évaluation

- Optional Standard Deduction OSDDocument28 pagesOptional Standard Deduction OSDLes EvangeListaPas encore d'évaluation

- Midterm Exam of Managerial Economics 2022Document4 pagesMidterm Exam of Managerial Economics 2022dayeyoutai779Pas encore d'évaluation

- WeBOC Registration RequirementDocument3 pagesWeBOC Registration RequirementbehindthelinkPas encore d'évaluation

- Taxpayer Bill of RightsDocument1 pageTaxpayer Bill of RightsCyrine CalagosPas encore d'évaluation

- Income Taxation ModuleDocument52 pagesIncome Taxation ModulePercival CelestinoPas encore d'évaluation

- Direct Tax Ca FinalDocument10 pagesDirect Tax Ca FinalGaurav GaurPas encore d'évaluation

- GST Scope Post Release DocumentDocument22 pagesGST Scope Post Release DocumentRajesh KumarPas encore d'évaluation

- 11 Handout 1Document4 pages11 Handout 1Jeffer Jay GubalanePas encore d'évaluation

- Informe de Riesgo JorsunDocument14 pagesInforme de Riesgo JorsunJosé Andrés Carrasco SáezPas encore d'évaluation

- Delish NutrishDocument54 pagesDelish NutrishNael ChiraghPas encore d'évaluation