Vous aimerez peut-être aussi

- Coinbase & IRSDocument14 pagesCoinbase & IRSTechCrunch100% (2)

- Coinbase Order IRSDocument14 pagesCoinbase Order IRSZerohedgePas encore d'évaluation

- Kaseberg V Conaco MIL OrderDocument18 pagesKaseberg V Conaco MIL OrderTHROnlinePas encore d'évaluation

- VL Order Judge Michael Clark - Santa Clara County Superior Court - In re the Marriage of Kamal Hiramanek and Adil Hiramanek Vexatious Litigant Proceeding Santa Clara Superior Court - Presiding Judge Rise Jones PichonDocument11 pagesVL Order Judge Michael Clark - Santa Clara County Superior Court - In re the Marriage of Kamal Hiramanek and Adil Hiramanek Vexatious Litigant Proceeding Santa Clara Superior Court - Presiding Judge Rise Jones PichonCalifornia Judicial Branch News Service - Investigative Reporting Source Material & Story IdeasPas encore d'évaluation

- Harper V Rettig: 21-1316Document16 pagesHarper V Rettig: 21-1316Western CPEPas encore d'évaluation

- San Francisco Et Al v. Sessions Et AlDocument61 pagesSan Francisco Et Al v. Sessions Et AlDoug MataconisPas encore d'évaluation

- Memorandum of LawDocument16 pagesMemorandum of LawGeorge GingoPas encore d'évaluation

- G.R. No. 174629Document15 pagesG.R. No. 174629Julia PoncianoPas encore d'évaluation

- Williams Broadcasting 13Document3 pagesWilliams Broadcasting 13Ethan GatesPas encore d'évaluation

- Herson v. Richmond 1983 MSJDocument18 pagesHerson v. Richmond 1983 MSJNorthern District of California BlogPas encore d'évaluation

- GSIS Vs Court of Appeals G.R. No. 189206 June 8 2011Document3 pagesGSIS Vs Court of Appeals G.R. No. 189206 June 8 2011Nor Alem SampornaPas encore d'évaluation

- Coon Ot Tax Appeals: Second DivisionDocument17 pagesCoon Ot Tax Appeals: Second DivisionLeamieRetalesPas encore d'évaluation

- Hamilton v. Snohomish County, Case No. 18-2-575598-SEADocument17 pagesHamilton v. Snohomish County, Case No. 18-2-575598-SEAchristopher kingPas encore d'évaluation

- Hammer Opinion Denying MTQ - Malibu MediaDocument15 pagesHammer Opinion Denying MTQ - Malibu Mediajoseph bahgatPas encore d'évaluation

- Millennium V Wicked OrderDocument11 pagesMillennium V Wicked OrderTHROnlinePas encore d'évaluation

- Toronto Dominion Bank V Giercke 2021Document9 pagesToronto Dominion Bank V Giercke 2021HenoAlambrePas encore d'évaluation

- National Urban League Oct 1 2020 Order REDocument15 pagesNational Urban League Oct 1 2020 Order RELaw&Crime100% (1)

- Bank of America vs. Philippine Racing Club, G.R. No. 150228, July 20, 2009Document13 pagesBank of America vs. Philippine Racing Club, G.R. No. 150228, July 20, 2009Chris ValenzuelaPas encore d'évaluation

- Saffon FeesDocument16 pagesSaffon FeesfleckaleckaPas encore d'évaluation

- 01.19.2018 Ezor Order Granting MTDDocument17 pages01.19.2018 Ezor Order Granting MTDKrista MarshallPas encore d'évaluation

- G.R. No. 125297 Oh vs. Court of Appeals, 403 SCRA 300 (2003)Document9 pagesG.R. No. 125297 Oh vs. Court of Appeals, 403 SCRA 300 (2003)Shereen AlobinayPas encore d'évaluation

- Gov Uscourts Nysd 551082 194 0Document3 pagesGov Uscourts Nysd 551082 194 0ForkLogPas encore d'évaluation

- REPUBLIC vs. EUGENIODocument17 pagesREPUBLIC vs. EUGENIOBiaPas encore d'évaluation

- Errico v. Pacific Capital Bank ECOA MTDDocument21 pagesErrico v. Pacific Capital Bank ECOA MTDNorthern District of California BlogPas encore d'évaluation

- HARIHAR Files DEMAND To Vacate Judgement, Recall Mandate & Amend Complaint, Following: (1) 2nd SCOTUS Timeline Ext and (2) Discovery of NEW EvidenceDocument26 pagesHARIHAR Files DEMAND To Vacate Judgement, Recall Mandate & Amend Complaint, Following: (1) 2nd SCOTUS Timeline Ext and (2) Discovery of NEW EvidenceMohan HariharPas encore d'évaluation

- Restraining Order in Securities America CaseDocument9 pagesRestraining Order in Securities America CaseDealBookPas encore d'évaluation

- Motion To Stay DiscoveryDocument14 pagesMotion To Stay DiscoveryMMA PayoutPas encore d'évaluation

- Solidbank Corporation v. Spouses TanDocument5 pagesSolidbank Corporation v. Spouses TanLiz KawiPas encore d'évaluation

- Waste Action Project/Buckley Recycle Center Consent DecreeDocument10 pagesWaste Action Project/Buckley Recycle Center Consent DecreeRay StillPas encore d'évaluation

- 5 - Yu Oh v. Court of Appeals (G.R. No. 125297, June 06, 2003)Document14 pages5 - Yu Oh v. Court of Appeals (G.R. No. 125297, June 06, 2003)Jaquelyn VidalPas encore d'évaluation

- Aniel v. Litton Loan Servc Mortgage MTDDocument11 pagesAniel v. Litton Loan Servc Mortgage MTDNorthern District of California BlogPas encore d'évaluation

- BEFORE THE COURT Is Defendant's Motion To Dismiss For Lack ofDocument10 pagesBEFORE THE COURT Is Defendant's Motion To Dismiss For Lack ofKatrina Nadonga JarabejoPas encore d'évaluation

- DFN Post Hearing BriefDocument14 pagesDFN Post Hearing BriefBeth Stoops Jacobson100% (1)

- United States Bankruptcy Court Western District of Washington at TacomaDocument16 pagesUnited States Bankruptcy Court Western District of Washington at Tacomavic broutellePas encore d'évaluation

- Gov Uscourts Cand 407115 10 0Document2 pagesGov Uscourts Cand 407115 10 0prometheusPas encore d'évaluation

- QC:ourt: of Tbe TlbilippinesDocument15 pagesQC:ourt: of Tbe TlbilippinesLey JeryPas encore d'évaluation

- Respondent in Pro PerDocument41 pagesRespondent in Pro PerRebeca MinguraPas encore d'évaluation

- 1 BPI Vs IACDocument10 pages1 BPI Vs IACjoycePas encore d'évaluation

- Sanctions - Lake v. HobbsDocument30 pagesSanctions - Lake v. HobbsJordan ConradsonPas encore d'évaluation

- Williams Broadcasting 19Document2 pagesWilliams Broadcasting 19Ethan GatesPas encore d'évaluation

- Case 8:18-cv-01644-VAP-KES Document 70 Filed 04/09/19 Page 1 of 19 Page ID #:1910Document19 pagesCase 8:18-cv-01644-VAP-KES Document 70 Filed 04/09/19 Page 1 of 19 Page ID #:1910EvieM.WarnerPas encore d'évaluation

- Superior Court of California, County ofDocument11 pagesSuperior Court of California, County ofJohnnyLarsonPas encore d'évaluation

- Federal Deposit Insurance Corporation v. Consolidated Mortgage and Finance Corporation, 805 F.2d 14, 1st Cir. (1986)Document13 pagesFederal Deposit Insurance Corporation v. Consolidated Mortgage and Finance Corporation, 805 F.2d 14, 1st Cir. (1986)Scribd Government DocsPas encore d'évaluation

- Order Granting Motion For Preliminary InjunctionDocument13 pagesOrder Granting Motion For Preliminary InjunctionSon Burnyoaz100% (1)

- District Court Order Denying Stanford International Bank 'S Foreign Liquidators Request For Recognition As A Foreign Main Proceeding Under Chapter 15 of The US Bankruptcy CodeDocument60 pagesDistrict Court Order Denying Stanford International Bank 'S Foreign Liquidators Request For Recognition As A Foreign Main Proceeding Under Chapter 15 of The US Bankruptcy CodeStanford Victims CoalitionPas encore d'évaluation

- Rule 113 Cases Full TextDocument65 pagesRule 113 Cases Full TextJamie VodPas encore d'évaluation

- Rite Aid Store ClosuresDocument29 pagesRite Aid Store ClosuresKhristopher Brooks100% (2)

- Order MSJ 071014Document16 pagesOrder MSJ 071014Nye LavallePas encore d'évaluation

- Castillo v. Nationstar Summ Jud. Order 11.22.2016Document13 pagesCastillo v. Nationstar Summ Jud. Order 11.22.2016DinSFLA100% (1)

- Attorneys For Plaintiffs and The Settlement ClassDocument9 pagesAttorneys For Plaintiffs and The Settlement ClassJian GabatPas encore d'évaluation

- Stern v. Does, 09-01985 DMG) (PLAx) (C.D. Cal. Feb. 10, 2011)Document30 pagesStern v. Does, 09-01985 DMG) (PLAx) (C.D. Cal. Feb. 10, 2011)Venkat BalasubramaniPas encore d'évaluation

- 79Document4 pages79Dr. Jonathan Levy, PhDPas encore d'évaluation

- CD GSIS v. Court of Appeals G.R. No. 189206 June 8 2011Document5 pagesCD GSIS v. Court of Appeals G.R. No. 189206 June 8 2011Dan ChuaPas encore d'évaluation

- Supreme Court Eminent Domain Case 09-381 Denied Without OpinionD'EverandSupreme Court Eminent Domain Case 09-381 Denied Without OpinionPas encore d'évaluation

- The Book of Writs - With Sample Writs of Quo Warranto, Habeas Corpus, Mandamus, Certiorari, and ProhibitionD'EverandThe Book of Writs - With Sample Writs of Quo Warranto, Habeas Corpus, Mandamus, Certiorari, and ProhibitionÉvaluation : 5 sur 5 étoiles5/5 (9)

- Petition for Certiorari Denied Without Opinion: Patent Case 98-1972.D'EverandPetition for Certiorari Denied Without Opinion: Patent Case 98-1972.Pas encore d'évaluation

- Petition for Extraordinary Writ Denied Without Opinion– Patent Case 94-1257D'EverandPetition for Extraordinary Writ Denied Without Opinion– Patent Case 94-1257Pas encore d'évaluation

- California Supreme Court Petition: S173448 – Denied Without OpinionD'EverandCalifornia Supreme Court Petition: S173448 – Denied Without OpinionÉvaluation : 4 sur 5 étoiles4/5 (1)

- U.S. v. Sun Myung Moon 532 F.Supp. 1360 (1982)D'EverandU.S. v. Sun Myung Moon 532 F.Supp. 1360 (1982)Pas encore d'évaluation

- D.E. 1 - FTX Class Action Complaint and Demand For Jury TrialDocument41 pagesD.E. 1 - FTX Class Action Complaint and Demand For Jury Trialjeff_roberts881100% (1)

- Coinbase Regulatory Framework FinalDocument28 pagesCoinbase Regulatory Framework Finaljeff_roberts881Pas encore d'évaluation

- SEC v. Coinbase, Coinbase Answer To ComplaintDocument177 pagesSEC v. Coinbase, Coinbase Answer To Complaintjeff_roberts881100% (1)

- SEC v. Coinbase, Coinbase Pre-Motion Letter - 12 (C) MotionDocument4 pagesSEC v. Coinbase, Coinbase Pre-Motion Letter - 12 (C) Motionjeff_roberts881Pas encore d'évaluation

- FINAL - Tornado Cash ComplaintDocument20 pagesFINAL - Tornado Cash Complaintjeff_roberts881Pas encore d'évaluation

- BLDF Defense Filing - 4.26.23Document39 pagesBLDF Defense Filing - 4.26.23jeff_roberts881Pas encore d'évaluation

- Ripple V SEC ProceduralDocument2 pagesRipple V SEC Proceduraljeff_roberts881Pas encore d'évaluation

- Coinbase Class ActionDocument26 pagesCoinbase Class Actionjeff_roberts881100% (1)

- Harris Timothy Mckimmy Opensea: I. (A) PlaintiffsDocument2 pagesHarris Timothy Mckimmy Opensea: I. (A) Plaintiffsjeff_roberts881Pas encore d'évaluation

- Coinbase MurderDocument7 pagesCoinbase Murderjeff_roberts881Pas encore d'évaluation

- Preliminary Statement To Ripple Answer 1.27.20Document8 pagesPreliminary Statement To Ripple Answer 1.27.20jeff_roberts881Pas encore d'évaluation

- 2019-09-09 Filed Opinion (DCKT)Document38 pages2019-09-09 Filed Opinion (DCKT)jeff_roberts881Pas encore d'évaluation

- Silk Road OrderDocument3 pagesSilk Road Orderjeff_roberts881Pas encore d'évaluation

- Binance ComplaintDocument12 pagesBinance Complaintjeff_roberts881Pas encore d'évaluation

- FB Biometrics FilingDocument74 pagesFB Biometrics Filingjeff_roberts881Pas encore d'évaluation

- Jarrett - DRAFT Complaint 05-18-2021Document8 pagesJarrett - DRAFT Complaint 05-18-2021jeff_roberts881Pas encore d'évaluation

- FOIA LetterDocument6 pagesFOIA Letterjeff_roberts881100% (3)

- Defendants' Motion To DismissDocument37 pagesDefendants' Motion To Dismissjeff_roberts881100% (4)

- ECF 1 - Complaint - 20-Cv-2747Document22 pagesECF 1 - Complaint - 20-Cv-2747jeff_roberts881Pas encore d'évaluation

- FB Class ActionDocument57 pagesFB Class Actionjeff_roberts881100% (1)

- 11-7-18 Letter To Judge Irizarry Requesting Pre-Motion Conference (Filed) (00168166xDE802)Document3 pages11-7-18 Letter To Judge Irizarry Requesting Pre-Motion Conference (Filed) (00168166xDE802)jeff_roberts881Pas encore d'évaluation

- Coinbase - Order Denying Mot To Compel, Mot To Dismiss in Part - 8!6!19Document8 pagesCoinbase - Order Denying Mot To Compel, Mot To Dismiss in Part - 8!6!19jeff_roberts881Pas encore d'évaluation

- Ripple CounterclaimDocument41 pagesRipple Counterclaimjeff_roberts881Pas encore d'évaluation

- Ripple XRP ContractDocument9 pagesRipple XRP Contractjeff_roberts881Pas encore d'évaluation

- Manafort IndictmentDocument31 pagesManafort IndictmentKatie Pavlich100% (5)

- Tax Cuts and Jobs Act - Full TextDocument429 pagesTax Cuts and Jobs Act - Full TextWJ Editorial Staff0% (1)

- Coinbase Summons DetailsDocument10 pagesCoinbase Summons Detailsjeff_roberts881Pas encore d'évaluation

- Shutterfly RulingDocument19 pagesShutterfly Rulingjeff_roberts881Pas encore d'évaluation

- Palin V NY Times - Opinion and Order Dismissing LawsuitDocument26 pagesPalin V NY Times - Opinion and Order Dismissing LawsuitLegal InsurrectionPas encore d'évaluation

- Module23 Version 2013Document80 pagesModule23 Version 2013Jed DíazPas encore d'évaluation

- BKash ProfileDocument10 pagesBKash ProfileAshik Md Siam100% (1)

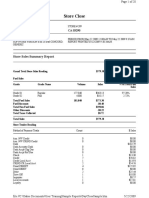

- Store Close: Store Sales Summary ReportDocument20 pagesStore Close: Store Sales Summary ReportJimmyPas encore d'évaluation

- 1z0-506 Questions and Answers HTTP WWW - Testsnow.net TXT 1 1288 14182.HTMLDocument102 pages1z0-506 Questions and Answers HTTP WWW - Testsnow.net TXT 1 1288 14182.HTMLmurali0% (1)

- Alcatel-Lucent: Marketing The Cell Phone As A Mobile Wallet (A)Document25 pagesAlcatel-Lucent: Marketing The Cell Phone As A Mobile Wallet (A)Rahul GargPas encore d'évaluation

- Charlene E Honeywell Financial Disclosure Report For Honeywell, Charlene EDocument8 pagesCharlene E Honeywell Financial Disclosure Report For Honeywell, Charlene EJudicial Watch, Inc.Pas encore d'évaluation

- 2017 Chevrolet Cruze Quote PDFDocument1 page2017 Chevrolet Cruze Quote PDFEvelynPas encore d'évaluation

- Wells Fargo Advisors Premium Rewards Visa Signature CardDocument13 pagesWells Fargo Advisors Premium Rewards Visa Signature CardRalph YoungPas encore d'évaluation

- Compound Property Management, Et Al. v. BUild Realty, Et Al. - ComplaintDocument98 pagesCompound Property Management, Et Al. v. BUild Realty, Et Al. - ComplaintFinney Law Firm, LLCPas encore d'évaluation

- Sample Forensic Audit 26045678Document15 pagesSample Forensic Audit 26045678KNOWLEDGE SOURCEPas encore d'évaluation

- Module-3-Investment-Properties CorrectionDocument18 pagesModule-3-Investment-Properties CorrectionLoven BoadoPas encore d'évaluation

- Lesson 1 - Handout 1 - Fundamentals of AccountingDocument6 pagesLesson 1 - Handout 1 - Fundamentals of AccountingccgomezPas encore d'évaluation

- V13 Manual 1.0Document336 pagesV13 Manual 1.0lp456Pas encore d'évaluation

- HRF - Design Document - V2.0Document33 pagesHRF - Design Document - V2.0AbhilashMadalaPas encore d'évaluation

- Discussion Questions: Hac311 - Tutorial Solutions Chapter 4: Accounting For RevenueDocument7 pagesDiscussion Questions: Hac311 - Tutorial Solutions Chapter 4: Accounting For RevenueAbdulaziz BsebsuPas encore d'évaluation

- Card Statement 2013 7Document2 pagesCard Statement 2013 72005monicaPas encore d'évaluation

- Chapter 15 Business Combinations - Part 2Document10 pagesChapter 15 Business Combinations - Part 2Erwin Labayog Medina100% (2)

- Types of Foreign Exchange MarketsDocument7 pagesTypes of Foreign Exchange MarketsLalit KarkiPas encore d'évaluation

- Jun-10, Dec-10, Jun-11, Dec 11Document64 pagesJun-10, Dec-10, Jun-11, Dec 11Celena Daiton83% (6)

- Prudential Bank vs. NLRCDocument7 pagesPrudential Bank vs. NLRCElla CanuelPas encore d'évaluation

- 1 Intermediate Accounting IFRS 3rd Edition-554-569Document16 pages1 Intermediate Accounting IFRS 3rd Edition-554-569Khofifah SalmahPas encore d'évaluation

- Managerial Finance Reviewer (Prelims)Document4 pagesManagerial Finance Reviewer (Prelims)Kendall JennerPas encore d'évaluation

- 2.shivananda Flyover - Tender Doc - Tec PDFDocument78 pages2.shivananda Flyover - Tender Doc - Tec PDFBirat PanthiPas encore d'évaluation

- Submitted By: Submitted To: TopicDocument4 pagesSubmitted By: Submitted To: TopicNavsPas encore d'évaluation

- LC Draft - Vikohasan - Hansung Indo - 5X40FCL - Ef-079 2020Document3 pagesLC Draft - Vikohasan - Hansung Indo - 5X40FCL - Ef-079 2020Khaerul FazriPas encore d'évaluation

- 35 Common Banking Terms Rates - Asked in Bank PO Interview (With Meaning Definitions)Document5 pages35 Common Banking Terms Rates - Asked in Bank PO Interview (With Meaning Definitions)Kalpesh BhagnePas encore d'évaluation

- Myconstant Token: TechnologyDocument4 pagesMyconstant Token: TechnologyIvan RuizPas encore d'évaluation

- Electronic Payment System (EPS)Document37 pagesElectronic Payment System (EPS)Jivika Patil100% (1)

- ICST Tallyerp9Document141 pagesICST Tallyerp9Ashish Salunkhe100% (1)

- Lease Financing: Learning OutcomesDocument31 pagesLease Financing: Learning Outcomesravi sharma100% (1)