Vous aimerez peut-être aussi

- "Debt: The First 5000 Years" by David Graeber (2009)Document9 pages"Debt: The First 5000 Years" by David Graeber (2009)recycled mindsPas encore d'évaluation

- Manners, Customs, and Dress During the Middle Ages and During the Renaissance PeriodD'EverandManners, Customs, and Dress During the Middle Ages and During the Renaissance PeriodPas encore d'évaluation

- DAVID GRAEBER - Debt, The First Five Thousand YearsDocument9 pagesDAVID GRAEBER - Debt, The First Five Thousand YearsFluckedUp ThingsPas encore d'évaluation

- What Is Debt - Interview With David GraeberDocument14 pagesWhat Is Debt - Interview With David GraeberOccupyEconomicsPas encore d'évaluation

- An Essay in the History of the Radical Sensibility in AmericaD'EverandAn Essay in the History of the Radical Sensibility in AmericaPas encore d'évaluation

- (#) Caffentzis, George - Debt and Money (The Commoner)Document4 pages(#) Caffentzis, George - Debt and Money (The Commoner)Guacamole Bamako ShivaPas encore d'évaluation

- Frenzied Finance Vol. 1: The Crime of AmalgamatedD'EverandFrenzied Finance Vol. 1: The Crime of AmalgamatedPas encore d'évaluation

- Abc123 NWO 101 NWO For DumbiesDocument81 pagesAbc123 NWO 101 NWO For Dumbiesjeromebill7718Pas encore d'évaluation

- Money Chapter ColorDocument15 pagesMoney Chapter Colorsonel_17Pas encore d'évaluation

- Sand Berg Nick Blueprint For A Prison PlanetDocument26 pagesSand Berg Nick Blueprint For A Prison PlanetlectoraavidaPas encore d'évaluation

- Cloud Theory of EconomicsDocument7 pagesCloud Theory of EconomicsMatthew100% (1)

- Private: 1. Is Capitalism Compatible With Christianity? Capitalism Is An Economic System Characterized byDocument4 pagesPrivate: 1. Is Capitalism Compatible With Christianity? Capitalism Is An Economic System Characterized byGlaiza Cabahug ImbuidoPas encore d'évaluation

- Of Bondage: Debt, Property, and Personhood in Early Modern EnglandD'EverandOf Bondage: Debt, Property, and Personhood in Early Modern EnglandÉvaluation : 5 sur 5 étoiles5/5 (1)

- Mixed Sentiments - PT 3 - of The Myth of CapitalDocument16 pagesMixed Sentiments - PT 3 - of The Myth of CapitalJ CooperPas encore d'évaluation

- Us Treasury Speech Dec 4 2003Document8 pagesUs Treasury Speech Dec 4 2003Will CrossPas encore d'évaluation

- Justice at Salem Reexamining The Witch Trials!!!!Document140 pagesJustice at Salem Reexamining The Witch Trials!!!!miarym1980Pas encore d'évaluation

- Discuss The Nature and Extent of Slavery As An Institution in Greco-Roman SocietyDocument4 pagesDiscuss The Nature and Extent of Slavery As An Institution in Greco-Roman SocietySouravPas encore d'évaluation

- Schwartz Misplaced-Ideas PDFDocument19 pagesSchwartz Misplaced-Ideas PDFCamila BatistaPas encore d'évaluation

- Fay Too Much Government Too Much TaxationDocument439 pagesFay Too Much Government Too Much TaxationWade SperryPas encore d'évaluation

- Article 3107 Additional Issues For The International Court of Justice Blood Money 10 Commodity RiggingDocument4 pagesArticle 3107 Additional Issues For The International Court of Justice Blood Money 10 Commodity RiggingJeff LouisPas encore d'évaluation

- Coughlin - Money - Questions and Answers (1971)Document181 pagesCoughlin - Money - Questions and Answers (1971)AdyRm100% (1)

- A New Order of the Ages: A Metaphysical Blueprint of Reality and an Exposé on Powerful Reptilian/Aryan Bloodlines Volume 2D'EverandA New Order of the Ages: A Metaphysical Blueprint of Reality and an Exposé on Powerful Reptilian/Aryan Bloodlines Volume 2Pas encore d'évaluation

- Ponasanje Obicaji I Odeca Kroz Srednji VekDocument418 pagesPonasanje Obicaji I Odeca Kroz Srednji Vekkalganov100% (1)

- ConspiracyofcentralbankingDocument56 pagesConspiracyofcentralbankingjoe chouinard100% (2)

- Conspiracy - of - Central - Banks - Rev2 - Gregory RichfordDocument37 pagesConspiracy - of - Central - Banks - Rev2 - Gregory RichfordShurhand FPPas encore d'évaluation

- The State - Its Historic Role: With an Excerpt from Comrade Kropotkin by Victor RobinsonD'EverandThe State - Its Historic Role: With an Excerpt from Comrade Kropotkin by Victor RobinsonÉvaluation : 5 sur 5 étoiles5/5 (1)

- Anthro FinalDocument4 pagesAnthro Finalapi-313683531Pas encore d'évaluation

- The rise, progress, and phases of human slavery: How it came into the world and how it shall be made to go outD'EverandThe rise, progress, and phases of human slavery: How it came into the world and how it shall be made to go outPas encore d'évaluation

- Intro Universal EconomicsDocument7 pagesIntro Universal Economicsagonza70Pas encore d'évaluation

- Lecture 2. Choice, Scarcity, and Ex-Change: T T - C ' N EDocument6 pagesLecture 2. Choice, Scarcity, and Ex-Change: T T - C ' N ErijderunnerPas encore d'évaluation

- Money Is Proof That Magick WorksDocument4 pagesMoney Is Proof That Magick WorksKali23YugaPas encore d'évaluation

- Validity of AFV 2Document24 pagesValidity of AFV 2csandmPas encore d'évaluation

- The Social Life of Cash Payment': Money, Markets, and The Mutualities of PovertyDocument26 pagesThe Social Life of Cash Payment': Money, Markets, and The Mutualities of PovertyVanguar DolPas encore d'évaluation

- CapitalDocument16 pagesCapitalVinicius SiqueiraPas encore d'évaluation

- Max Primitive Accumulation - UnknownDocument8 pagesMax Primitive Accumulation - Unknownハイロ ナルバエスPas encore d'évaluation

- The Unpopular Review, Volume II Number 3 by VariousDocument109 pagesThe Unpopular Review, Volume II Number 3 by VariousGutenberg.orgPas encore d'évaluation

- Michael J. Hudson - The Collapse of Antiquity - Greece and Rome As Civilization's Oligarchic Turning Point (2023) - Islet (2023)Document481 pagesMichael J. Hudson - The Collapse of Antiquity - Greece and Rome As Civilization's Oligarchic Turning Point (2023) - Islet (2023)edojidaiPas encore d'évaluation

- Cyril Smith - Marx at The MillenniumDocument28 pagesCyril Smith - Marx at The MillenniumMarijan KraljevićPas encore d'évaluation

- All Work and No Pay - Paul HeinDocument48 pagesAll Work and No Pay - Paul HeinJeffrey ChangPas encore d'évaluation

- Debt and The Cyclical RiseDocument7 pagesDebt and The Cyclical RiseKatty UrrutiaPas encore d'évaluation

- Who Is Claiming My TitleDocument10 pagesWho Is Claiming My TitleMichael Jones100% (1)

- Bahan 12Document11 pagesBahan 12yosafat panjiPas encore d'évaluation

- Jacques Ranciere - Hatred of The Poor - Politics or The Lost ShepherdDocument17 pagesJacques Ranciere - Hatred of The Poor - Politics or The Lost ShepherdEugeneLangPas encore d'évaluation

- Rachael Sotos Arendtian Grounds For Graeber's Debt LiberationDocument18 pagesRachael Sotos Arendtian Grounds For Graeber's Debt LiberationRachael SotosPas encore d'évaluation

- Are We Rome PDFDocument12 pagesAre We Rome PDFJoe Fishpaw100% (1)

- Comparative Analysis On Non Performing Assets of Private and Public Sector BanksDocument106 pagesComparative Analysis On Non Performing Assets of Private and Public Sector BanksNeerajPas encore d'évaluation

- Differences Between Islamic BanksDocument4 pagesDifferences Between Islamic BanksFatima AliPas encore d'évaluation

- The State of Domestic Commerce in Pakistan Study 9 - Real Estate in PakistanDocument75 pagesThe State of Domestic Commerce in Pakistan Study 9 - Real Estate in PakistanInnovative Development Strategies (Pvt.) LtdPas encore d'évaluation

- Compound InterestDocument4 pagesCompound InterestMaria JocosaPas encore d'évaluation

- Lawful Rebellion St. Albans. - Taking Control of Your BC TrustDocument6 pagesLawful Rebellion St. Albans. - Taking Control of Your BC TrustHenoAlambre100% (8)

- EMV OverviewDocument51 pagesEMV OverviewManish ChofflaPas encore d'évaluation

- Property Amount: Compute For The Gross Estate of Each Decedent BelowDocument2 pagesProperty Amount: Compute For The Gross Estate of Each Decedent Belowjarlen cosasPas encore d'évaluation

- Electricity Bill-35Document1 pageElectricity Bill-35geswanthuppalPas encore d'évaluation

- Banks and Other Financial IntermediariesDocument3 pagesBanks and Other Financial IntermediariesMary Elleonice Franchette QuiambaoPas encore d'évaluation

- World Bank GlossaryDocument435 pagesWorld Bank Glossarydon_isauroPas encore d'évaluation

- Alternate PetaDocument2 pagesAlternate PetaAngel Ann AgaoPas encore d'évaluation

- Presented By:-Sumit Singal MBA-I (3129)Document34 pagesPresented By:-Sumit Singal MBA-I (3129)Inderpreet SinghPas encore d'évaluation

- Debt Securities: by Lee M. Dunham, PHD, Cfa, and Vijay Singal, PHD, CfaDocument25 pagesDebt Securities: by Lee M. Dunham, PHD, Cfa, and Vijay Singal, PHD, CfaDouglas ZimunyaPas encore d'évaluation

- Answers To Chapter 27 and 28 CasesDocument4 pagesAnswers To Chapter 27 and 28 CasesVic RabayaPas encore d'évaluation

- Civ - Zuniga Notes - CreditDocument175 pagesCiv - Zuniga Notes - CreditLirio IringanPas encore d'évaluation

- Week 05 - Compendium V - Factoring & Forfaiting v3Document16 pagesWeek 05 - Compendium V - Factoring & Forfaiting v3ximenaPas encore d'évaluation

- Jalandhar Amritsar PDFDocument120 pagesJalandhar Amritsar PDFBhagyashreePas encore d'évaluation

- Legal Aspects: Canara Bank Officers' AssociationDocument20 pagesLegal Aspects: Canara Bank Officers' Associationmail2me.preet1801Pas encore d'évaluation

- Real Property LawDocument22 pagesReal Property LawgjkmgjkgjgPas encore d'évaluation

- Investors Exchange Investment FundDocument53 pagesInvestors Exchange Investment FundOlivierPas encore d'évaluation

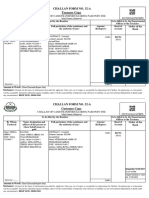

- Challan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheDocument1 pageChallan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into Theآرنولڈ دا فینPas encore d'évaluation

- Forensic Psychology HypnosisDocument3 pagesForensic Psychology HypnosisJhai Jhai DumsyyPas encore d'évaluation

- Financial Ratio Analysis of Bank Performance PDFDocument24 pagesFinancial Ratio Analysis of Bank Performance PDFRatnesh Singh100% (1)

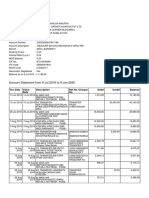

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaePas encore d'évaluation

- Islamic Commercial BankingDocument26 pagesIslamic Commercial BankingjmfaleelPas encore d'évaluation

- Saptg ReportDocument3 pagesSaptg ReportThabo MoalusiPas encore d'évaluation

- IDBI Federal Life InsuranceDocument15 pagesIDBI Federal Life InsuranceAiswarya Johny RCBSPas encore d'évaluation

- RD011 ReceivablesDocument7 pagesRD011 ReceivablesAnusha ReddyPas encore d'évaluation

- Valuation 1Document29 pagesValuation 1Rohan SaxenaPas encore d'évaluation