Vous aimerez peut-être aussi

- Transportation Law Case DigestsDocument9 pagesTransportation Law Case DigestsScents GalorePas encore d'évaluation

- Transportation Law Case Digests and SynthesisDocument10 pagesTransportation Law Case Digests and SynthesisDessa ReyesPas encore d'évaluation

- 1 Case Digests PartnershipDocument5 pages1 Case Digests PartnershipAndrew Mercado NavarretePas encore d'évaluation

- III Theories That Justify Application of Foreign LawDocument45 pagesIII Theories That Justify Application of Foreign Lawjappy27Pas encore d'évaluation

- Pascual Vs Members of TRAMODocument1 pagePascual Vs Members of TRAMOJoshua Erik MadriaPas encore d'évaluation

- WersdfDocument2 pagesWersdfJoan PaynorPas encore d'évaluation

- G.R. No. 210987Document2 pagesG.R. No. 210987Earl Andre PerezPas encore d'évaluation

- Trust ReceiptsDocument23 pagesTrust ReceiptskarenkierPas encore d'évaluation

- 67 Lizarraga v. Abada DIMLADocument2 pages67 Lizarraga v. Abada DIMLAAlfonso DimlaPas encore d'évaluation

- Confidence and Trust.: Law On PartnershipsDocument8 pagesConfidence and Trust.: Law On PartnershipsDwight BlezaPas encore d'évaluation

- Transportation Law PDFDocument24 pagesTransportation Law PDFMuli MJPas encore d'évaluation

- RA 9829 Pre Need CodeDocument23 pagesRA 9829 Pre Need CodeAicing Namingit-VelascoPas encore d'évaluation

- Partnership Case DigestDocument7 pagesPartnership Case DigestMaria Fei Del MundoPas encore d'évaluation

- CHPT 3 GtranspoDocument15 pagesCHPT 3 GtranspoGIGI KHOPas encore d'évaluation

- 32 Serafica Vs Treasurer of Ormoc FULLDocument4 pages32 Serafica Vs Treasurer of Ormoc FULLQueenie Hadiyah Diampuan SaripPas encore d'évaluation

- Nego - Bar 2007-2013Document9 pagesNego - Bar 2007-2013yukibambam_28Pas encore d'évaluation

- Phil Guaranty v. CIRDocument2 pagesPhil Guaranty v. CIR8111 aaa 1118Pas encore d'évaluation

- Lim V Phil Fishing Gear G.R. No. 136448Document1 pageLim V Phil Fishing Gear G.R. No. 136448Anonymous zIDJz7Pas encore d'évaluation

- Caballero V Deiperine DigestDocument5 pagesCaballero V Deiperine DigestJJ CoolPas encore d'évaluation

- Insurance Code: P.D. 612 R.A. 10607 Atty. Jobert O. Rillera, CPA, REB, READocument85 pagesInsurance Code: P.D. 612 R.A. 10607 Atty. Jobert O. Rillera, CPA, REB, REAChing ApostolPas encore d'évaluation

- Case Digest2Document14 pagesCase Digest2Mar Darby ParaydayPas encore d'évaluation

- 02 Manila Steamship Co v. AbdulhamanDocument2 pages02 Manila Steamship Co v. AbdulhamanMark Anthony Javellana SicadPas encore d'évaluation

- Case Digest For Transportation LawDocument2 pagesCase Digest For Transportation LawjaychrisPas encore d'évaluation

- Taxation Law 1 CasesDocument4 pagesTaxation Law 1 CasesAna RobinPas encore d'évaluation

- 1code of CommerceDocument5 pages1code of CommerceTwinklePas encore d'évaluation

- Docu 1 - Lozana vs. Depakabibo Et.Document16 pagesDocu 1 - Lozana vs. Depakabibo Et.KaiserPas encore d'évaluation

- Metal Forming Corp. v. Office of The20181026-5466-122hfzhDocument6 pagesMetal Forming Corp. v. Office of The20181026-5466-122hfzhellePas encore d'évaluation

- 1786 - Moran, Jr. vs. Court of Appeals, L-59956, October 31, 1984 - DIGESTDocument2 pages1786 - Moran, Jr. vs. Court of Appeals, L-59956, October 31, 1984 - DIGESTI took her to my penthouse and i freaked itPas encore d'évaluation

- Transportation Law CasesDocument10 pagesTransportation Law CasesJepski ScopePas encore d'évaluation

- Interpretation: Insurance Law Midterms Reviewer Sunny & Chinita NotesDocument33 pagesInterpretation: Insurance Law Midterms Reviewer Sunny & Chinita NotesHezekiah JoshuaPas encore d'évaluation

- Case Digest - TranspoDocument4 pagesCase Digest - TranspoJerik SolasPas encore d'évaluation

- Partnership Case DigestsDocument7 pagesPartnership Case DigestsRamon T. Conducto IIPas encore d'évaluation

- 11) CIR V American Airlines 180 SCRA 274Document1 page11) CIR V American Airlines 180 SCRA 274gel94Pas encore d'évaluation

- Obillos, Jr. vs. Commissioner of Internal Revenue 139 SCRA 436, October 29, 1985Document1 pageObillos, Jr. vs. Commissioner of Internal Revenue 139 SCRA 436, October 29, 1985Clarissa Sawali0% (1)

- Cover NotesDocument3 pagesCover NotesNIKITA KABRA0% (1)

- R.A. 8791 GENERAL BANKING LAW of 2000 - Law, Politics, and Philosophy (Recovered)Document23 pagesR.A. 8791 GENERAL BANKING LAW of 2000 - Law, Politics, and Philosophy (Recovered)Michael VillalonPas encore d'évaluation

- Presumption of Negligence Pestano vs. Sumayang FactsDocument2 pagesPresumption of Negligence Pestano vs. Sumayang FactsJayPas encore d'évaluation

- 14d G.R. No. L-18330 July 31, 1963 de Borja Vs GellaDocument2 pages14d G.R. No. L-18330 July 31, 1963 de Borja Vs GellarodolfoverdidajrPas encore d'évaluation

- Tacao Vs CA Partnership Case #3Document6 pagesTacao Vs CA Partnership Case #3Jhudith De Julio BuhayPas encore d'évaluation

- Cases BankingDocument52 pagesCases BankingDane Pauline AdoraPas encore d'évaluation

- Donor'S Tax Compilation of Case DigestDocument8 pagesDonor'S Tax Compilation of Case DigestmarydalemPas encore d'évaluation

- G.R. No. 174156 FIlcar Transport Vs Espinas Registered OwnerDocument13 pagesG.R. No. 174156 FIlcar Transport Vs Espinas Registered OwnerChatPas encore d'évaluation

- Medicard vs. CIRDocument6 pagesMedicard vs. CIRYodh Jamin OngPas encore d'évaluation

- Busorg1 DigestDocument5 pagesBusorg1 DigestOwie JoeyPas encore d'évaluation

- Garcia Vs Hongkong Fire and Marine InsuranceDocument2 pagesGarcia Vs Hongkong Fire and Marine InsurancejezzahPas encore d'évaluation

- Agency - EDocument25 pagesAgency - EvalkyriorPas encore d'évaluation

- Bascos v. CaDocument4 pagesBascos v. CaMay ChanPas encore d'évaluation

- Articles of PartnershipDocument4 pagesArticles of PartnershipLady BellePas encore d'évaluation

- Domingo vs. Garlitos (8 SCRA 443, G.R. No. L-18994, June 29, 1963)Document2 pagesDomingo vs. Garlitos (8 SCRA 443, G.R. No. L-18994, June 29, 1963)Kent UgaldePas encore d'évaluation

- China Banking Corp Vs CADocument19 pagesChina Banking Corp Vs CAChristelle Ayn BaldosPas encore d'évaluation

- ME Holding Corp vs. CADocument2 pagesME Holding Corp vs. CAJeremae Ann CeriacoPas encore d'évaluation

- Succession 2010Document81 pagesSuccession 2010hotjurist100% (1)

- Agency ReviewerDocument71 pagesAgency ReviewerMarvi BlaisePas encore d'évaluation

- Affidavit of Loss SampleDocument1 pageAffidavit of Loss SampleJayheartDumapayTumbagaPas encore d'évaluation

- Navarro vs. Court of Appeals 222 SCRA 675, May 27, 1993Document7 pagesNavarro vs. Court of Appeals 222 SCRA 675, May 27, 1993Jane BandojaPas encore d'évaluation

- Transportation Law Case Digests-FRANCISCODocument15 pagesTransportation Law Case Digests-FRANCISCOZesyl Avigail FranciscoPas encore d'évaluation

- Pascual vs. Commissioner of Internal RevenueDocument6 pagesPascual vs. Commissioner of Internal RevenueAngelReaPas encore d'évaluation

- Pascual Vs CirDocument6 pagesPascual Vs CirReth GuevarraPas encore d'évaluation

- Pascual V Cir DigestDocument1 pagePascual V Cir DigestDani Lynne100% (4)

- Pascual V CIRDocument4 pagesPascual V CIRFlorence UdaPas encore d'évaluation

- Scra 2014Document3 pagesScra 2014Czara DyPas encore d'évaluation

- Marie Ivonne F. Reyes: Pasig Catholic SchoolDocument1 pageMarie Ivonne F. Reyes: Pasig Catholic SchoolCzara DyPas encore d'évaluation

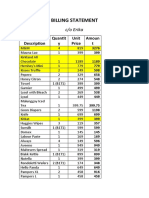

- S&R - Billing StatementDocument4 pagesS&R - Billing StatementCzara DyPas encore d'évaluation

- Castillo vs. RepublicDocument2 pagesCastillo vs. RepublicCzara DyPas encore d'évaluation

- Barcelote Vs - RepublicDocument2 pagesBarcelote Vs - RepublicCzara DyPas encore d'évaluation

- Banking Mon 7718Document2 pagesBanking Mon 7718Czara DyPas encore d'évaluation

- Corpo Notes 2018 PrelimsDocument14 pagesCorpo Notes 2018 PrelimsCzara DyPas encore d'évaluation

- Institution of Heirs. It Will Not Result To IntestacyDocument9 pagesInstitution of Heirs. It Will Not Result To IntestacyCzara DyPas encore d'évaluation

- Policarpio Vs Active BankDocument2 pagesPolicarpio Vs Active BankCzara DyPas encore d'évaluation

- G.R. No. L-48955, June 30, 1987)Document8 pagesG.R. No. L-48955, June 30, 1987)Czara DyPas encore d'évaluation

- Sunio v. NLRCDocument3 pagesSunio v. NLRCCzara DyPas encore d'évaluation

- Nil Cases FinalsDocument37 pagesNil Cases FinalsCzara DyPas encore d'évaluation

- TORTS Page 2 Cases SyllabusDocument77 pagesTORTS Page 2 Cases SyllabusCzara DyPas encore d'évaluation

- Annum From July 1, 2013 Until Full PaymentDocument1 pageAnnum From July 1, 2013 Until Full PaymentCzara DyPas encore d'évaluation

- Jimenez vs. FranciscoDocument1 pageJimenez vs. FranciscoCzara DyPas encore d'évaluation

- Q&A Wills Dean AligadaDocument5 pagesQ&A Wills Dean AligadaCzara DyPas encore d'évaluation

- PNB Vs CA DigestDocument3 pagesPNB Vs CA DigestCzara DyPas encore d'évaluation

- Reynolds v. Ca (Dy)Document2 pagesReynolds v. Ca (Dy)Czara DyPas encore d'évaluation

- Memorandum On Charter Change: Presidential Federal ConstitutionDocument1 pageMemorandum On Charter Change: Presidential Federal ConstitutionCzara DyPas encore d'évaluation

- Carpio CalaycayDocument4 pagesCarpio CalaycayCzara DyPas encore d'évaluation

- A Portrayal of Gender and A Description of Gender Roles in SelectDocument429 pagesA Portrayal of Gender and A Description of Gender Roles in SelectPtah El100% (1)

- UntitledDocument8 pagesUntitledMara GanalPas encore d'évaluation

- 150 Years of PharmacovigilanceDocument2 pages150 Years of PharmacovigilanceCarlos José Lacava Fernández100% (1)

- 2nd Exam 201460 UpdatedDocument12 pages2nd Exam 201460 UpdatedAlbert LuchyniPas encore d'évaluation

- National ScientistDocument2 pagesNational ScientistHu T. BunuanPas encore d'évaluation

- Ba GastrectomyDocument10 pagesBa GastrectomyHope3750% (2)

- Development Communication Theories MeansDocument13 pagesDevelopment Communication Theories MeansKendra NodaloPas encore d'évaluation

- Introduction To Computational Fluid DynamicsDocument3 pagesIntroduction To Computational Fluid DynamicsJonyzhitop TenorioPas encore d'évaluation

- AD&D 2nd Edition - Dark Sun - Monstrous Compendium - Appendix II - Terrors Beyond Tyr PDFDocument130 pagesAD&D 2nd Edition - Dark Sun - Monstrous Compendium - Appendix II - Terrors Beyond Tyr PDFWannes Ikkuhyu100% (8)

- Lesson Plan Earth and Life Science: Exogenic ProcessesDocument2 pagesLesson Plan Earth and Life Science: Exogenic ProcessesNuevalyn Quijano FernandoPas encore d'évaluation

- Eapp Module 1Document6 pagesEapp Module 1Benson CornejaPas encore d'évaluation

- InfoVista Xeus Pro 5 TMR Quick GuideDocument76 pagesInfoVista Xeus Pro 5 TMR Quick GuideNguyen Dang KhanhPas encore d'évaluation

- Role LibrariesDocument57 pagesRole LibrariesGiovanni AnggastaPas encore d'évaluation

- Why-Most Investors Are Mostly Wrong Most of The TimeDocument3 pagesWhy-Most Investors Are Mostly Wrong Most of The TimeBharat SahniPas encore d'évaluation

- 3658 - Implement Load BalancingDocument6 pages3658 - Implement Load BalancingDavid Hung NguyenPas encore d'évaluation

- Gaulish DictionaryDocument4 pagesGaulish DictionarywoodwysePas encore d'évaluation

- Mis 2023Document62 pagesMis 2023Ana Mae MunsayacPas encore d'évaluation

- ( (LEAD - FIRSTNAME) ) 'S Spouse Visa PackageDocument14 pages( (LEAD - FIRSTNAME) ) 'S Spouse Visa PackageDamon Culbert0% (1)

- Effective Communication Chapter11Document9 pagesEffective Communication Chapter11kamaljeet70Pas encore d'évaluation

- Endogenic Processes (Erosion and Deposition) : Group 3Document12 pagesEndogenic Processes (Erosion and Deposition) : Group 3Ralph Lawrence C. PagaranPas encore d'évaluation

- Sosa Ernest - Causation PDFDocument259 pagesSosa Ernest - Causation PDFtri korne penal100% (1)

- Girl: Dad, I Need A Few Supplies For School, and I Was Wondering If - . .Document3 pagesGirl: Dad, I Need A Few Supplies For School, and I Was Wondering If - . .AKSHATPas encore d'évaluation

- Breast Cancer ChemotherapyDocument7 pagesBreast Cancer Chemotherapydini kusmaharaniPas encore d'évaluation

- Calcutta Bill - Abhimanyug@Document2 pagesCalcutta Bill - Abhimanyug@abhimanyugirotraPas encore d'évaluation

- BD9897FS Ic DetailsDocument5 pagesBD9897FS Ic DetailsSundaram LakshmananPas encore d'évaluation

- Clinical Handbook of Infectious Diseases in Farm AnimalsDocument146 pagesClinical Handbook of Infectious Diseases in Farm Animalsigorgalopp100% (1)

- Lesson Plan (Speaking Skills)Document7 pagesLesson Plan (Speaking Skills)Nurul Fathiah Zulkarnain100% (1)

- SWOT ANALYSIS - TitleDocument9 pagesSWOT ANALYSIS - TitleAlexis John Altona BetitaPas encore d'évaluation

- Contoh Pidato Bahasa Inggris Dan Terjemahannya Untuk SMPDocument15 pagesContoh Pidato Bahasa Inggris Dan Terjemahannya Untuk SMPAli Husein SiregarPas encore d'évaluation

- 08 Night 09 Days Ujjain & Omkareshwar Tour Package - Travel HuntDocument5 pages08 Night 09 Days Ujjain & Omkareshwar Tour Package - Travel HuntsalesPas encore d'évaluation