Vous aimerez peut-être aussi

- Malakoff Ar2017 27.3.18 FinalDocument264 pagesMalakoff Ar2017 27.3.18 FinalfivanadaPas encore d'évaluation

- Svja 9 oDocument49 pagesSvja 9 ofivanadaPas encore d'évaluation

- ASG PersaraanDocument1 pageASG PersaraanfivanadaPas encore d'évaluation

- ERC+Resolution+No +17+s2013+-+Annex+A+ (Proposed+revision)Document29 pagesERC+Resolution+No +17+s2013+-+Annex+A+ (Proposed+revision)fivanadaPas encore d'évaluation

- Energy Malaysia Volume 11Document52 pagesEnergy Malaysia Volume 11fivanadaPas encore d'évaluation

- Energy Malaysia Volume 11Document52 pagesEnergy Malaysia Volume 11fivanadaPas encore d'évaluation

- Sabah Electricity Supply Industry Outlook 2015Document62 pagesSabah Electricity Supply Industry Outlook 2015fivanada100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

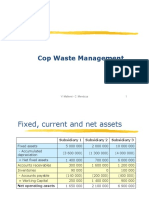

- Cop Waste Management SolutionDocument5 pagesCop Waste Management SolutionPaul GhanimehPas encore d'évaluation

- The Cost of Capital: Sources of Capital Component Costs Wacc Adjusting For Flotation Costs Adjusting For RiskDocument37 pagesThe Cost of Capital: Sources of Capital Component Costs Wacc Adjusting For Flotation Costs Adjusting For RiskMohammed MiftahPas encore d'évaluation

- From Beds, To Burgers, To Booze - Grand Metropolitan and The Creation of A Drinks GiantDocument13 pagesFrom Beds, To Burgers, To Booze - Grand Metropolitan and The Creation of A Drinks GiantHomme zyPas encore d'évaluation

- Adwords Fundamental Exam Questions Answers 2016Document21 pagesAdwords Fundamental Exam Questions Answers 2016Avinash VermaPas encore d'évaluation

- Mou Mt103 One WayDocument15 pagesMou Mt103 One WayParveen Jain80% (5)

- Revision Questions 2020 Part IDocument21 pagesRevision Questions 2020 Part IJeffrey KamPas encore d'évaluation

- Developing Agro-Industries For Employment Generation in Rural AreasDocument2 pagesDeveloping Agro-Industries For Employment Generation in Rural AreasRaj RudrapaaPas encore d'évaluation

- Management Accounting Summer 20091Document18 pagesManagement Accounting Summer 20091MahmozPas encore d'évaluation

- EVP Case StudyDocument11 pagesEVP Case StudyMayuri Joshi DhavalePas encore d'évaluation

- Construction & Design Mang ManualDocument93 pagesConstruction & Design Mang ManualSaad HajjarPas encore d'évaluation

- T3TMD - Miscellaneous Deals - R10Document78 pagesT3TMD - Miscellaneous Deals - R10KLB USERPas encore d'évaluation

- Marketing Demographics - The OpportunityDocument4 pagesMarketing Demographics - The OpportunityVonderPas encore d'évaluation

- PEL PakistanDocument27 pagesPEL Pakistanjutt707100% (1)

- Running Head: MARKETING PLAN 1Document21 pagesRunning Head: MARKETING PLAN 1Isba RafiquePas encore d'évaluation

- B2C Cross-Border E-Commerce Export Logistics ModeDocument7 pagesB2C Cross-Border E-Commerce Export Logistics ModeVoiceover SpotPas encore d'évaluation

- NTT 2011 CSR ReportDocument261 pagesNTT 2011 CSR ReportcattleyajenPas encore d'évaluation

- 523755152-503469149-GO2Bank-Template-2-2 NOVDocument3 pages523755152-503469149-GO2Bank-Template-2-2 NOVAlex NeziPas encore d'évaluation

- Portfolio ManagementDocument71 pagesPortfolio ManagementAnantha Nag100% (1)

- Lesson 5 EBBADocument152 pagesLesson 5 EBBAHuyền LinhPas encore d'évaluation

- Smart Notes On Contract DraftingDocument32 pagesSmart Notes On Contract DraftingGourav RathodPas encore d'évaluation

- Mcdonald'S China: Presented By: Team XiDocument7 pagesMcdonald'S China: Presented By: Team XiRuchita RanjanPas encore d'évaluation

- Raport Anual Accor HotelDocument404 pagesRaport Anual Accor HotelIsrati Valeriu100% (3)

- Plant Layout and Location DecisionsDocument52 pagesPlant Layout and Location DecisionsAEHYUN YENVYPas encore d'évaluation

- SBIR Program OverviewDocument13 pagesSBIR Program OverviewFernie1Pas encore d'évaluation

- BS Mumbai English 14-12Document20 pagesBS Mumbai English 14-12jay pujaraPas encore d'évaluation

- MSS - More Than MESDocument6 pagesMSS - More Than MESrkponrajPas encore d'évaluation

- Reviewer For MASDocument5 pagesReviewer For MASSVTKhsiaPas encore d'évaluation

- The Kurt Salmon Review Issue 05 VFSP PDFDocument68 pagesThe Kurt Salmon Review Issue 05 VFSP PDFDuc NguyenPas encore d'évaluation

- Methods of Software AcquisitionDocument12 pagesMethods of Software AcquisitionSimranjeet Singh100% (4)

- SAP IS Blue Print DocumentDocument4 pagesSAP IS Blue Print DocumentSupriyo DuttaPas encore d'évaluation