Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Global Currency Reset - Revaluation of Currencies - Historical OverviewDocument20 pagesGlobal Currency Reset - Revaluation of Currencies - Historical Overviewenerchi111196% (28)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- FIDIC Contracts Claims Management Dispute ResolutionDocument3 pagesFIDIC Contracts Claims Management Dispute ResolutionadamcyzPas encore d'évaluation

- Philippine Laws on Credit TransactionsDocument5 pagesPhilippine Laws on Credit TransactionsCamille ArominPas encore d'évaluation

- Company Analysis of Tata Steel (Bs Assignment)Document35 pagesCompany Analysis of Tata Steel (Bs Assignment)bedipankaj718181% (16)

- Chapter 14Document43 pagesChapter 14Dominic RomeroPas encore d'évaluation

- Bloomberg Energy Cheat SheetDocument2 pagesBloomberg Energy Cheat Sheetanup782Pas encore d'évaluation

- Summary-AHM 510 PDFDocument70 pagesSummary-AHM 510 PDFSiddhartha KalasikamPas encore d'évaluation

- SMA Session 1Document24 pagesSMA Session 1Siddhartha PatraPas encore d'évaluation

- Nihms 131892 PDFDocument13 pagesNihms 131892 PDFSiddhartha PatraPas encore d'évaluation

- How Maersk Line Executed on Its Social Media PlanDocument1 pageHow Maersk Line Executed on Its Social Media PlanSiddhartha PatraPas encore d'évaluation

- Nihms 131892 PDFDocument13 pagesNihms 131892 PDFSiddhartha PatraPas encore d'évaluation

- Swot Analysis Strengths of Tata SteelDocument1 pageSwot Analysis Strengths of Tata SteelSiddhartha PatraPas encore d'évaluation

- Financial DistressDocument32 pagesFinancial DistressSiddhartha PatraPas encore d'évaluation

- Two PortfolioDocument6 pagesTwo PortfolioSiddhartha PatraPas encore d'évaluation

- Mahindra Holidays and Resorts India LTDDocument9 pagesMahindra Holidays and Resorts India LTDSiddhartha PatraPas encore d'évaluation

- Financial DistressDocument32 pagesFinancial DistressSiddhartha PatraPas encore d'évaluation

- Two PortfolioDocument6 pagesTwo PortfolioSiddhartha PatraPas encore d'évaluation

- International Financial ManagementDocument15 pagesInternational Financial ManagementSiddhartha Patra0% (1)

- CF 2016 17 SecA GroupsDocument2 pagesCF 2016 17 SecA GroupsSiddhartha PatraPas encore d'évaluation

- CF 8 2016Document40 pagesCF 8 2016Siddhartha PatraPas encore d'évaluation

- Valuation and Pricing of BondsDocument43 pagesValuation and Pricing of BondsSiddhartha PatraPas encore d'évaluation

- Please Print Report On Both Sides of The Paper (There Is A Penalty For Not Adhering To This Norm)Document1 pagePlease Print Report On Both Sides of The Paper (There Is A Penalty For Not Adhering To This Norm)Siddhartha PatraPas encore d'évaluation

- CF 3 2016Document91 pagesCF 3 2016Siddhartha PatraPas encore d'évaluation

- CF 7 2016Document45 pagesCF 7 2016Siddhartha PatraPas encore d'évaluation

- Numerical Questions On As-14 - 1Document3 pagesNumerical Questions On As-14 - 1Siddhartha PatraPas encore d'évaluation

- Brand Positioning of Air ConditionsDocument87 pagesBrand Positioning of Air ConditionsSiddhartha PatraPas encore d'évaluation

- CF 1 2016Document27 pagesCF 1 2016Siddhartha PatraPas encore d'évaluation

- Business Models For Video GamesFINDocument94 pagesBusiness Models For Video GamesFINlarslehnhofPas encore d'évaluation

- Financial Markets and Services Groups (2017)Document3 pagesFinancial Markets and Services Groups (2017)Siddhartha PatraPas encore d'évaluation

- CF 2 2016Document50 pagesCF 2 2016Siddhartha PatraPas encore d'évaluation

- Assignment 2Document16 pagesAssignment 2Siddhartha PatraPas encore d'évaluation

- Video Game Industry Business Models and Strategies of Activision-Blizzard and EADocument71 pagesVideo Game Industry Business Models and Strategies of Activision-Blizzard and EASiddhartha PatraPas encore d'évaluation

- Hindalco NovelisDocument22 pagesHindalco NovelisSiddhartha PatraPas encore d'évaluation

- Strategic Review: Unit Code: U20467 Student Number: 483563Document26 pagesStrategic Review: Unit Code: U20467 Student Number: 483563Siddhartha PatraPas encore d'évaluation

- Chapter 2Document10 pagesChapter 2Siddhartha PatraPas encore d'évaluation

- Week 15 - Revision 2Document113 pagesWeek 15 - Revision 2Trung Nguyễn QuangPas encore d'évaluation

- Final Order - Case No 38 of 2014Document148 pagesFinal Order - Case No 38 of 2014sachinoilPas encore d'évaluation

- TheEdge + Sun-240124Document52 pagesTheEdge + Sun-240124one2paii-1Pas encore d'évaluation

- Heller, Jack, CPCUMARPDocument4 pagesHeller, Jack, CPCUMARPTexas WatchdogPas encore d'évaluation

- A Formal Language For Analyzing Contracts - Nick Szabo - Prelim Draft From 2002Document27 pagesA Formal Language For Analyzing Contracts - Nick Szabo - Prelim Draft From 2002John PPas encore d'évaluation

- COST ACCOUNTING HOMEWORKDocument6 pagesCOST ACCOUNTING HOMEWORKaltaPas encore d'évaluation

- PrefaceDocument49 pagesPrefaceManish RajakPas encore d'évaluation

- Raunak Kumar ResumeDocument2 pagesRaunak Kumar Resumeraunak29Pas encore d'évaluation

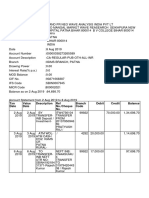

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaPas encore d'évaluation

- Updated - Ooredoo at A Glance 2019Document11 pagesUpdated - Ooredoo at A Glance 2019AMR ERFANPas encore d'évaluation

- IASB Conceptual Framework OverviewDocument28 pagesIASB Conceptual Framework OverviewTinoManhangaPas encore d'évaluation

- Case Study MMDocument4 pagesCase Study MMMehdi TaseerPas encore d'évaluation

- 8 - 8 - 31 - 2023 12 - 00 - 00 Am - 2023Document2 pages8 - 8 - 31 - 2023 12 - 00 - 00 Am - 2023Larry GatlinPas encore d'évaluation

- 5 Parkin Samantha Chapter 2 - Measuring Your Financial Health and Making A PlanDocument6 pages5 Parkin Samantha Chapter 2 - Measuring Your Financial Health and Making A Planapi-245262597100% (1)

- ProjectDocument79 pagesProjectvishwajit bhoir100% (1)

- TPA Deals Only With Immovable Property'Document17 pagesTPA Deals Only With Immovable Property'Prachi Verma0% (1)

- Chapter 6 Mental AccountingDocument6 pagesChapter 6 Mental AccountingAbdulPas encore d'évaluation

- Chapter 6 Partnership Formation Operation and LiquidationDocument6 pagesChapter 6 Partnership Formation Operation and Liquidationanwaradem225Pas encore d'évaluation

- Muslim Women Entrepreneurs: A Study On Success FactorsDocument14 pagesMuslim Women Entrepreneurs: A Study On Success FactorsBadiu'zzaman FahamiPas encore d'évaluation

- CLEANSING PROCESS FOR DIVIDENDS AND GAINSDocument2 pagesCLEANSING PROCESS FOR DIVIDENDS AND GAINSAbdul Aziz MuhammadPas encore d'évaluation

- Regular ManualDocument164 pagesRegular ManualManikdnathPas encore d'évaluation

- FCY English CTRA F98799eaDocument7 pagesFCY English CTRA F98799eaRojer DanzingerPas encore d'évaluation

- Notes - Timeliness of Reporting and Stock Price Reaction To Earnings AnnoucementsDocument12 pagesNotes - Timeliness of Reporting and Stock Price Reaction To Earnings AnnoucementsChacko JacobPas encore d'évaluation

- Vizco, Krizia Mae H.Document11 pagesVizco, Krizia Mae H.Meng VizcoPas encore d'évaluation