Vous aimerez peut-être aussi

- Sippican A Case Study PDFDocument9 pagesSippican A Case Study PDFAlex G. PichliavasPas encore d'évaluation

- SippicanDocument6 pagesSippicanMatija KaraulaPas encore d'évaluation

- Sippican Case Analysis ReportDocument3 pagesSippican Case Analysis Reportfelipecalvette100% (2)

- 241485467-Sippican Case PDFDocument6 pages241485467-Sippican Case PDFSylviaZambranoSorianoPas encore d'évaluation

- Sippican CorporationDocument3 pagesSippican CorporationSaswata Banerjee0% (1)

- Full Report Case 4Document13 pagesFull Report Case 4Ina Noina100% (4)

- Sippican CorporationDocument2 pagesSippican CorporationManikandan Swaminathan100% (3)

- Sippican Case ReviewDocument9 pagesSippican Case ReviewDavid KijadaPas encore d'évaluation

- 18 4 Sippican CorporationDocument2 pages18 4 Sippican CorporationamitkrhpcicPas encore d'évaluation

- Destin BrassDocument5 pagesDestin Brassdamanfromiran100% (1)

- Outsourcing Manifold ProductionDocument8 pagesOutsourcing Manifold Productionaliraza100% (2)

- WilkersonDocument4 pagesWilkersonmayurmachoPas encore d'évaluation

- Selligram Case Answer KeyDocument3 pagesSelligram Case Answer Keysharkss521Pas encore d'évaluation

- Sippican CoDocument5 pagesSippican CoMagali Thibaut67% (3)

- Wilkerson Company ABC Cost System Exhibit 1.a Cost Pool Cost DriverDocument2 pagesWilkerson Company ABC Cost System Exhibit 1.a Cost Pool Cost DriverLeonardoGomez100% (1)

- Wilkerson - Case Study1 PDFDocument2 pagesWilkerson - Case Study1 PDFPavanPas encore d'évaluation

- Bridgeton Industries Case Study Analysis of Overhead AllocationDocument3 pagesBridgeton Industries Case Study Analysis of Overhead Allocationzxcv3214100% (1)

- Destin Brass Costing ProjectDocument2 pagesDestin Brass Costing ProjectNitish Bhardwaj100% (1)

- Case Analysis of AIC NetbooksDocument7 pagesCase Analysis of AIC NetbooksHitesh Diyora0% (3)

- Bridgeton Industries Case Study - Designing Cost SystemsDocument2 pagesBridgeton Industries Case Study - Designing Cost Systemsdgrgich0% (3)

- Estimate break-even quantity for iPhone 4 using cost dataDocument1 pageEstimate break-even quantity for iPhone 4 using cost dataAnkit VermaPas encore d'évaluation

- DakotaDocument5 pagesDakotaMadhavi SerenityPas encore d'évaluation

- Siemens CaseDocument4 pagesSiemens Casespaw1108Pas encore d'évaluation

- 17-2 Lipman Bottle CompanyDocument6 pages17-2 Lipman Bottle CompanyYJ26126100% (1)

- Precision Motors Division CaseDocument9 pagesPrecision Motors Division CaseAliza Rizvi50% (2)

- Costing Systems Reveal True Product MarginsDocument1 pageCosting Systems Reveal True Product Marginsfelipevwa100% (1)

- Wilkerson Company ABCDocument4 pagesWilkerson Company ABCrajyalakshmiPas encore d'évaluation

- Seligram 2Document4 pagesSeligram 2Yvette YuanPas encore d'évaluation

- Wilkerson Case Assignment Questions Part 1Document1 pageWilkerson Case Assignment Questions Part 1gangster91Pas encore d'évaluation

- Colorscope Case - Operational Advantages and Cost AnalysisDocument2 pagesColorscope Case - Operational Advantages and Cost AnalysisstevenPas encore d'évaluation

- AIC NetbookDocument4 pagesAIC NetbookSalil AggarwalPas encore d'évaluation

- Wilkerson CompanyDocument2 pagesWilkerson CompanyAnkit VermaPas encore d'évaluation

- AIC Netbooks Optimizing Product AssemblyDocument2 pagesAIC Netbooks Optimizing Product AssemblyMrinal Gupta0% (4)

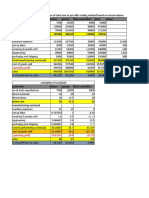

- Colorscope ExcelDocument11 pagesColorscope ExcelPriyabrat Mishra100% (1)

- Dakota Case Activity-Based Costing SolutionDocument6 pagesDakota Case Activity-Based Costing SolutionKamruzzamanPas encore d'évaluation

- How Does Wilkerson's Existing Cost System Operate? Develop A Diagram To Show How Costs Flow From Factory Expense Accounts To ProductsDocument4 pagesHow Does Wilkerson's Existing Cost System Operate? Develop A Diagram To Show How Costs Flow From Factory Expense Accounts To ProductsKunal DhagePas encore d'évaluation

- Dakota AnalysisDocument13 pagesDakota Analysistonylcaston100% (2)

- Import Distributors Case Analysis: Television Dept ContinuationDocument3 pagesImport Distributors Case Analysis: Television Dept ContinuationKram Olegna Anagerg0% (1)

- Cost Management - Software Associate CaseDocument7 pagesCost Management - Software Associate CaseVaibhav GuptaPas encore d'évaluation

- Wilkerson Company Full ReportDocument9 pagesWilkerson Company Full ReportFatihahZainalLim100% (1)

- Case1 Colorscope Solution PPTXDocument42 pagesCase1 Colorscope Solution PPTXAmit Dixit100% (1)

- Wilkerson Case Study FinalDocument5 pagesWilkerson Case Study Finalmayer_oferPas encore d'évaluation

- Dakota Office ProductsDocument10 pagesDakota Office ProductsMithun KarthikeyanPas encore d'évaluation

- Davey Brothers Watch Co. SubmissionDocument13 pagesDavey Brothers Watch Co. SubmissionEkta Derwal PGP 2022-24 BatchPas encore d'évaluation

- Company CASE 4 Analyzes Activity-Based Costing to Improve Profit Margins/TITLEDocument24 pagesCompany CASE 4 Analyzes Activity-Based Costing to Improve Profit Margins/TITLECik Beb Gojes100% (1)

- SUBJECT: Analyses and Recommendations For The Different Cost AccountingDocument4 pagesSUBJECT: Analyses and Recommendations For The Different Cost AccountinglddPas encore d'évaluation

- Classic Pen Company: Case Analysis - Activity Based Cost System Group - 07Document16 pagesClassic Pen Company: Case Analysis - Activity Based Cost System Group - 07Anupriya Sen100% (1)

- AIC Netbooks: Optimizing Assembly EfficiencyDocument6 pagesAIC Netbooks: Optimizing Assembly EfficiencyShivam Mishra100% (3)

- Destin Brass Case Study SolutionDocument5 pagesDestin Brass Case Study SolutionAmruta Turmé100% (2)

- Wilkerson CompanyDocument26 pagesWilkerson CompanyChris Vincent50% (2)

- EX 1 - WilkersonDocument8 pagesEX 1 - WilkersonDror PazPas encore d'évaluation

- Group 8Document20 pagesGroup 8nirajPas encore d'évaluation

- Wilkerson Case Study Final1Document5 pagesWilkerson Case Study Final1mayer_ofer95% (22)

- CH 10 SMDocument17 pagesCH 10 SMapi-267019092Pas encore d'évaluation

- TRADITIONAL VS ABC COSTING FOR TWO PRODUCTSDocument16 pagesTRADITIONAL VS ABC COSTING FOR TWO PRODUCTSrsalicsicPas encore d'évaluation

- F5 Handout 1 For Dec 2011Document18 pagesF5 Handout 1 For Dec 2011saeed@atcPas encore d'évaluation

- Activity Based Costing Worked Example: Products TotalDocument6 pagesActivity Based Costing Worked Example: Products TotalafghanihunkPas encore d'évaluation

- Mas 03 - Activity Based CostingDocument6 pagesMas 03 - Activity Based CostingCarl Angelo LopezPas encore d'évaluation

- Chapter 5 (Activity-Based Costing) Video: Overhead To Products Based On Direct Labor, With Labor Being A Measure ofDocument8 pagesChapter 5 (Activity-Based Costing) Video: Overhead To Products Based On Direct Labor, With Labor Being A Measure ofMhekai SuarezPas encore d'évaluation

- CH 10 SMDocument17 pagesCH 10 SMNafisah MambuayPas encore d'évaluation

- Project Case - Brannigan Foods - Financial CalculationsDocument2 pagesProject Case - Brannigan Foods - Financial CalculationsDuyên NguyễnPas encore d'évaluation

- 6 Joint AND By-Product Costing: Lecture Notes - 12/13 Jan 2015Document27 pages6 Joint AND By-Product Costing: Lecture Notes - 12/13 Jan 2015XPas encore d'évaluation

- HashLabs V3 - Feb 2021 - Financial ProjectionsDocument260 pagesHashLabs V3 - Feb 2021 - Financial Projectionsবিষাক্ত মানবPas encore d'évaluation

- Z Company Income Statement ComparisonDocument11 pagesZ Company Income Statement ComparisonMohamed RefaayPas encore d'évaluation

- RSM222 Costing AssignmentDocument14 pagesRSM222 Costing AssignmentKirsten WangPas encore d'évaluation

- DGS Mock Exam - Full AnswerDocument11 pagesDGS Mock Exam - Full AnswerSofia NicoriciPas encore d'évaluation

- The cost of unused capacity is $10,000 (50,000 - 40,000 units x $2 POHRDocument80 pagesThe cost of unused capacity is $10,000 (50,000 - 40,000 units x $2 POHRCaila Joice FavorPas encore d'évaluation

- Spoilage, Scrap, ReworkDocument6 pagesSpoilage, Scrap, ReworkJanine Malicdem AvilaPas encore d'évaluation

- Mark Up, Markdown Gross MarginDocument17 pagesMark Up, Markdown Gross MarginDenise CordetaPas encore d'évaluation

- Business ModelDocument3 pagesBusiness ModelAnji JoguilonPas encore d'évaluation

- Handouts and WorksheetsDocument47 pagesHandouts and WorksheetsPio GuiretPas encore d'évaluation

- HWChap 006Document67 pagesHWChap 006hellooceanPas encore d'évaluation

- Financial Aspects Ofmarketing ManagementDocument38 pagesFinancial Aspects Ofmarketing ManagementAli AlsayedPas encore d'évaluation

- Chapter 3 CVPDocument26 pagesChapter 3 CVPshuhadaPas encore d'évaluation

- "Financial Statement Analysis of Bank of Maharashtra": A Project Report OnDocument65 pages"Financial Statement Analysis of Bank of Maharashtra": A Project Report OnShashi RanjanPas encore d'évaluation

- Nature ViewDocument4 pagesNature ViewRituja RanePas encore d'évaluation

- Case Study of Amazon's CSR PerformanceDocument19 pagesCase Study of Amazon's CSR PerformanceJahid Hasan MenonPas encore d'évaluation

- CHAPTER 4 Basic Pricing Strategies and The Use of Breakeven AnalysisDocument30 pagesCHAPTER 4 Basic Pricing Strategies and The Use of Breakeven AnalysisWilfredo Yabut Jr.100% (2)

- CHP MethodologyDocument12 pagesCHP MethodologyHojing SeokPas encore d'évaluation

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 10Document26 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 10jasperkennedy083% (36)

- Pie Restaurant Business PlanDocument45 pagesPie Restaurant Business PlanVuinsia BcsbacPas encore d'évaluation

- Variable Costing: A Decision-Making Perspective: True-False StatementsDocument8 pagesVariable Costing: A Decision-Making Perspective: True-False StatementsJanina Marie GarciaPas encore d'évaluation

- Solutions To All Assigned Practice Problems (W502)Document27 pagesSolutions To All Assigned Practice Problems (W502)donjazonPas encore d'évaluation

- Weekly PlusDocument12 pagesWeekly PlusRandora LkPas encore d'évaluation

- Inventories: Additional Valuation IssuesDocument44 pagesInventories: Additional Valuation IssuesjulsPas encore d'évaluation

- Executive SummaryDocument49 pagesExecutive SummaryMuhsin ShahPas encore d'évaluation

- Grocery Inquiry Report - July 2008Document543 pagesGrocery Inquiry Report - July 2008Abdikadir AbdiPas encore d'évaluation

- Analysis and RatioDocument35 pagesAnalysis and RatioJP80% (5)

- 2 Example Problems CH 7 8Document30 pages2 Example Problems CH 7 8Aldrin Zolina100% (1)

- The Machine That Changed the World: The Story of Lean Production-- Toyota's Secret Weapon in the Global Car Wars That Is Now Revolutionizing World IndustryD'EverandThe Machine That Changed the World: The Story of Lean Production-- Toyota's Secret Weapon in the Global Car Wars That Is Now Revolutionizing World IndustryÉvaluation : 4.5 sur 5 étoiles4.5/5 (40)

- Process!: How Discipline and Consistency Will Set You and Your Business FreeD'EverandProcess!: How Discipline and Consistency Will Set You and Your Business FreeÉvaluation : 4.5 sur 5 étoiles4.5/5 (5)

- The Goal: A Process of Ongoing Improvement - 30th Aniversary EditionD'EverandThe Goal: A Process of Ongoing Improvement - 30th Aniversary EditionÉvaluation : 4 sur 5 étoiles4/5 (684)

- Leading Product Development: The Senior Manager's Guide to Creating and ShapingD'EverandLeading Product Development: The Senior Manager's Guide to Creating and ShapingÉvaluation : 5 sur 5 étoiles5/5 (1)

- Project Planning and SchedulingD'EverandProject Planning and SchedulingÉvaluation : 5 sur 5 étoiles5/5 (6)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItD'EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItÉvaluation : 5 sur 5 étoiles5/5 (13)

- PMP Exam Prep: How to pass the PMP Exam on your First Attempt – Learn Faster, Retain More and Pass the PMP ExamD'EverandPMP Exam Prep: How to pass the PMP Exam on your First Attempt – Learn Faster, Retain More and Pass the PMP ExamÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- Self-Discipline: The Ultimate Guide To Beat Procrastination, Achieve Your Goals, and Get What You Want In Your LifeD'EverandSelf-Discipline: The Ultimate Guide To Beat Procrastination, Achieve Your Goals, and Get What You Want In Your LifeÉvaluation : 4.5 sur 5 étoiles4.5/5 (662)

- Kaizen: The Step-by-Step Guide to Success. Adopt a Winning Mindset and Learn Effective Strategies to Productivity Improvement.D'EverandKaizen: The Step-by-Step Guide to Success. Adopt a Winning Mindset and Learn Effective Strategies to Productivity Improvement.Pas encore d'évaluation

- Kanban: A Step-by-Step Guide to Agile Project Management with KanbanD'EverandKanban: A Step-by-Step Guide to Agile Project Management with KanbanÉvaluation : 5 sur 5 étoiles5/5 (6)

- Vibration Basics and Machine Reliability Simplified : A Practical Guide to Vibration AnalysisD'EverandVibration Basics and Machine Reliability Simplified : A Practical Guide to Vibration AnalysisÉvaluation : 4 sur 5 étoiles4/5 (2)

- The Influential Product Manager: How to Lead and Launch Successful Technology ProductsD'EverandThe Influential Product Manager: How to Lead and Launch Successful Technology ProductsÉvaluation : 5 sur 5 étoiles5/5 (2)

- Value Stream Mapping: How to Visualize Work and Align Leadership for Organizational Transformation: How to Visualize Work and Align Leadership for Organizational TransformationD'EverandValue Stream Mapping: How to Visualize Work and Align Leadership for Organizational Transformation: How to Visualize Work and Align Leadership for Organizational TransformationÉvaluation : 5 sur 5 étoiles5/5 (34)

- Design Thinking for Beginners: Innovation as a Factor for Entrepreneurial SuccessD'EverandDesign Thinking for Beginners: Innovation as a Factor for Entrepreneurial SuccessÉvaluation : 4.5 sur 5 étoiles4.5/5 (7)

- Digital Supply Networks: Transform Your Supply Chain and Gain Competitive Advantage with Disruptive Technology and Reimagined ProcessesD'EverandDigital Supply Networks: Transform Your Supply Chain and Gain Competitive Advantage with Disruptive Technology and Reimagined ProcessesÉvaluation : 5 sur 5 étoiles5/5 (5)

- Execution (Review and Analysis of Bossidy and Charan's Book)D'EverandExecution (Review and Analysis of Bossidy and Charan's Book)Pas encore d'évaluation

- Total Productive Maintenance For Organisational EffectivenessD'EverandTotal Productive Maintenance For Organisational EffectivenessÉvaluation : 4 sur 5 étoiles4/5 (4)