Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Compiled UPCAT Questions Mathematics - Dxgty9 PDFDocument17 pagesCompiled UPCAT Questions Mathematics - Dxgty9 PDFMeg Angela Cirunay-DecenaPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Defective ContractsDocument3 pagesDefective Contractsisangbedista100% (2)

- Ose Pa1Document17 pagesOse Pa1gladys manaliliPas encore d'évaluation

- Chapter 11 - AnswerDocument31 pagesChapter 11 - AnsweragnesPas encore d'évaluation

- Law NotesDocument21 pagesLaw NotesVic FabePas encore d'évaluation

- CPAR P2 7406 Business Combination at Date of Acquisition With Answer PDFDocument6 pagesCPAR P2 7406 Business Combination at Date of Acquisition With Answer PDFRose Vee0% (2)

- Ose - Pa2Document18 pagesOse - Pa2gladys manaliliPas encore d'évaluation

- Blank Taxi Receipt TemplateDocument4 pagesBlank Taxi Receipt TemplatedigrajPas encore d'évaluation

- Fraud and ErrorDocument6 pagesFraud and ErrorSel AtenionPas encore d'évaluation

- CamScanner Scans PDF DocsDocument6 pagesCamScanner Scans PDF Docsgladys manaliliPas encore d'évaluation

- Chapter 18 - AnswerDocument7 pagesChapter 18 - AnswerAgentSkySkyPas encore d'évaluation

- BSPDocument1 pageBSPgladsPas encore d'évaluation

- Taxation Law UST PDFDocument339 pagesTaxation Law UST PDFAdelaide MabalotPas encore d'évaluation

- Major Deficiencies That Took Place During The Audit Process: Deficiency in The Audit Why It Was A Deficiency?Document2 pagesMajor Deficiencies That Took Place During The Audit Process: Deficiency in The Audit Why It Was A Deficiency?gladys manaliliPas encore d'évaluation

- T BSP P S 1. What Is Inflation?Document18 pagesT BSP P S 1. What Is Inflation?gladys manaliliPas encore d'évaluation

- Aud TheoDocument30 pagesAud TheogladsPas encore d'évaluation

- T BSP P S 1. What Is Inflation?Document18 pagesT BSP P S 1. What Is Inflation?gladys manaliliPas encore d'évaluation

- AuditingDocument37 pagesAuditingJoyce A. DawatesPas encore d'évaluation

- Aud TheoDocument30 pagesAud TheogladsPas encore d'évaluation

- M Ess g-4Document11 pagesM Ess g-4gladys manaliliPas encore d'évaluation

- Geometry PDFDocument14 pagesGeometry PDFgladys manaliliPas encore d'évaluation

- Arcs and Chords: THEOREM 11.4Document5 pagesArcs and Chords: THEOREM 11.4gladys manaliliPas encore d'évaluation

- Geometrical PDFDocument24 pagesGeometrical PDFgladys manaliliPas encore d'évaluation

- Arcs and Chords: THEOREM 11.4Document5 pagesArcs and Chords: THEOREM 11.4gladys manaliliPas encore d'évaluation

- Taxation Law UST PDFDocument339 pagesTaxation Law UST PDFAdelaide MabalotPas encore d'évaluation

- Taxation Law UST PDFDocument339 pagesTaxation Law UST PDFAdelaide MabalotPas encore d'évaluation

- Geometry PDFDocument14 pagesGeometry PDFgladys manaliliPas encore d'évaluation

- Red Is CountingDocument16 pagesRed Is Countinggladys manaliliPas encore d'évaluation

- Auditing Chapter 07Document18 pagesAuditing Chapter 07gladys manaliliPas encore d'évaluation

- Arcs and Chords: THEOREM 11.4Document5 pagesArcs and Chords: THEOREM 11.4gladys manaliliPas encore d'évaluation

- Appellee.: Chanrobles Law LibraryDocument16 pagesAppellee.: Chanrobles Law Librarygladys manaliliPas encore d'évaluation

- ADGM General Rulebook GENDocument114 pagesADGM General Rulebook GENAdrin AshPas encore d'évaluation

- Appointment, Removal and Resignation of An AuditorDocument8 pagesAppointment, Removal and Resignation of An AuditorDsp VarmaPas encore d'évaluation

- 01 Structure of Financial AccountingDocument41 pages01 Structure of Financial AccountinglrgerardPas encore d'évaluation

- Far East Group Limited Prospectus PDFDocument262 pagesFar East Group Limited Prospectus PDFBilly LeePas encore d'évaluation

- Internal Halal Auditing Documents and MaDocument20 pagesInternal Halal Auditing Documents and Maquality wyzePas encore d'évaluation

- Donde R. Salazar, Cpa: Independent Auditors' Report The Board of Directors Seabutterfly IncDocument2 pagesDonde R. Salazar, Cpa: Independent Auditors' Report The Board of Directors Seabutterfly IncJheza Mae PitogoPas encore d'évaluation

- 2012 Paper F8 QandA PDFDocument144 pages2012 Paper F8 QandA PDFmiaeyangwaheedPas encore d'évaluation

- Control Account Reconciliations ExamplesDocument3 pagesControl Account Reconciliations ExamplesRameen FatimaPas encore d'évaluation

- Accounting Changes in The Public Sector in EstoniaDocument10 pagesAccounting Changes in The Public Sector in EstoniaMohammad AlfianPas encore d'évaluation

- Cost of Goods Sold Assignment Q No. 03 To 09Document7 pagesCost of Goods Sold Assignment Q No. 03 To 09mukarram123100% (2)

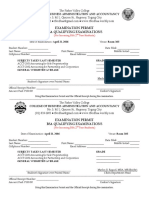

- 2016 Bsa Qualifying Examination PermitDocument2 pages2016 Bsa Qualifying Examination Permitapi-194241825Pas encore d'évaluation

- Nagaland University Act, 1989Document34 pagesNagaland University Act, 1989Latest Laws TeamPas encore d'évaluation

- Chapter 2Document35 pagesChapter 2Ellah GedalanonPas encore d'évaluation

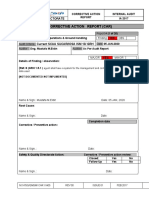

- Corrective Action Report (Car) : Safety & Quality DirectorateDocument26 pagesCorrective Action Report (Car) : Safety & Quality DirectorateNAI HmamiPas encore d'évaluation

- Establish Quality StandardsDocument15 pagesEstablish Quality Standardstemesgen yohannes100% (1)

- Effectiveness of Minority Language ProjectsDocument22 pagesEffectiveness of Minority Language ProjectslaloshPas encore d'évaluation

- Aas 7 Relying Upon The Work of An Internal AuditorDocument4 pagesAas 7 Relying Upon The Work of An Internal AuditorRishabh GuptaPas encore d'évaluation

- Audit of ReceivablesDocument8 pagesAudit of ReceivablesClene DocontePas encore d'évaluation

- Book Keeping AccountancyDocument8 pagesBook Keeping AccountancyNarra JanardhanPas encore d'évaluation

- IFRS A Briefing For Boards of DirectorsDocument60 pagesIFRS A Briefing For Boards of DirectorsJose Martin Castillo PatiñoPas encore d'évaluation

- Code of Corporate Governance: The Board'S Governance ResponsibilitiesDocument12 pagesCode of Corporate Governance: The Board'S Governance ResponsibilitiesMartha TanPas encore d'évaluation

- True or FalseDocument1 pageTrue or FalseStela Marie CarandangPas encore d'évaluation

- Tendernotice 1Document82 pagesTendernotice 1viveknigamPas encore d'évaluation

- Government Accounting Written ReportDocument14 pagesGovernment Accounting Written ReportMary Joy DomantayPas encore d'évaluation

- Audit of The Revenue and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Revenue and Collection CycleDocument20 pagesAudit of The Revenue and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Revenue and Collection Cycleem cortezPas encore d'évaluation

- AUI3703 Assignm02 Solution S2 2022 FinalDocument12 pagesAUI3703 Assignm02 Solution S2 2022 FinalTerrence MokoenaPas encore d'évaluation

- (Samsung Biologics) 2022 Business ReportDocument26 pages(Samsung Biologics) 2022 Business Report林正遠Pas encore d'évaluation

- Islam Aur Jadeed Maeeshat o Tijarat by Mufti Taqi UsmaniDocument171 pagesIslam Aur Jadeed Maeeshat o Tijarat by Mufti Taqi UsmaniShahood Ahmed100% (1)