Vous aimerez peut-être aussi

- Viability of Mixed-Use DevelopmentsDocument2 pagesViability of Mixed-Use DevelopmentsogrimlookednightPas encore d'évaluation

- Viability of Mixed-Use DevelopmentsDocument2 pagesViability of Mixed-Use DevelopmentsogrimlookednightPas encore d'évaluation

- Overview of Japanese Cross-Border Mergers and AcquisitionsDocument6 pagesOverview of Japanese Cross-Border Mergers and AcquisitionsogrimlookednightPas encore d'évaluation

- Joint Venture Conflicts of InterestDocument4 pagesJoint Venture Conflicts of InterestogrimlookednightPas encore d'évaluation

- Philippine Credit Rating MovementsDocument1 pagePhilippine Credit Rating MovementsogrimlookednightPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

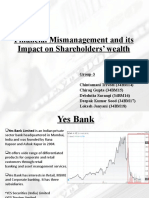

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 pagesGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodPas encore d'évaluation

- Summary of IFRS 12Document3 pagesSummary of IFRS 12Dwight BentPas encore d'évaluation

- Prosedur Dan Akibat Hukum Penundaan Kewajiban Pembayaran Utang Perseroan Terbatas (Studi Kasus Putusan Nomor 03/PKPU/2010/PN - Niaga.Sby)Document5 pagesProsedur Dan Akibat Hukum Penundaan Kewajiban Pembayaran Utang Perseroan Terbatas (Studi Kasus Putusan Nomor 03/PKPU/2010/PN - Niaga.Sby)anindita putriPas encore d'évaluation

- Financial Model of New RestaurantDocument42 pagesFinancial Model of New RestaurantPrabhdeep Dadyal0% (1)

- Financial Model: Prepared By: The Marquee GroupDocument16 pagesFinancial Model: Prepared By: The Marquee GroupSZA100% (1)

- Ifrs Example Interim Consolidated Financial Statements 2021Document46 pagesIfrs Example Interim Consolidated Financial Statements 2021Kurt Leonard AlbaoPas encore d'évaluation

- CHAPTER 4 Adjusting The AccountsDocument5 pagesCHAPTER 4 Adjusting The Accountsmojii caarrPas encore d'évaluation

- 32 Daggu Srinivasa Chakravarthi D'Souza Abner Aldrich Damarla Geetha Susmitha Greenlam Industries LTD Stylam Industries LTDDocument16 pages32 Daggu Srinivasa Chakravarthi D'Souza Abner Aldrich Damarla Geetha Susmitha Greenlam Industries LTD Stylam Industries LTDDAGGU SRINIVASA CHAKRAVARTHIPas encore d'évaluation

- Book Value Per Common ShareDocument2 pagesBook Value Per Common SharepriteechauhanPas encore d'évaluation

- Company Law Last Day Revision Notes CA InterDocument2 pagesCompany Law Last Day Revision Notes CA InterGANESH KUNJAPPA POOJARI100% (1)

- HERTZMEMARTDocument15 pagesHERTZMEMARTDismas LyassaPas encore d'évaluation

- OffentliggorelseDocument23 pagesOffentliggorelseJames RodriguezPas encore d'évaluation

- CH 14 Country and Political RiskDocument32 pagesCH 14 Country and Political Riskklm klmPas encore d'évaluation

- 87efe75eb3 9308202d90Document101 pages87efe75eb3 9308202d90Azzirwand SufriePas encore d'évaluation

- Cost Accountancy: Bba - Ii Semester - IiiDocument19 pagesCost Accountancy: Bba - Ii Semester - IiiNishikant RayanadePas encore d'évaluation

- Module 2 - Partnership OperationsDocument10 pagesModule 2 - Partnership OperationsJhanella Faith FagarPas encore d'évaluation

- SearsDocument11 pagesSearsHelplinePas encore d'évaluation

- p2 Long SeatworkDocument6 pagesp2 Long SeatworkLeisleiRagoPas encore d'évaluation

- T2 Corporation Income Tax Return (2019 and Later Tax Years) : IdentificationDocument9 pagesT2 Corporation Income Tax Return (2019 and Later Tax Years) : IdentificationBryan WilleyPas encore d'évaluation

- LSIP - Bilingual - 30 - Sep - 2022 RELEASE PDFDocument121 pagesLSIP - Bilingual - 30 - Sep - 2022 RELEASE PDFandry4jcPas encore d'évaluation

- Review Materials For DeptlDocument4 pagesReview Materials For DeptlSteffPas encore d'évaluation

- Financial Accounting Disposal of Asset and Good Will Week 3Document28 pagesFinancial Accounting Disposal of Asset and Good Will Week 3Hania SohailPas encore d'évaluation

- BIMB Vs BSN PDFDocument10 pagesBIMB Vs BSN PDFIelts TutorPas encore d'évaluation

- Phase 2 - 420 & 445Document60 pagesPhase 2 - 420 & 445SPas encore d'évaluation

- Ssignment RiefDocument6 pagesSsignment RiefShah MuradPas encore d'évaluation

- Assignment On Powers of Corporation Pt. 3 Name: Section: Date: ScoreDocument2 pagesAssignment On Powers of Corporation Pt. 3 Name: Section: Date: ScoreKris Tine100% (1)

- Fees Hit Private-EquityCos - Dechert StudyDocument3 pagesFees Hit Private-EquityCos - Dechert StudyputigersPas encore d'évaluation

- ASE20093 Resource BookDocument8 pagesASE20093 Resource BookAung Zaw Htwe0% (1)

- The Role of Accounting in BusinessDocument18 pagesThe Role of Accounting in BusinessJawad AzizPas encore d'évaluation

- Mid Term Examination Far 1st Sem 22 23Document11 pagesMid Term Examination Far 1st Sem 22 23Rechelle Anne Naris ObilloPas encore d'évaluation