Vous aimerez peut-être aussi

- ScotiaBank-JUN-25-Weekly FX CFTC Commitments of TradersDocument4 pagesScotiaBank-JUN-25-Weekly FX CFTC Commitments of TradersMiir ViirPas encore d'évaluation

- September 12th CFTC DataDocument3 pagesSeptember 12th CFTC Dataderailedcapitalism.comPas encore d'évaluation

- Exc Rate As On Jan 30, 2024Document1 pageExc Rate As On Jan 30, 2024Gourab SarkarPas encore d'évaluation

- October 15th CFTC DataDocument3 pagesOctober 15th CFTC Dataderailedcapitalism.comPas encore d'évaluation

- Exc Rate As On Aug 02, 2023Document1 pageExc Rate As On Aug 02, 2023kutyranisPas encore d'évaluation

- September 17th CFTC DataDocument3 pagesSeptember 17th CFTC Dataderailedcapitalism.comPas encore d'évaluation

- Use Market Reportjan 10-2008Document1 pageUse Market Reportjan 10-2008Semwanga GodfreyPas encore d'évaluation

- Weekly Report - 11 June 2021Document4 pagesWeekly Report - 11 June 2021Dan HathurusinghePas encore d'évaluation

- Name Type SymbolDocument3 pagesName Type SymbolMergim VeselajPas encore d'évaluation

- Exc Rate As On Aug 01, 2023Document1 pageExc Rate As On Aug 01, 2023kutyranisPas encore d'évaluation

- Company Name Ticker Free Float Volume Traded Share Outstandin G Average Closing PriceDocument23 pagesCompany Name Ticker Free Float Volume Traded Share Outstandin G Average Closing PricenkmpatnaPas encore d'évaluation

- Exc Rate As On Nov 08, 2022Document1 pageExc Rate As On Nov 08, 2022iftihaj HossainPas encore d'évaluation

- SWP Return CalculatorDocument14 pagesSWP Return CalculatorMarotrao BhisePas encore d'évaluation

- 2022 January Report: 1) Win & Loss ChartDocument3 pages2022 January Report: 1) Win & Loss ChartKeren Martha Guerrero OlivaresPas encore d'évaluation

- Adira Dinamika Multi Finance TBKDocument3 pagesAdira Dinamika Multi Finance TBKrofiqsabilalPas encore d'évaluation

- Weekly 12082017Document5 pagesWeekly 12082017Thiyaga RajanPas encore d'évaluation

- October 8th CFTC DataDocument3 pagesOctober 8th CFTC Dataderailedcapitalism.comPas encore d'évaluation

- September 24th CFTC DataDocument3 pagesSeptember 24th CFTC Dataderailedcapitalism.comPas encore d'évaluation

- ForexDocument1 pageForexMuhammad NomanPas encore d'évaluation

- Vishnu Trading Account Report FinvasiaDocument6 pagesVishnu Trading Account Report FinvasiaNiraj HPas encore d'évaluation

- BTPNDocument3 pagesBTPNNidaPas encore d'évaluation

- SWP MAF - Jun'22Document6 pagesSWP MAF - Jun'22Deepak GoyalPas encore d'évaluation

- Mapi PDFDocument3 pagesMapi PDFSabila Surya PutriPas encore d'évaluation

- Rate Sheet 12032023Document1 pageRate Sheet 12032023Fernando TorresPas encore d'évaluation

- Tuesday 09 Jun - 07.00 CET: Market Strategy Trends Moving Averages Strength Support Spot ResistanceDocument1 pageTuesday 09 Jun - 07.00 CET: Market Strategy Trends Moving Averages Strength Support Spot Resistancecibercollins2014Pas encore d'évaluation

- Mayes 8e CH06 SolutionsDocument18 pagesMayes 8e CH06 SolutionsRamez AhmedPas encore d'évaluation

- Tabel5 40Document4 pagesTabel5 40doby907Pas encore d'évaluation

- Amarnath Advisors DataDocument12 pagesAmarnath Advisors Dataashutosh trivediPas encore d'évaluation

- Foreign Investments in IndiaDocument10 pagesForeign Investments in IndiavasuPas encore d'évaluation

- Rupee Karvy 130911Document3 pagesRupee Karvy 130911jitmPas encore d'évaluation

- Anoop Report On Parle GDocument2 pagesAnoop Report On Parle GAnoop PatidarPas encore d'évaluation

- LPCKDocument3 pagesLPCKPrasetyo Indra SuronoPas encore d'évaluation

- Equity Futures & Options SegmentDocument20 pagesEquity Futures & Options SegmentsuralkarPas encore d'évaluation

- Archives: Stock PricesDocument9 pagesArchives: Stock PricesPuneit YadavPas encore d'évaluation

- Exchange RateDocument1 pageExchange RateBRTA SCSPas encore d'évaluation

- October 1st CFTC DataDocument3 pagesOctober 1st CFTC Dataderailedcapitalism.comPas encore d'évaluation

- 08.populasi Unit Hauling Juni 2023Document1 page08.populasi Unit Hauling Juni 2023Saparnas RoniPas encore d'évaluation

- Speculators Reduced Bets in Favor of The Dollar in IMM - CFTC September 17, 2013Document1 pageSpeculators Reduced Bets in Favor of The Dollar in IMM - CFTC September 17, 2013Eduardo PetazzePas encore d'évaluation

- 12.populasi Unit Hauling Juni 2023Document1 page12.populasi Unit Hauling Juni 2023Saparnas RoniPas encore d'évaluation

- Exchange RateDocument1 pageExchange RateFaisal MahbubPas encore d'évaluation

- QuotesDocument7 pagesQuotesJames BestPas encore d'évaluation

- JUL 21 DanskeTechnicalUpdateDocument1 pageJUL 21 DanskeTechnicalUpdateMiir ViirPas encore d'évaluation

- DailyNewsLetter - 20 Oct 10Document3 pagesDailyNewsLetter - 20 Oct 10checrucifixPas encore d'évaluation

- AcesDocument3 pagesAceswidiandikaPas encore d'évaluation

- RKDPLK - 3353 - 2021Document42 pagesRKDPLK - 3353 - 2021Benjamin Eliezer Pascareno SimanjuntakPas encore d'évaluation

- Rate SheetDocument1 pageRate Sheetmuhammad bhamPas encore d'évaluation

- Daily Report: News & UpdatesDocument3 pagesDaily Report: News & UpdatesМөнхбат ДоржпүрэвPas encore d'évaluation

- Exchange Rate 31 May 2023Document2 pagesExchange Rate 31 May 2023BRTA SCSPas encore d'évaluation

- Exc Rate As On Aug 23, 2021Document1 pageExc Rate As On Aug 23, 2021MRKNPas encore d'évaluation

- Exc Rate As On Aug 23, 2021Document1 pageExc Rate As On Aug 23, 2021MRKNPas encore d'évaluation

- Exc Rate As On Aug 23, 2021Document1 pageExc Rate As On Aug 23, 2021Md. Mohit HasanPas encore d'évaluation

- Exc Rate As On Aug 23, 2021Document1 pageExc Rate As On Aug 23, 2021MRKNPas encore d'évaluation

- AUG 06 DanskeTechnicalUpdateDocument1 pageAUG 06 DanskeTechnicalUpdateMiir ViirPas encore d'évaluation

- Foreign Exchange Rate Sheet: Bulletin August 21, 2020Document1 pageForeign Exchange Rate Sheet: Bulletin August 21, 2020asifimasterPas encore d'évaluation

- ADTV and RPCDocument15 pagesADTV and RPCBVMF_RIPas encore d'évaluation

- Analysis of ITC Stocks Against BSEDocument13 pagesAnalysis of ITC Stocks Against BSEAnupam GautamPas encore d'évaluation

- RateSheet - 2024-04-10T202549.828Document1 pageRateSheet - 2024-04-10T202549.828Fawad khanPas encore d'évaluation

- Issue & Receipt KPIs June2010Document13 pagesIssue & Receipt KPIs June2010ayazraboPas encore d'évaluation

- 23 12 11 Yanzhou Coal NomuraDocument14 pages23 12 11 Yanzhou Coal NomuraMichael BauermPas encore d'évaluation

- India Heart of Gold Revival 10 Nov 2010Document28 pagesIndia Heart of Gold Revival 10 Nov 2010derailedcapitalism.comPas encore d'évaluation

- Currency Report Card - USD Recovery: Three Month Forecast ReturnsDocument26 pagesCurrency Report Card - USD Recovery: Three Month Forecast Returnsderailedcapitalism.comPas encore d'évaluation

- The Weekly Peak - December 10, 2010Document7 pagesThe Weekly Peak - December 10, 2010derailedcapitalism.comPas encore d'évaluation

- Annual State of The Residential Mortgage Market in CanadaDocument43 pagesAnnual State of The Residential Mortgage Market in Canadaderailedcapitalism.comPas encore d'évaluation

- CME Silver Margin RequirementsDocument2 pagesCME Silver Margin Requirementsderailedcapitalism.comPas encore d'évaluation

- Oct 27 Home SalesDocument4 pagesOct 27 Home Salesderailedcapitalism.comPas encore d'évaluation

- Picton MahoneyDocument3 pagesPicton Mahoneyderailedcapitalism.comPas encore d'évaluation

- Guggenheim Partners - Market Perspectives - September 30, 2010Document10 pagesGuggenheim Partners - Market Perspectives - September 30, 2010derailedcapitalism.comPas encore d'évaluation

- October 22nd CFTC DataDocument3 pagesOctober 22nd CFTC Dataderailedcapitalism.comPas encore d'évaluation

- What Canada Can Teach The WorldDocument6 pagesWhat Canada Can Teach The Worldderailedcapitalism.comPas encore d'évaluation

- October 8th CFTC DataDocument3 pagesOctober 8th CFTC Dataderailedcapitalism.comPas encore d'évaluation

- October 1st CFTC DataDocument3 pagesOctober 1st CFTC Dataderailedcapitalism.comPas encore d'évaluation

- September 24th CFTC DataDocument3 pagesSeptember 24th CFTC Dataderailedcapitalism.comPas encore d'évaluation

- Pay As You Earn UK ProposalDocument34 pagesPay As You Earn UK Proposalderailedcapitalism.comPas encore d'évaluation

- September 17th CFTC DataDocument3 pagesSeptember 17th CFTC Dataderailedcapitalism.comPas encore d'évaluation

- ECGCDocument9 pagesECGCzakirno19248Pas encore d'évaluation

- OPECDocument10 pagesOPECParnami KrishnaPas encore d'évaluation

- Transferwise Receipt 124257197Document2 pagesTransferwise Receipt 124257197Danilo Oliveira67% (3)

- CH 1 Basic ConceptsDocument6 pagesCH 1 Basic Conceptscaps videosPas encore d'évaluation

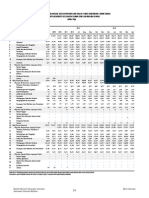

- I.8 Posisi Pinjaman Modal Kerja Rupiah Dan Valas Yang Diberikan Bank Umum Dan BPR Menurut Kelompok Bank Dan Lapangan Usaha (Miliar RP)Document2 pagesI.8 Posisi Pinjaman Modal Kerja Rupiah Dan Valas Yang Diberikan Bank Umum Dan BPR Menurut Kelompok Bank Dan Lapangan Usaha (Miliar RP)Izzuddin AbdurrahmanPas encore d'évaluation

- Alerts SummaryDocument31 pagesAlerts SummaryMau F-Marinay BadilloPas encore d'évaluation

- Eλλhnikη Δhmokpatia Republika Grčka Hellenic Republic Yпoypгeio Oikonomiaσ Ministarstvo Privrede I Ministry Of Economy & & Oikonomikωn Finansija FinanceDocument4 pagesEλλhnikη Δhmokpatia Republika Grčka Hellenic Republic Yпoypгeio Oikonomiaσ Ministarstvo Privrede I Ministry Of Economy & & Oikonomikωn Finansija FinanceIvanMiticPas encore d'évaluation

- Make in IndiaDocument10 pagesMake in IndiaRajeshsharmapurangPas encore d'évaluation

- Philippine Banking SystemDocument2 pagesPhilippine Banking SystemXytusPas encore d'évaluation

- Diskusi 2-Bahasa Inggris NiagaDocument2 pagesDiskusi 2-Bahasa Inggris NiagaDiah RaiPas encore d'évaluation

- Mba50 Wa4 Key 202223Document7 pagesMba50 Wa4 Key 202223serepasfPas encore d'évaluation

- BADM 580 (APS) - Conquistador Beer CaseDocument4 pagesBADM 580 (APS) - Conquistador Beer Caseedwarddudlik100% (1)

- Future of Manufacturing 2016Document1 pageFuture of Manufacturing 2016Jeremy KurnPas encore d'évaluation

- Reading in General Business - CompressedDocument90 pagesReading in General Business - CompressedMỹ QuyênPas encore d'évaluation

- Choppies PDFDocument29 pagesChoppies PDFjoe musiwaPas encore d'évaluation

- Elimination of Cascading Tax EffectDocument2 pagesElimination of Cascading Tax EffectHariharanPas encore d'évaluation

- Payroll ExampleDocument27 pagesPayroll ExampleYoni JonathanPas encore d'évaluation

- Earnings Statement: Benny D Oakley 11191 S. Wheeling Pike Fairmount IN 46928Document2 pagesEarnings Statement: Benny D Oakley 11191 S. Wheeling Pike Fairmount IN 46928mashaPas encore d'évaluation

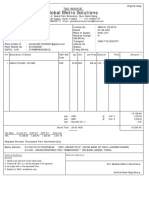

- Global Metro Solutions: Party DetailsDocument1 pageGlobal Metro Solutions: Party DetailsAashish PaulPas encore d'évaluation

- Formato de Fast Response (Version 09-21)Document53 pagesFormato de Fast Response (Version 09-21)francisco.rodolfo.martinez63Pas encore d'évaluation

- Indian Economy by Ramesh Singh 5th Edition Ramesh SinghDocument1 pageIndian Economy by Ramesh Singh 5th Edition Ramesh SinghVishnuvardhana SimhaPas encore d'évaluation

- Economic Reforms Since 1991Document12 pagesEconomic Reforms Since 1991Sampann KumarPas encore d'évaluation

- An Overview: M.O.P. Vaishnav College For WomenDocument6 pagesAn Overview: M.O.P. Vaishnav College For WomenThrisha_H_Shet_8391Pas encore d'évaluation

- Form 05 Cusdec Ro Blank App p1 p2Document3 pagesForm 05 Cusdec Ro Blank App p1 p2chamith.transcoPas encore d'évaluation

- 5 Forms of International Business - IbtDocument3 pages5 Forms of International Business - IbtGilbert CastroPas encore d'évaluation

- Indian Economy Statistics Know India BetterDocument3 pagesIndian Economy Statistics Know India BetterTarique FaridPas encore d'évaluation

- Ibt ReviewerDocument9 pagesIbt ReviewerCatherine AntineroPas encore d'évaluation

- Globalization PDFDocument20 pagesGlobalization PDFGeorge Villadolid100% (3)

- Cambridge IGCSE Business Studies 4th Edition © Hodder & Stoughton LTD 2013Document1 pageCambridge IGCSE Business Studies 4th Edition © Hodder & Stoughton LTD 2013RedrioxPas encore d'évaluation

- Agriculture Sector of PakistanDocument19 pagesAgriculture Sector of PakistanAsad viiPas encore d'évaluation