Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- No Excuses, Assume ResponsibilityDocument4 pagesNo Excuses, Assume ResponsibilityCristy Yaun-CabagnotPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- GOOSEBUMPS by Cristy Y. CabagnotDocument6 pagesGOOSEBUMPS by Cristy Y. CabagnotCristy Yaun-CabagnotPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Fashio: Ned Way: With My Own Hands AnDocument1 pageFashio: Ned Way: With My Own Hands AnCristy Yaun-CabagnotPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- G.R. No. 96016 October 17, 1991 Commissioner of Internal Revenue, Petitioner, vs. The Court of Appeals and Efren P. Castaneda, RespondentsDocument1 pageG.R. No. 96016 October 17, 1991 Commissioner of Internal Revenue, Petitioner, vs. The Court of Appeals and Efren P. Castaneda, RespondentsCristy Yaun-CabagnotPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Notes On EvidenceDocument6 pagesNotes On EvidenceCristy Yaun-Cabagnot100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- G.R. No. 137377 December 18, 2001 Commissioner of Internal Revenue, Petitioner, vs. MARUBENI CORPORATION, RespondentDocument11 pagesG.R. No. 137377 December 18, 2001 Commissioner of Internal Revenue, Petitioner, vs. MARUBENI CORPORATION, RespondentCristy Yaun-CabagnotPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Final SharesDocument1 pageFinal SharesCristy Yaun-CabagnotPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Honeste Vivere, Non Alterum Laedere Et Jus Suum Cuique Tribuere. To LiveDocument64 pagesHoneste Vivere, Non Alterum Laedere Et Jus Suum Cuique Tribuere. To LiveCristy Yaun-CabagnotPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Cir V Pascor Realty & Dev'T Corp Et. Al. GR No. 128315, June 29, 1999Document8 pagesCir V Pascor Realty & Dev'T Corp Et. Al. GR No. 128315, June 29, 1999Cristy Yaun-CabagnotPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Lending FormatDocument2 pagesLending FormatCristy Yaun-CabagnotPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- LOAN/s LOAN/s: TOTAL: - TOTALDocument1 pageLOAN/s LOAN/s: TOTAL: - TOTALCristy Yaun-CabagnotPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

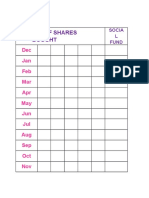

- No. of Shares Bought: Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct NovDocument2 pagesNo. of Shares Bought: Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct NovCristy Yaun-CabagnotPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Loan Record: Amount Loaned: Interest: Total Amount Payable: Signature: Date PaidDocument2 pagesLoan Record: Amount Loaned: Interest: Total Amount Payable: Signature: Date PaidCristy Yaun-CabagnotPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Allowable Deductions NotesDocument5 pagesAllowable Deductions NotesPaula Mae DacanayPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Pepsi Vs Municipality of TanauanDocument7 pagesPepsi Vs Municipality of TanauanKenmar NoganPas encore d'évaluation

- National Internal Revenue CodeDocument160 pagesNational Internal Revenue CodearchiesylPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Manila Electric Company v. City Assessor, G.R. No.166102Document53 pagesManila Electric Company v. City Assessor, G.R. No.166102Jerikka AcuñaPas encore d'évaluation

- Final Income Taxation: Catch-All For Item of Gross Income Not Subject To Final Tax and Capital Gains TaxDocument2 pagesFinal Income Taxation: Catch-All For Item of Gross Income Not Subject To Final Tax and Capital Gains Taxdaenielle reyesPas encore d'évaluation

- Tax Lecture Gross IncomeDocument6 pagesTax Lecture Gross IncomeAngelojason De LunaPas encore d'évaluation

- Issues in Philippine Fiscal AdministrationDocument8 pagesIssues in Philippine Fiscal AdministrationMIS Informal Settler FamiliesPas encore d'évaluation

- Personal Income TaxDocument31 pagesPersonal Income TaxRenese LeePas encore d'évaluation

- Topic 14 - Income and Business TaxationDocument71 pagesTopic 14 - Income and Business TaxationFrancez Anne Guanzon100% (1)

- Chapter 12 v2Document18 pagesChapter 12 v2Sheilamae Sernadilla GregorioPas encore d'évaluation

- C.T.A. Case No. 9076 - Keansburg Marketing Corp. v. CIRDocument31 pagesC.T.A. Case No. 9076 - Keansburg Marketing Corp. v. CIRcaren kay b. adolfoPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Manila Mandarin Hotels Vs CommissionerDocument2 pagesManila Mandarin Hotels Vs CommissionerEryl Yu100% (1)

- TAXDocument10 pagesTAXJeana Segumalian100% (3)

- PDF The Impact of Train Law in Micro Business On Sari-Sari Stores IncomeDocument68 pagesPDF The Impact of Train Law in Micro Business On Sari-Sari Stores IncomeRussel100% (2)

- Module 4 - Income TaxationDocument6 pagesModule 4 - Income TaxationLumbay, Jolly MaePas encore d'évaluation

- 1701 Annual Income Tax Return: Rogelio D. GonzalesDocument1 page1701 Annual Income Tax Return: Rogelio D. GonzalesJoshua CarzaPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Tax EvasionDocument2 pagesTax EvasionOkwuchi AlaukwuPas encore d'évaluation

- Cases On Taxation For Individualss AnswersDocument11 pagesCases On Taxation For Individualss AnswersMitchie Faustino100% (2)

- Principles of TaxationDocument32 pagesPrinciples of TaxationTyra Joyce Revadavia100% (1)

- En Banc Commissioner of Internal Revenue v. Northern Tobacco Redrying Co., Inc.Document11 pagesEn Banc Commissioner of Internal Revenue v. Northern Tobacco Redrying Co., Inc.Vince Lupango (imistervince)Pas encore d'évaluation

- Reply - ShowcauseDocument3 pagesReply - ShowcauseFarrukhPas encore d'évaluation

- Assignment No. 2: Part 1: Determination of Income Tax Due/PayableDocument4 pagesAssignment No. 2: Part 1: Determination of Income Tax Due/PayableKenneth Pimentel100% (1)

- Unnumbered BIR Ruling Dated November 21, 1996 - Memorandum For Commissioner - Inventory Write-OffDocument16 pagesUnnumbered BIR Ruling Dated November 21, 1996 - Memorandum For Commissioner - Inventory Write-OffGil PinoPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hello Tax Income Taxation True or FalseDocument51 pagesHello Tax Income Taxation True or FalseCassie ParkPas encore d'évaluation

- Individual TaxpayerDocument3 pagesIndividual TaxpayerJovie Ann RamiloPas encore d'évaluation

- Accenture Inc. V Commissioner of Internal Revenue G.R. No. 190102Document10 pagesAccenture Inc. V Commissioner of Internal Revenue G.R. No. 190102Gerard Sta. CruzPas encore d'évaluation

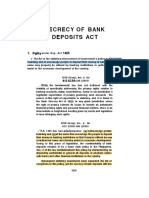

- Secrecy of Bank DepositsDocument8 pagesSecrecy of Bank DepositsCyrine CalagosPas encore d'évaluation

- TAX - LEAD BATCH 3 - Preweek 2Document13 pagesTAX - LEAD BATCH 3 - Preweek 2Josiah ZeusPas encore d'évaluation

- JASF Template English Jan2022Document12 pagesJASF Template English Jan2022Rizky Rizky NurdiansyahPas encore d'évaluation

- Taxation Midterm ReviewerDocument12 pagesTaxation Midterm ReviewerJerico GodoyPas encore d'évaluation

- How to get US Bank Account for Non US ResidentD'EverandHow to get US Bank Account for Non US ResidentÉvaluation : 5 sur 5 étoiles5/5 (1)