Vous aimerez peut-être aussi

- New Microsoft Office Word DocumentDocument50 pagesNew Microsoft Office Word Documentkanchanagrawal91Pas encore d'évaluation

- Insurance LawDocument110 pagesInsurance LawfarhatxdaPas encore d'évaluation

- IRDA Recruitment Assistant Managers 2017 - Official NotificationDocument28 pagesIRDA Recruitment Assistant Managers 2017 - Official NotificationKshitija100% (1)

- Quantitative Easing (QE) Is An UnconventionalDocument16 pagesQuantitative Easing (QE) Is An Unconventionalkanchanagrawal91Pas encore d'évaluation

- Net Sales Gross Sales - (Returns and Allowances)Document11 pagesNet Sales Gross Sales - (Returns and Allowances)kanchanagrawal91Pas encore d'évaluation

- LIFE INSURANCE PRINCIPLESDocument9 pagesLIFE INSURANCE PRINCIPLESMadz MadrastoPas encore d'évaluation

- The Hindu Review August 2017Document23 pagesThe Hindu Review August 2017kanchanagrawal91Pas encore d'évaluation

- University Topper ListDocument51 pagesUniversity Topper Listkanchanagrawal91Pas encore d'évaluation

- AccountingDocument3 pagesAccountingkanchanagrawal91Pas encore d'évaluation

- Vault-Finance Practice GuideDocument126 pagesVault-Finance Practice GuideMohit Sharma100% (1)

- Feel GoodDocument1 pageFeel Goodkanchanagrawal91Pas encore d'évaluation

- Basic of Accounting Principles PDFDocument23 pagesBasic of Accounting Principles PDFMani KandanPas encore d'évaluation

- Support Material On Writing Skills - For XAT, TISS, FMS EtcDocument54 pagesSupport Material On Writing Skills - For XAT, TISS, FMS EtcakashPas encore d'évaluation

- Event Management - II (Case Study)Document22 pagesEvent Management - II (Case Study)swathrav100% (1)

- Ibps RRB (Group - A Officers) ExamDocument33 pagesIbps RRB (Group - A Officers) ExamSrinivas GoudPas encore d'évaluation

- Brutal SCDocument22 pagesBrutal SCbestboy_vijayPas encore d'évaluation

- Event Management - II (Case Study)Document22 pagesEvent Management - II (Case Study)swathrav100% (1)

- TISS Sample Paper - MA Part 1 & 2 Combined - 2009-11Document56 pagesTISS Sample Paper - MA Part 1 & 2 Combined - 2009-11bhustlero0oPas encore d'évaluation

- Brutal SCDocument22 pagesBrutal SCbestboy_vijayPas encore d'évaluation

- DebateDocument8 pagesDebatekanchanagrawal91Pas encore d'évaluation

- OSI 7 Layers Reference Model For Network CommunicationDocument18 pagesOSI 7 Layers Reference Model For Network Communicationkanchanagrawal91Pas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- BUCKS CONCRETE & PAVERS INC - AmTrust Workers' Compensation PolicyDocument37 pagesBUCKS CONCRETE & PAVERS INC - AmTrust Workers' Compensation PolicyYvette BroadwaterPas encore d'évaluation

- Ls 208Document1 pageLs 208El CapitánPas encore d'évaluation

- Department of Labor: kwc120 (Rev-04-02)Document26 pagesDepartment of Labor: kwc120 (Rev-04-02)USA_DepartmentOfLaborPas encore d'évaluation

- Summary-AHM 510 PDFDocument70 pagesSummary-AHM 510 PDFSiddhartha KalasikamPas encore d'évaluation

- ECC Case DigestsDocument9 pagesECC Case DigestsJohn Michael CamposPas encore d'évaluation

- PFR-Franklin Baker Vs AlillanaDocument5 pagesPFR-Franklin Baker Vs Alillanabam112190Pas encore d'évaluation

- 1994 BAR NO - XX:: Ibid., Pp. 613-614Document5 pages1994 BAR NO - XX:: Ibid., Pp. 613-614poiuytrewq9115Pas encore d'évaluation

- Summary of Court Convictions - WorkSafeBC - 1996-2011 Cases Completed 1996 To 2011Document86 pagesSummary of Court Convictions - WorkSafeBC - 1996-2011 Cases Completed 1996 To 2011The Vancouver SunPas encore d'évaluation

- Compensation ManagementDocument212 pagesCompensation ManagementSyed Adil Hussain100% (1)

- Edgar Eugene Black v. Texas Employers Insurance Association, 326 F.2d 603, 10th Cir. (1964)Document4 pagesEdgar Eugene Black v. Texas Employers Insurance Association, 326 F.2d 603, 10th Cir. (1964)Scribd Government DocsPas encore d'évaluation

- Construction MGT L5 - InclusiveDocument93 pagesConstruction MGT L5 - InclusiveFenta Dejene100% (2)

- Work Comp C4Document5 pagesWork Comp C4ijustwanawritePas encore d'évaluation

- T P. Din 110 S S C A, N Y 12236: A. Results of ExaminationDocument6 pagesT P. Din 110 S S C A, N Y 12236: A. Results of ExaminationjspectorPas encore d'évaluation

- Three Parts of Workers Compensation InsuranceDocument13 pagesThree Parts of Workers Compensation InsuranceeldhobehananPas encore d'évaluation

- IBRDocument37 pagesIBRravirawat15Pas encore d'évaluation

- Worker's Compensation LawsDocument19 pagesWorker's Compensation LawsSadaqat KhanPas encore d'évaluation

- Social Security Benefits PESSIDocument38 pagesSocial Security Benefits PESSIpakistanzindabadPas encore d'évaluation

- Client Intake ManualDocument21 pagesClient Intake Manualdwrighte175% (4)

- Labour Law-II Second WeekDocument28 pagesLabour Law-II Second WeekAkanksha BohraPas encore d'évaluation

- Raymond Feifer, Nicholas Pocchia, and Edwin Molina v. Prudential Insurance Company of America, Daily News, L.P., and Daily News, L.P. Benefits Program, 306 F.3d 1202, 2d Cir. (2002)Document16 pagesRaymond Feifer, Nicholas Pocchia, and Edwin Molina v. Prudential Insurance Company of America, Daily News, L.P., and Daily News, L.P. Benefits Program, 306 F.3d 1202, 2d Cir. (2002)Scribd Government DocsPas encore d'évaluation

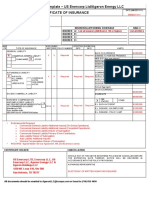

- Sample COI Template - US Enercorp Ltd/Ageron Energy LLC Certificate of InsuranceDocument1 pageSample COI Template - US Enercorp Ltd/Ageron Energy LLC Certificate of InsuranceMohamed Ashraf SolimanPas encore d'évaluation

- 2nd Semester Notes in Torts-2Document28 pages2nd Semester Notes in Torts-2Venugopal MantraratnamPas encore d'évaluation

- IT Managed Support Services ProposalDocument8 pagesIT Managed Support Services ProposalRicky ChanPas encore d'évaluation

- General Safety ManualDocument17 pagesGeneral Safety Manualrung_na_uy2011100% (1)

- HRM Practice of Square Textile LTDDocument32 pagesHRM Practice of Square Textile LTDapi-371549380% (20)

- Fayetteville School Board Agenda For Dec. 16, 2010Document44 pagesFayetteville School Board Agenda For Dec. 16, 2010Ozarks UnboundPas encore d'évaluation

- Ellipse 63 Full Course Catalogue 2Document79 pagesEllipse 63 Full Course Catalogue 2Aniruddha NathPas encore d'évaluation

- Contract Terms GuideDocument12 pagesContract Terms GuideNadir ShahPas encore d'évaluation

- Dcom207 Labour Laws PDFDocument252 pagesDcom207 Labour Laws PDFshwetamolly04Pas encore d'évaluation

- OPTCL Technical SpecificationDocument751 pagesOPTCL Technical Specificationsrimant patel100% (1)