Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Deductions Under Income Tax ActDocument39 pagesDeductions Under Income Tax ActbhavdeepsinhPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- A Project Report On Group InsuranceDocument64 pagesA Project Report On Group Insurancesharinair1393% (15)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- PageGroup Salary Guide 2023 Switzerland enDocument40 pagesPageGroup Salary Guide 2023 Switzerland enMr StrangerPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Disciplinary Proceedings To Impose Minor Penalty and Retirement of Government ServantDocument2 pagesDisciplinary Proceedings To Impose Minor Penalty and Retirement of Government ServantRaghavPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Corporate Governance Complete ProjectDocument21 pagesCorporate Governance Complete ProjectEswar Stark100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Wa0001Document116 pagesWa0001Karthik Keyan100% (1)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Mondo Condo Makeover A Looming Nightmare For UFCWDocument10 pagesMondo Condo Makeover A Looming Nightmare For UFCWWanda PaszPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- International Estate & Inheritance Tax Guide (Ernst&Young-2012)Document276 pagesInternational Estate & Inheritance Tax Guide (Ernst&Young-2012)JohnWWPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Finance HSC Business NotesDocument32 pagesFinance HSC Business NoteschloePas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

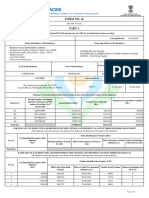

- Form16 Mar 2019 PDFDocument9 pagesForm16 Mar 2019 PDFManish Kumar SinghPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Deve 60398Document7 pagesDeve 60398Devesh Pratap ChandPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Service ConditionsDocument181 pagesService ConditionsAnonymous UDTfkXFPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- p2014 FSI 01final ReportDocument350 pagesp2014 FSI 01final Reportalt.xq-2twvdr2Pas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Insurance Companies and Pension Funds: All Rights ReservedDocument46 pagesInsurance Companies and Pension Funds: All Rights Reservednadeem.aftab1177Pas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Summary: Intervention and Options: Impact Assessment (IA)Document9 pagesSummary: Intervention and Options: Impact Assessment (IA)Edward SuarezPas encore d'évaluation

- PFR CasesDocument102 pagesPFR CasesEran Martin KimayongPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Strategic Staffing Planning & ProcessDocument25 pagesThe Strategic Staffing Planning & ProcessGhazalPas encore d'évaluation

- The National Pension Reform and Its Benefits To The Ghanaian WorkerDocument19 pagesThe National Pension Reform and Its Benefits To The Ghanaian WorkerJosephine FrempongPas encore d'évaluation

- SOCIAL WELFARE - Vulnerable SectorsDocument8 pagesSOCIAL WELFARE - Vulnerable SectorsLizzette Dela PenaPas encore d'évaluation

- Retirement Under The Labor CodeDocument14 pagesRetirement Under The Labor CodeSam ConcepcionPas encore d'évaluation

- CMA MCQ Self Entrance-1Document2 pagesCMA MCQ Self Entrance-1Ava DasPas encore d'évaluation

- Acct 428 - HW 7Document3 pagesAcct 428 - HW 7Shaikh GufranPas encore d'évaluation

- SparshDocument13 pagesSparshIFA DSSC100% (1)

- Assignment - Explain Income From Other SourcesDocument9 pagesAssignment - Explain Income From Other SourcesPraveen SPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- "Salary", "Perquisite" and "Profits in Lieu of Salary" Defined. 17Document5 pages"Salary", "Perquisite" and "Profits in Lieu of Salary" Defined. 17vineet_agrawal_ca2574Pas encore d'évaluation

- Revised SAIL TA RulesDocument15 pagesRevised SAIL TA RulesgntdocPas encore d'évaluation

- Financial Statement Analysis: Charles H. GibsonDocument30 pagesFinancial Statement Analysis: Charles H. GibsonAmutha RamasamyPas encore d'évaluation

- Bajaj Allianz Life Insurance Company.Document19 pagesBajaj Allianz Life Insurance Company.HaniaSadia100% (1)

- MCQ For RBI Grade BDocument30 pagesMCQ For RBI Grade Bsaurabhmakta100% (2)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Abstract of Labour LawsDocument4 pagesAbstract of Labour LawsVishwesh KoundilyaPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)