Vous aimerez peut-être aussi

- Project On e Filing Income Tax Return OnlineDocument60 pagesProject On e Filing Income Tax Return Onlineadeol5012100% (1)

- Income Tax Planning in India With Respect To Individual Assessee MBA Project - 215080540Document90 pagesIncome Tax Planning in India With Respect To Individual Assessee MBA Project - 215080540Naveen Kumar67% (3)

- A Project Report On Taxation in IndiaDocument59 pagesA Project Report On Taxation in IndiaYash Bhagat100% (1)

- Income Tax ProjectDocument58 pagesIncome Tax ProjectSuhas YadavPas encore d'évaluation

- E-Filing of Returns: Live ProjectDocument60 pagesE-Filing of Returns: Live ProjectAnshu LalitPas encore d'évaluation

- A Project Report On Direct TaxDocument44 pagesA Project Report On Direct Taxrani26oct100% (2)

- Income Tax Plannig in India With Respectred To Individual AssesseeDocument79 pagesIncome Tax Plannig in India With Respectred To Individual AssesseeSAJIDA SHAIKHPas encore d'évaluation

- Awareness On e Filing and Tax Returns PDFDocument51 pagesAwareness On e Filing and Tax Returns PDFVijaykumar ChalwadiPas encore d'évaluation

- Black BookDocument45 pagesBlack Bookamrit thakur50% (2)

- Presentaton On Review of LiteratureDocument27 pagesPresentaton On Review of LiteraturearchitPas encore d'évaluation

- Income Tax ReturnDocument96 pagesIncome Tax ReturnKapil SalujaPas encore d'évaluation

- DARSHAN P Project Report On TAX PAYERS PERSEPTION TOWARDS E - FILING SYSTEM OF INCOME TAX" (IN CASE STUDY OF BELLARI CITY)Document73 pagesDARSHAN P Project Report On TAX PAYERS PERSEPTION TOWARDS E - FILING SYSTEM OF INCOME TAX" (IN CASE STUDY OF BELLARI CITY)DARSHAN PPas encore d'évaluation

- Neha K CLG MBA Proj - Itr - CompressedDocument47 pagesNeha K CLG MBA Proj - Itr - CompressedNeha Sathaye100% (1)

- A Synopsis ON "Study On Tax Planning of 10 Assesses"Document6 pagesA Synopsis ON "Study On Tax Planning of 10 Assesses"hemant100% (1)

- Effect of Taxation On Small BusinessDocument37 pagesEffect of Taxation On Small BusinessBhanu pratap singh100% (1)

- Consumer Perception Towards GSTDocument82 pagesConsumer Perception Towards GSTsakshi100% (2)

- Chapter 5 Int TaxDocument9 pagesChapter 5 Int TaxBhavana GadagPas encore d'évaluation

- Report On IMPACT OF GST ON REAL ESTATE INDUSTRYDocument31 pagesReport On IMPACT OF GST ON REAL ESTATE INDUSTRYsamPas encore d'évaluation

- Various Type of Heads of IncomeDocument76 pagesVarious Type of Heads of Incomejesal makwana100% (1)

- Good and Service Tax"Document37 pagesGood and Service Tax"yash saharePas encore d'évaluation

- A STUDY OF PERCEPTION OF TAXPAYERS TOWARDS NewDocument41 pagesA STUDY OF PERCEPTION OF TAXPAYERS TOWARDS NewVijaykumar ChalwadiPas encore d'évaluation

- Tax Planning For Salaried IndividualsDocument7 pagesTax Planning For Salaried IndividualspilluPas encore d'évaluation

- Sip Report (1) All India ITRDocument67 pagesSip Report (1) All India ITRGagan BhatiaPas encore d'évaluation

- Tata Motors Nano To Roll OutDocument4 pagesTata Motors Nano To Roll OutSymon StefenPas encore d'évaluation

- Epzs, Eous, Tps and SezsDocument23 pagesEpzs, Eous, Tps and Sezssachin patel100% (1)

- Final Project With FindingsDocument51 pagesFinal Project With FindingsDivya PatelPas encore d'évaluation

- Summer Internship ReportDocument47 pagesSummer Internship ReportBijal Mehta43% (7)

- A Study On Awareness of GST Among College Students in MumbaiDocument56 pagesA Study On Awareness of GST Among College Students in Mumbaisameep gourPas encore d'évaluation

- QB - Indirect Tax - Mcom Sem 4Document5 pagesQB - Indirect Tax - Mcom Sem 4Prathmesh KadamPas encore d'évaluation

- Review of LiteratureDocument8 pagesReview of LiteratureNehaPas encore d'évaluation

- Project On GSTDocument3 pagesProject On GSTkismat yadav50% (2)

- Introducing GST and Its Impact On Indian EconomyDocument210 pagesIntroducing GST and Its Impact On Indian EconomyJ100% (1)

- Impact of GST On Gold Purchase - Devika UnniDocument55 pagesImpact of GST On Gold Purchase - Devika UnniAthul G100% (1)

- Hotel Industry Project Work DoneDocument101 pagesHotel Industry Project Work DoneShreya Poojari0% (1)

- 03 - Review of Litreature On GSTDocument10 pages03 - Review of Litreature On GSTAnonymous u9mzfWNF80% (10)

- Comparative Analysis On NBFC & Banks NPADocument33 pagesComparative Analysis On NBFC & Banks NPABHAVESH KHOMNEPas encore d'évaluation

- Black Book PDFDocument69 pagesBlack Book PDFdhwani100% (1)

- Corporate Tax PlanningDocument85 pagesCorporate Tax PlanningLavi KambojPas encore d'évaluation

- Mcom Part 2 Project of Mvat Cen VatDocument53 pagesMcom Part 2 Project of Mvat Cen Vatrani26oct100% (4)

- Final Mcom ProjectDocument47 pagesFinal Mcom ProjectGautamChakrabortyPas encore d'évaluation

- Unit 2 Talent ManagementDocument42 pagesUnit 2 Talent Managementshaifali chauhanPas encore d'évaluation

- Final Project Report On Tax Planning PDFDocument67 pagesFinal Project Report On Tax Planning PDFAniket ChavanPas encore d'évaluation

- A Study of Impact of GST On Hospitality & Travel and Tourism Industry - BHAKTI NISHAR TDAF026CDocument66 pagesA Study of Impact of GST On Hospitality & Travel and Tourism Industry - BHAKTI NISHAR TDAF026Csanu duttaPas encore d'évaluation

- Sip Project ReportDocument29 pagesSip Project ReportAAKIB HAMDANIPas encore d'évaluation

- A Comparative Study of NBFC in IndiaDocument28 pagesA Comparative Study of NBFC in IndiaGuru Prasad0% (1)

- Introduction of RbiDocument63 pagesIntroduction of RbiAshley BakerPas encore d'évaluation

- Project Report On Financial InstitutionDocument86 pagesProject Report On Financial Institutionarchana_anuragi83% (6)

- Impact of GST On Small and Medium EnterprisesDocument5 pagesImpact of GST On Small and Medium Enterprisesarcherselevators0% (2)

- Project Report - On The Job - SWMCDocument30 pagesProject Report - On The Job - SWMCRashiPas encore d'évaluation

- Project ReportDocument24 pagesProject ReportanilPas encore d'évaluation

- Synopsis On GSTDocument9 pagesSynopsis On GSTsamiullah100% (1)

- Taxation Planning For Individual A Y 2014-15Document77 pagesTaxation Planning For Individual A Y 2014-15MitaliPatilPas encore d'évaluation

- Taxation - Business and ProfessionDocument45 pagesTaxation - Business and ProfessionSanah Bijlani67% (3)

- Project Report On "Types of Allowances and Their Permissible LimitsDocument34 pagesProject Report On "Types of Allowances and Their Permissible LimitsPooja Jain100% (1)

- Tax Planning For SalaryDocument31 pagesTax Planning For SalaryAjit SwainPas encore d'évaluation

- Project Report Sem IV - Tax Planning in IndiaDocument62 pagesProject Report Sem IV - Tax Planning in IndiaRahul SinghPas encore d'évaluation

- Financial Planning For Salaried Employee and Strategies For Tax SavingsDocument8 pagesFinancial Planning For Salaried Employee and Strategies For Tax SavingsNivetha0% (2)

- Regional Rural Banks of India: Evolution, Performance and ManagementD'EverandRegional Rural Banks of India: Evolution, Performance and ManagementPas encore d'évaluation

- Project Report On TaxationDocument51 pagesProject Report On Taxationanuragmishra211276% (38)

- Income Tax Planning in IndiaDocument61 pagesIncome Tax Planning in IndiaPRIYANKA LANDGEPas encore d'évaluation

- Chapter 1: Introduction To GSTDocument3 pagesChapter 1: Introduction To GSTsnehalPas encore d'évaluation

- Chapter 1: Introduction To GSTDocument3 pagesChapter 1: Introduction To GSTsnehalPas encore d'évaluation

- Chapter 1: Introduction To GSTDocument3 pagesChapter 1: Introduction To GSTsnehalPas encore d'évaluation

- Project Report On Direct Tax (5 Heads of Income Tax)Document42 pagesProject Report On Direct Tax (5 Heads of Income Tax)Sagar Zine67% (39)

- Chapter 10 - Allowable Deductions: IndividualDocument17 pagesChapter 10 - Allowable Deductions: IndividualKyle BacaniPas encore d'évaluation

- Toronto Police Service Sunshine List 2012Document94 pagesToronto Police Service Sunshine List 2012CynthiaMcLeodSunPas encore d'évaluation

- Employee HandbookDocument44 pagesEmployee HandbookKhizar ShaikhPas encore d'évaluation

- BB0019-IncomeTax Valuation PerquisitesDocument314 pagesBB0019-IncomeTax Valuation PerquisitesMohammed Abu ObaidahPas encore d'évaluation

- Exam Content Outline: Certifications in Human ResourcesDocument18 pagesExam Content Outline: Certifications in Human ResourcesMuhammad Akmal HossainPas encore d'évaluation

- IAS 19 Employee BenefitsDocument14 pagesIAS 19 Employee BenefitsShiza ArifPas encore d'évaluation

- Benefits BookletDocument59 pagesBenefits BookletThe QuadfatherPas encore d'évaluation

- File 6 Unit С Work and motivationDocument10 pagesFile 6 Unit С Work and motivationРодион ЛучнойPas encore d'évaluation

- Summary Tax ManagementDocument15 pagesSummary Tax Managementfarhan100% (1)

- OPEX Budget Guidelines.2017Document13 pagesOPEX Budget Guidelines.2017Mark BuendiaPas encore d'évaluation

- Examples of Inadmissible Expenses and Admissible ExpensesDocument3 pagesExamples of Inadmissible Expenses and Admissible ExpensesBhuvaneswari karuturi100% (4)

- Twelve: Human Resource Managemen TDocument40 pagesTwelve: Human Resource Managemen TBlue StandyPas encore d'évaluation

- Digital School Management Systems - For Emerging AfricaDocument83 pagesDigital School Management Systems - For Emerging AfricaKosi Emmanuel Chukwujindu50% (2)

- Cape Cod and Hyannis Railroad Inc. - Anatomy of An 03 Account - June 1989Document15 pagesCape Cod and Hyannis Railroad Inc. - Anatomy of An 03 Account - June 1989ffm784Pas encore d'évaluation

- Group 4: Salary Computation Per Year (Rate of Increase) : 10% Every 6 MonthsDocument5 pagesGroup 4: Salary Computation Per Year (Rate of Increase) : 10% Every 6 MonthsCamille SaltarinPas encore d'évaluation

- Paid Sick Leave MemoDocument4 pagesPaid Sick Leave Memodharry8108Pas encore d'évaluation

- 8531 1uniDocument18 pages8531 1uniMs AimaPas encore d'évaluation

- AriseDocument21 pagesArisearjunparekh100% (6)

- LNL Iklcqd /: Employee Share Employer Share Employee Share Employer ShareDocument3 pagesLNL Iklcqd /: Employee Share Employer Share Employee Share Employer ShareMadhusmita MishraPas encore d'évaluation

- Muthoot Finace Annual Report 2013Document68 pagesMuthoot Finace Annual Report 2013aayush13Pas encore d'évaluation

- Non Diminution of BenefitDocument3 pagesNon Diminution of BenefitBonito BulanPas encore d'évaluation

- Tax FinalDocument7 pagesTax FinalDinosaur KoreanPas encore d'évaluation

- Solved, MU0015 Compensation BenefitsDocument6 pagesSolved, MU0015 Compensation BenefitsArvind KPas encore d'évaluation

- ATP Oil First Day Declaration Company CFODocument38 pagesATP Oil First Day Declaration Company CFOChapter 11 DocketsPas encore d'évaluation

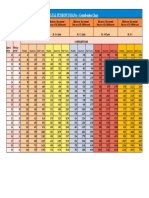

- Apy Chart PDFDocument1 pageApy Chart PDFDeep Kumar0% (1)

- HR Induction Powerpoint Presentation SlidesDocument53 pagesHR Induction Powerpoint Presentation SlidesVivek SubburamanPas encore d'évaluation

- HRM Plan of GrameenPhoneDocument19 pagesHRM Plan of GrameenPhoneSakif Ryhan100% (1)

- DIRECT TAX I Bharathiar University B.com PADocument78 pagesDIRECT TAX I Bharathiar University B.com PAkalpanaPas encore d'évaluation

- Idbi Federal LifeDocument67 pagesIdbi Federal LifeSangeetha Venugopal33% (3)

- VOYA USG Accident-Hospital IndemnityDocument37 pagesVOYA USG Accident-Hospital IndemnityDavid BriggsPas encore d'évaluation