Vous aimerez peut-être aussi

- Medical Aspects of Fitness For Offshore Work PDFDocument22 pagesMedical Aspects of Fitness For Offshore Work PDFParth DM100% (1)

- LG OLED55C7P CNET Review Calibration ResultsDocument3 pagesLG OLED55C7P CNET Review Calibration ResultsDavid KatzmaierPas encore d'évaluation

- Forecast For US Oil and Gas Production (Laherrère & Hall 2018)Document24 pagesForecast For US Oil and Gas Production (Laherrère & Hall 2018)Cliffhanger100% (3)

- Oil From A Critical Raw Material Perspective - Geological Survey of Finland (GTK) (12/22/19)Document510 pagesOil From A Critical Raw Material Perspective - Geological Survey of Finland (GTK) (12/22/19)CliffhangerPas encore d'évaluation

- As G Kuala LumpurDocument23 pagesAs G Kuala LumpurYawanda Andhika PutraPas encore d'évaluation

- Trinidad and Tobago diversification-KBenjamin - DSinanan - CORM - 2012Document20 pagesTrinidad and Tobago diversification-KBenjamin - DSinanan - CORM - 2012jefferyleclercPas encore d'évaluation

- Production of U.S. Crude Oil and Natural Gas Plant LiquidsDocument7 pagesProduction of U.S. Crude Oil and Natural Gas Plant LiquidsCarlos RorizPas encore d'évaluation

- Residual Plots For Yield: Normal Probability Plot Versus FitsDocument3 pagesResidual Plots For Yield: Normal Probability Plot Versus FitsBablu KumarPas encore d'évaluation

- Assignment 4Document69 pagesAssignment 4amy ackerPas encore d'évaluation

- Israeli Economy: GDP Growth, Exports, Labor Market Trends and Financial ReformsDocument39 pagesIsraeli Economy: GDP Growth, Exports, Labor Market Trends and Financial ReformsAqib JavedPas encore d'évaluation

- Condition: Technical Service BulletinDocument22 pagesCondition: Technical Service BulletinOleksiy OsiychukPas encore d'évaluation

- Merak Fiscal Model Library: Bangladesh PSC (1993)Document2 pagesMerak Fiscal Model Library: Bangladesh PSC (1993)Tripoli ManoPas encore d'évaluation

- Baltic Exchange Presentation 09-13-2021Document26 pagesBaltic Exchange Presentation 09-13-2021JackPas encore d'évaluation

- Forecast Simulation: Input Value Base ForecastDocument6 pagesForecast Simulation: Input Value Base ForecastcpbdumwPas encore d'évaluation

- Macrovoices October 1, 2020: Slide 1 Labyrinth Consulting Services, IncDocument13 pagesMacrovoices October 1, 2020: Slide 1 Labyrinth Consulting Services, IncBlasPas encore d'évaluation

- Engineering Safety: Going Lower - Reducing Risk, Enhancing ProjectsDocument58 pagesEngineering Safety: Going Lower - Reducing Risk, Enhancing ProjectsHedi Ben MohamedPas encore d'évaluation

- 2000-03-24 An Overview of Internet Valuation - Is The Internet A Bubble Waiting To Burst?Document37 pages2000-03-24 An Overview of Internet Valuation - Is The Internet A Bubble Waiting To Burst?Jerry LeePas encore d'évaluation

- The Boston Beer CompanyDocument52 pagesThe Boston Beer CompanyLarsPas encore d'évaluation

- Introduction To: Cost of UalityDocument29 pagesIntroduction To: Cost of UalitySaad ParachaPas encore d'évaluation

- Tenaris Investors Presentation Mar 2017 Howard Weil Mar 27 2017Document12 pagesTenaris Investors Presentation Mar 2017 Howard Weil Mar 27 2017Roulettista CoinistaPas encore d'évaluation

- Cópia de Unidades 2005 - Brakes LimeiraDocument15 pagesCópia de Unidades 2005 - Brakes LimeiraamaralabPas encore d'évaluation

- EVA Acctg Adjustments YoungDocument64 pagesEVA Acctg Adjustments YoungKarya BangunanPas encore d'évaluation

- Chapter One: Management Science Break-Even AnalysisDocument5 pagesChapter One: Management Science Break-Even AnalysisDexter Joseph CuevasPas encore d'évaluation

- Bio-Fuels: The BackdropDocument22 pagesBio-Fuels: The Backdropjivitesh YadavPas encore d'évaluation

- 164B Shale DeckDocument16 pages164B Shale DeckIman NasseriPas encore d'évaluation

- Unconventional Reservoir Future: Science, Technology and EconomicsDocument51 pagesUnconventional Reservoir Future: Science, Technology and EconomicsSmail KechamPas encore d'évaluation

- Approved Oils Mack Mdrive TransmissionsDocument4 pagesApproved Oils Mack Mdrive TransmissionsDavid PomaPas encore d'évaluation

- Petroleum and Other LiquidsDocument18 pagesPetroleum and Other LiquidsSCAP SADECVPas encore d'évaluation

- Oil Approval List 2023 MC-10209265-0001Document32 pagesOil Approval List 2023 MC-10209265-0001Lemont 3vPas encore d'évaluation

- API Base Oil Groups and Lubricant ApplicationsDocument5 pagesAPI Base Oil Groups and Lubricant ApplicationsAbdul GhafoorPas encore d'évaluation

- Texas PriceDocument1 pageTexas PricecnomegaPas encore d'évaluation

- Major Upcoming Upstream Projects NigeriaDocument1 pageMajor Upcoming Upstream Projects NigeriaZvonko BosnjakPas encore d'évaluation

- Factsheet NY ALVDocument2 pagesFactsheet NY ALVAnkit JoshiPas encore d'évaluation

- Merak Fiscal Model Library: Kurdistan PSC (2006)Document2 pagesMerak Fiscal Model Library: Kurdistan PSC (2006)Libya TripoliPas encore d'évaluation

- Fundamental Analysis by COL FInancialDocument43 pagesFundamental Analysis by COL FInancialroksimalsPas encore d'évaluation

- Indonesia Economic Outlook 2018 - KEB Hana BankDocument31 pagesIndonesia Economic Outlook 2018 - KEB Hana Bankmeiji_99Pas encore d'évaluation

- Cost Report ContohDocument24 pagesCost Report ContohagungPas encore d'évaluation

- In Thousands of USD: Lightspeed ForecastDocument15 pagesIn Thousands of USD: Lightspeed ForecastAmy TruongPas encore d'évaluation

- Crude Oil Refining ExplainedDocument33 pagesCrude Oil Refining ExplainedgustavoemirPas encore d'évaluation

- PN Co PresentationDocument57 pagesPN Co PresentationFernando De Juan Ruíz-Montalvo Perez de AragónPas encore d'évaluation

- Reservoir Drive MechanismsDocument30 pagesReservoir Drive Mechanismszeeshan tanOli (shani)Pas encore d'évaluation

- Corrosion Resistant Materials 02Document85 pagesCorrosion Resistant Materials 02Anonymous NxpnI6jCPas encore d'évaluation

- Design and Operation of LPG ShipsDocument476 pagesDesign and Operation of LPG Shipsashwani chandraPas encore d'évaluation

- Fuels and Lubricants June 2015Document38 pagesFuels and Lubricants June 2015tollywhistlePas encore d'évaluation

- Gulf Oil Marine - Product RangeDocument8 pagesGulf Oil Marine - Product RangeObydur RahmanPas encore d'évaluation

- Emerging From The Downturn: A New Business Environment For Refining?Document16 pagesEmerging From The Downturn: A New Business Environment For Refining?Lindsey BondPas encore d'évaluation

- ATPL TestDocument17 pagesATPL TestJosh BullasPas encore d'évaluation

- MBA RM I 2021 2023 UpdatedDocument2 pagesMBA RM I 2021 2023 UpdatedYASH BHOJWANIPas encore d'évaluation

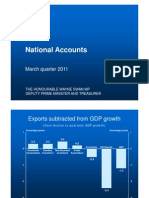

- National Accounts National Accounts: March Quarter 2011Document6 pagesNational Accounts National Accounts: March Quarter 2011api-64584013Pas encore d'évaluation

- Fuel SystemDocument45 pagesFuel SystemMelwyn FernandesPas encore d'évaluation

- 818 Paleogeotherm 1Document1 page818 Paleogeotherm 1hamed1725Pas encore d'évaluation

- Eicher Motors LTD: DCF Analysis Valuation Date: 13 March, 2019Document60 pagesEicher Motors LTD: DCF Analysis Valuation Date: 13 March, 2019CharanjitPas encore d'évaluation

- Reservoir Performance FactorsDocument329 pagesReservoir Performance Factorsjazhman100% (1)

- Octane Benefits: Mobile Source Technical Review SubcommiteeDocument16 pagesOctane Benefits: Mobile Source Technical Review SubcommiteeAnonymous QqyLDoW1Pas encore d'évaluation

- Oil Lecture on Exploration, Development, and ProductionDocument18 pagesOil Lecture on Exploration, Development, and ProductionyemiPas encore d'évaluation

- Volvo Oil Brand EquityDocument13 pagesVolvo Oil Brand EquityMohamed Ahmed HassaninPas encore d'évaluation

- LG OLED65E7P CNET Review Calibration ResultsDocument3 pagesLG OLED65E7P CNET Review Calibration ResultsDavid KatzmaierPas encore d'évaluation

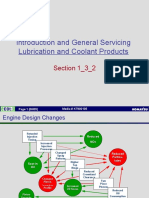

- Lube Coolant ProductsDocument10 pagesLube Coolant ProductsRohmanPas encore d'évaluation

- How Charts Can Make You Money: An Investor’s Guide to Technical AnalysisD'EverandHow Charts Can Make You Money: An Investor’s Guide to Technical AnalysisPas encore d'évaluation

- Corbion Whitepaper Feedstock Sourcing 11Document17 pagesCorbion Whitepaper Feedstock Sourcing 11Parth DMPas encore d'évaluation

- Strong Industry Performance Continues As Profits Rise Despite Declining SalesDocument6 pagesStrong Industry Performance Continues As Profits Rise Despite Declining SalesParth DMPas encore d'évaluation

- 25k Bop FlyerDocument1 page25k Bop FlyersyedainahmadPas encore d'évaluation

- Building Workforce Models - 0Document20 pagesBuilding Workforce Models - 0Parth DMPas encore d'évaluation

- BCG Specialty Chemical Distribution Market Update Apr 2014 Tcm80-158064Document16 pagesBCG Specialty Chemical Distribution Market Update Apr 2014 Tcm80-158064Parth DMPas encore d'évaluation

- Workforce Planning ModelDocument27 pagesWorkforce Planning ModelParth DM100% (1)

- Roland Berger Global Automotive Supplier Study 2018Document86 pagesRoland Berger Global Automotive Supplier Study 2018Parth DMPas encore d'évaluation

- Rightmove House Price Index 16 September London 2019Document6 pagesRightmove House Price Index 16 September London 2019Parth DMPas encore d'évaluation

- Gensets For OG MIDocument29 pagesGensets For OG MIParth DMPas encore d'évaluation

- Energy Recovery Analyst Day (FINAL)Document81 pagesEnergy Recovery Analyst Day (FINAL)Parth DMPas encore d'évaluation

- Factsheet Circular Economy in ChinaDocument2 pagesFactsheet Circular Economy in ChinaParth DMPas encore d'évaluation

- Amc Floc C PDSDocument1 pageAmc Floc C PDSParth DMPas encore d'évaluation

- Working Ourselves Out of A JobDocument2 pagesWorking Ourselves Out of A JobParth DMPas encore d'évaluation

- MYAS Industrial Investors Guide 2011Document62 pagesMYAS Industrial Investors Guide 2011Luca CampanaPas encore d'évaluation

- Ethylene ProcessDocument8 pagesEthylene Processkapil1979Pas encore d'évaluation

- MR SmukherjeeDocument36 pagesMR SmukherjeeParth DMPas encore d'évaluation

- Opinion Roll ResultsDocument1 pageOpinion Roll ResultsParth DMPas encore d'évaluation

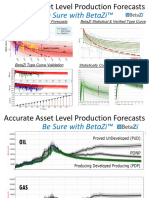

- BetaZi Focus On Reserves and Asset Level Production V2Document51 pagesBetaZi Focus On Reserves and Asset Level Production V2Parth DMPas encore d'évaluation

- Retail SalesDocument2 pagesRetail SalesParth DMPas encore d'évaluation

- The Golden LadyDocument1 pageThe Golden LadyParth DMPas encore d'évaluation

- ReaderDocument102 pagesReaderParth DMPas encore d'évaluation

- ReleasenotesDocument4 pagesReleasenotesSalvador LimachiPas encore d'évaluation

- Dynamics GuideDocument488 pagesDynamics GuideParth DMPas encore d'évaluation

- Readme HysysDocument1 pageReadme HysysParth DMPas encore d'évaluation

- HYSYS Documentation Suite for Process, Plant, HYCON & PIPESYSDocument1 pageHYSYS Documentation Suite for Process, Plant, HYCON & PIPESYSParth DMPas encore d'évaluation

- Search HysysDocument71 pagesSearch HysysParth DMPas encore d'évaluation

- Hysys Plant DocumentationDocument1 pageHysys Plant DocumentationParth DMPas encore d'évaluation

- 09 Population Growth in YeastDocument2 pages09 Population Growth in YeastParth DMPas encore d'évaluation

- WebtocDocument20 pagesWebtocusaid saifullahPas encore d'évaluation

- Gas Injection in ReservoirDocument10 pagesGas Injection in Reservoirsuhrab samiPas encore d'évaluation

- Unconventional Hydrocarbon Resources: - Geological StatisticsDocument26 pagesUnconventional Hydrocarbon Resources: - Geological Statisticsdorian.axel.ptPas encore d'évaluation

- Spe 211396 MsDocument17 pagesSpe 211396 MsAlfonso RamosPas encore d'évaluation

- Exploration PDFDocument19 pagesExploration PDFMarilyn Garzón AguirrePas encore d'évaluation

- Reservoir Simulation StudyDocument143 pagesReservoir Simulation StudyKunal Khandelwal0% (1)

- Drilling Fluid Selection for Shale GasDocument56 pagesDrilling Fluid Selection for Shale GasAhmer AkhlaquePas encore d'évaluation

- Non-Conventional Oil Resources. Crude Oil, Tar Sands, Tight Oil, Shale OilDocument6 pagesNon-Conventional Oil Resources. Crude Oil, Tar Sands, Tight Oil, Shale OilMukhtarov PgPas encore d'évaluation

- PETRONAS Floating LNG1 (PFLNG SATU) Activity Outlook 2018-2020Document35 pagesPETRONAS Floating LNG1 (PFLNG SATU) Activity Outlook 2018-2020ssgkooiPas encore d'évaluation

- Spe 191575 PaDocument14 pagesSpe 191575 PaNavneet SinghPas encore d'évaluation

- Final Year Project:: Engr. Hasan JehanzaibDocument56 pagesFinal Year Project:: Engr. Hasan JehanzaibMuhammad AbdullahPas encore d'évaluation

- Gas Engineering: Rabia Sabir Lecture #1Document36 pagesGas Engineering: Rabia Sabir Lecture #1Rabia SabirPas encore d'évaluation

- Syllabus RESGEO202 Spr2019 PDFDocument3 pagesSyllabus RESGEO202 Spr2019 PDFMohsin KhanPas encore d'évaluation

- An Overview of Unconventional Oil and Natural Gas: Resources and Federal ActionsDocument30 pagesAn Overview of Unconventional Oil and Natural Gas: Resources and Federal Actionskevin900Pas encore d'évaluation

- WEM Shale BrochureDocument2 pagesWEM Shale BrochureRuben PerazaPas encore d'évaluation

- ReservoirDocument26 pagesReservoirMohammad MakeyPas encore d'évaluation

- Fracturing Fluid Additive Risk AssessmentDocument4 pagesFracturing Fluid Additive Risk AssessmentMiguelPas encore d'évaluation

- Oil Shale PDFDocument59 pagesOil Shale PDFPondok Huda100% (3)

- Tight Gas ReservoirsDocument62 pagesTight Gas Reservoirshector vansPas encore d'évaluation

- Out 3Document24 pagesOut 3aminbm.pt24Pas encore d'évaluation

- Advanced Oil and Gas Exploration and RecoveryDocument11 pagesAdvanced Oil and Gas Exploration and RecoveryCARLOS LOPEZPas encore d'évaluation

- Encana - Lara Conrad PresentationDocument47 pagesEncana - Lara Conrad PresentationСергей СтояновPas encore d'évaluation

- KrisEnergy LTD - Appendices A To CDocument70 pagesKrisEnergy LTD - Appendices A To CInvest StockPas encore d'évaluation

- Oil and Gas Refining FocusDocument92 pagesOil and Gas Refining Focushasan.cepuPas encore d'évaluation

- Reservoir Geomechanics Syllabus 2020Document3 pagesReservoir Geomechanics Syllabus 2020mycurrentjobPas encore d'évaluation

- Crude Oil Properties-Handling Fire SafetyDocument96 pagesCrude Oil Properties-Handling Fire SafetyMichael J. BanePas encore d'évaluation

- Shale Oil Impacts on RefiningDocument24 pagesShale Oil Impacts on RefiningAnonymous NmOXutCKPas encore d'évaluation

- CMGWebinar Unconventional Reservoir Modelling 18feb15Document49 pagesCMGWebinar Unconventional Reservoir Modelling 18feb15mvinassa4828100% (2)