Vous aimerez peut-être aussi

- The Secrets To Successful Strategy ExecutionDocument10 pagesThe Secrets To Successful Strategy Executionits4krishna3776Pas encore d'évaluation

- Problems On Income StatementDocument2 pagesProblems On Income Statementits4krishna3776Pas encore d'évaluation

- Nepal Taxation Guide 2018 - 20180801041445 - 20181126030832Document25 pagesNepal Taxation Guide 2018 - 20180801041445 - 20181126030832its4krishna3776Pas encore d'évaluation

- Financial Statement Analysis: by Ghanendrafago Mba, M PhilDocument19 pagesFinancial Statement Analysis: by Ghanendrafago Mba, M Philits4krishna3776Pas encore d'évaluation

- Scanning Labour Act - 1992Document10 pagesScanning Labour Act - 1992its4krishna3776Pas encore d'évaluation

- Best Value For Money SlidesDocument9 pagesBest Value For Money Slidesits4krishna3776Pas encore d'évaluation

- Lecture 4 General Conditions of ContractIVDocument31 pagesLecture 4 General Conditions of ContractIVits4krishna3776Pas encore d'évaluation

- Corporate Finance Corporate Finance: The Balance The Balance - Sheet Model of The Sheet Model of The Firm FirmDocument5 pagesCorporate Finance Corporate Finance: The Balance The Balance - Sheet Model of The Sheet Model of The Firm Firmits4krishna3776Pas encore d'évaluation

- Environment Protection ActDocument7 pagesEnvironment Protection Actits4krishna3776Pas encore d'évaluation

- Construction: Industry AdvisorDocument8 pagesConstruction: Industry Advisorits4krishna3776Pas encore d'évaluation

- Wcms 117982 PDFDocument26 pagesWcms 117982 PDFits4krishna3776Pas encore d'évaluation

- 10th Annual ReportDocument28 pages10th Annual Reportits4krishna3776Pas encore d'évaluation

- Case 5 DiscussionDocument7 pagesCase 5 Discussionits4krishna3776Pas encore d'évaluation

- Variable and Absorption Income StatementDocument29 pagesVariable and Absorption Income Statementits4krishna3776Pas encore d'évaluation

- Cost Volume Profit AnalysisDocument19 pagesCost Volume Profit Analysisits4krishna3776Pas encore d'évaluation

- Section V: Financial Ratio AnalysisDocument12 pagesSection V: Financial Ratio Analysisits4krishna3776Pas encore d'évaluation

- REDCap - Guide To REDCap Exported FilesDocument14 pagesREDCap - Guide To REDCap Exported Filesits4krishna3776Pas encore d'évaluation

- Sample Detailed EvaluationDocument5 pagesSample Detailed Evaluationits4krishna3776Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Invoice HP CoverDocument1 pageInvoice HP CoverSurbhi JainPas encore d'évaluation

- TAXATIONDocument3 pagesTAXATIONcherry blossomPas encore d'évaluation

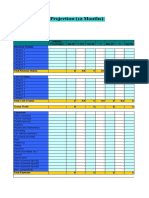

- Profit Loss 12 MonthDocument6 pagesProfit Loss 12 MonthMstefPas encore d'évaluation

- PremiumPaidStatement 2022-2023 AADocument1 pagePremiumPaidStatement 2022-2023 AAwk16111996Pas encore d'évaluation

- International Tax Notes (Part II) For May & Nov 23Document95 pagesInternational Tax Notes (Part II) For May & Nov 23Tushar MalhotraPas encore d'évaluation

- Tax.108 Allowed Deductions From Gross IncomeDocument10 pagesTax.108 Allowed Deductions From Gross IncomeLeshaira Jimeno100% (1)

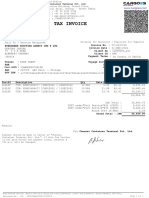

- Invoice CT-2237192Document2 pagesInvoice CT-2237192ABALUPas encore d'évaluation

- Chapter 3 SlidesDocument27 pagesChapter 3 SlidesEmily AirhartPas encore d'évaluation

- Ad Valorem TaxDocument4 pagesAd Valorem TaxManoj KPas encore d'évaluation

- Solved On January 1 of The Current Year Scott Borrows 80 000Document1 pageSolved On January 1 of The Current Year Scott Borrows 80 000Anbu jaromiaPas encore d'évaluation

- Your Wednesday Evening Trip With Uber: Thanks For Choosing Uber, Deepak June 14, 2017 - UberxDocument3 pagesYour Wednesday Evening Trip With Uber: Thanks For Choosing Uber, Deepak June 14, 2017 - UberxdeePas encore d'évaluation

- Beer, Bourbon, & BBQDocument3 pagesBeer, Bourbon, & BBQSunlight FoundationPas encore d'évaluation

- BibliographyDocument11 pagesBibliographypaulPas encore d'évaluation

- Article 265 of Constitution of IndiaDocument10 pagesArticle 265 of Constitution of IndiaAshutosh Singh ParmarPas encore d'évaluation

- Hwhwwjwjwjwjwjwiwiwiwkke Cpa Review School of The Philippines Manila Corporations Dela Cruz / de Vera / Lopez / LlamadoDocument9 pagesHwhwwjwjwjwjwjwiwiwiwkke Cpa Review School of The Philippines Manila Corporations Dela Cruz / de Vera / Lopez / LlamadoSophia PerezPas encore d'évaluation

- Veerabadreshwara Medicals BillsDocument1 pageVeerabadreshwara Medicals BillsPavan KPas encore d'évaluation

- Receipt Voucher: Xiaomi Technology India Private LimitedDocument1 pageReceipt Voucher: Xiaomi Technology India Private LimitedRubhan kumarPas encore d'évaluation

- Kitui County Annual Development Plan 2016 - 2017Document119 pagesKitui County Annual Development Plan 2016 - 2017Oloo Yussuf Ochieng'Pas encore d'évaluation

- 2307 NEW PLDTDocument2 pages2307 NEW PLDTdayneblazePas encore d'évaluation

- Chapter 1 Introduction To GSTDocument5 pagesChapter 1 Introduction To GSTabhay javiyaPas encore d'évaluation

- Income Taxation Reviewer Banggawan 2019 PDFDocument10 pagesIncome Taxation Reviewer Banggawan 2019 PDFKryzzel Anne Jon100% (1)

- Franking Account WorkpaperDocument6 pagesFranking Account WorkpaperCarol YaoPas encore d'évaluation

- Systra Philippines vs. Cir G.R. No. 176290 September 21, 2007Document2 pagesSystra Philippines vs. Cir G.R. No. 176290 September 21, 2007Armstrong BosantogPas encore d'évaluation

- Dividends and The Dividend ExemptionDocument1 pageDividends and The Dividend ExemptionSunny KirpalaniPas encore d'évaluation

- 2019 TaxReturn PDFDocument23 pages2019 TaxReturn PDFalhajikura2252Pas encore d'évaluation

- AFF's Memorandum On Finance (Supplementary) Bill 2023Document7 pagesAFF's Memorandum On Finance (Supplementary) Bill 2023Ahmad SubhaniPas encore d'évaluation

- Payslip For The Month of March 2015 Earnings DeductionsDocument1 pagePayslip For The Month of March 2015 Earnings Deductionsmadhusudhan N RPas encore d'évaluation

- Form 1 - Illustration Income Tax: For Individuals Earning Purely Compensation Income Accomplish BIR Form No. - 1700Document3 pagesForm 1 - Illustration Income Tax: For Individuals Earning Purely Compensation Income Accomplish BIR Form No. - 1700Rea Rose TampusPas encore d'évaluation

- Principles of Taxation Law Part 7Document104 pagesPrinciples of Taxation Law Part 7Han Ny PhamPas encore d'évaluation

- Clubbing of IncomeDocument3 pagesClubbing of IncomeVachanamrutha R.VPas encore d'évaluation