Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Palanca v. City of Manila and TrinidadDocument2 pagesPalanca v. City of Manila and TrinidadJanine Ismael100% (1)

- 25 Site Clearance PlanDocument12 pages25 Site Clearance PlanmabrarahmedPas encore d'évaluation

- Gamboa vs. Teves, 652 SCRA 690, G.R. No. 176579 June 28, 2011Document32 pagesGamboa vs. Teves, 652 SCRA 690, G.R. No. 176579 June 28, 2011Daysel FatePas encore d'évaluation

- @ Neg .Syo: An Trabahst KonsyumerDocument11 pages@ Neg .Syo: An Trabahst KonsyumermarcmiPas encore d'évaluation

- FILAMER CHRISTIAN UNIVERSITY SENIOR HIGH SCHOOL ABM WORK IMMERSIONDocument2 pagesFILAMER CHRISTIAN UNIVERSITY SENIOR HIGH SCHOOL ABM WORK IMMERSIONyouismyfavcolour80% (5)

- Maranan vs. Perez, 20 SCRA 412, No. L-22272 June 26, 1967Document3 pagesMaranan vs. Perez, 20 SCRA 412, No. L-22272 June 26, 1967Daysel FatePas encore d'évaluation

- Saudi Arabia Airlines and Brenda Betia vs. ResebencioDocument2 pagesSaudi Arabia Airlines and Brenda Betia vs. ResebencioMarc Lester Hernandez-Sta Ana100% (1)

- Mock Exam Nov 302015Document37 pagesMock Exam Nov 302015Law_Portal100% (2)

- CIVIL SERVICE COMMISSION V. SALAS – REYESDocument2 pagesCIVIL SERVICE COMMISSION V. SALAS – REYESRuby Reyes100% (3)

- Assoc. of Medical Clinics For Overseas Workers V GCC Approved Medical CenterDocument2 pagesAssoc. of Medical Clinics For Overseas Workers V GCC Approved Medical CenterDany100% (1)

- Bsen25817 PDFDocument18 pagesBsen25817 PDFdzat_sudrazat0% (1)

- Deed of AssignmentDocument2 pagesDeed of AssignmentRizalFaiz50% (2)

- 2016 - Hernandez vs. Crossworld Marine Services, Inc., 808 SCRA 575, G.R. No. 209098 November 14, 2016 - Quit ClaimsDocument11 pages2016 - Hernandez vs. Crossworld Marine Services, Inc., 808 SCRA 575, G.R. No. 209098 November 14, 2016 - Quit ClaimsDaysel FatePas encore d'évaluation

- 2014 - Balasbas vs. Monayao, 716 SCRA 190, G.R. No. 190524 February 17, 2014 - Administrative Law - Public OfficersDocument7 pages2014 - Balasbas vs. Monayao, 716 SCRA 190, G.R. No. 190524 February 17, 2014 - Administrative Law - Public OfficersDaysel FatePas encore d'évaluation

- 2016 - Hernandez vs. Crossworld Marine Services, Inc., 808 SCRA 575, G.R. No. 209098 November 14, 2016 - Quit ClaimsDocument11 pages2016 - Hernandez vs. Crossworld Marine Services, Inc., 808 SCRA 575, G.R. No. 209098 November 14, 2016 - Quit ClaimsDaysel FatePas encore d'évaluation

- 2014 - Afulugencia vs. Metropolitan Bank & Trust Co., 715 SCRA 399, G.R. No. 185145 February 5, 2014 - Remedial Law - CourtsDocument7 pages2014 - Afulugencia vs. Metropolitan Bank & Trust Co., 715 SCRA 399, G.R. No. 185145 February 5, 2014 - Remedial Law - CourtsDaysel FatePas encore d'évaluation

- Affidavit of Registration of BirthDocument1 pageAffidavit of Registration of BirthDaysel FatePas encore d'évaluation

- Vda. De. Aviles vs. Court of Appeals, 264 SCRA 473, G.R. No. 95748 November 21, 1996Document5 pagesVda. De. Aviles vs. Court of Appeals, 264 SCRA 473, G.R. No. 95748 November 21, 1996Daysel FatePas encore d'évaluation

- Dio vs. Japor, 463 SCRA 170, G.R. No. 154129 July 8, 2005Document4 pagesDio vs. Japor, 463 SCRA 170, G.R. No. 154129 July 8, 2005Daysel FatePas encore d'évaluation

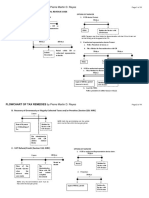

- Flowchart of Tax Remedies 2017 Update PRDocument11 pagesFlowchart of Tax Remedies 2017 Update PRMarjorie Kate CresciniPas encore d'évaluation

- Francisco vs. Intermediate Appellate Court, 177 SCRA 527, G.R. No. 63996 September 15, 1989Document8 pagesFrancisco vs. Intermediate Appellate Court, 177 SCRA 527, G.R. No. 63996 September 15, 1989Daysel FatePas encore d'évaluation

- RR No. 9Document9 pagesRR No. 9John Paul de leonPas encore d'évaluation

- Floro vs. Llenado, 244 SCRA 713, G.R. No. 75723 June 2, 1995Document10 pagesFloro vs. Llenado, 244 SCRA 713, G.R. No. 75723 June 2, 1995Daysel FatePas encore d'évaluation

- Habana vs. Robles, 310 SCRA 511, July 19, 1999Document9 pagesHabana vs. Robles, 310 SCRA 511, July 19, 1999Daysel FatePas encore d'évaluation

- Francisco vs. Intermediate Appellate Court, 177 SCRA 527, G.R. No. 63996 September 15, 1989 PDFDocument6 pagesFrancisco vs. Intermediate Appellate Court, 177 SCRA 527, G.R. No. 63996 September 15, 1989 PDFDaysel FatePas encore d'évaluation

- Wegel Vs Senpium DyDocument2 pagesWegel Vs Senpium DyBelteshazzarL.CabacangPas encore d'évaluation

- Raymundo V PenasDocument4 pagesRaymundo V PenasDaysel FatePas encore d'évaluation

- Civ CaseDocument10 pagesCiv CaseDaysel FatePas encore d'évaluation

- Villanueva V People of The PhilippinesDocument5 pagesVillanueva V People of The PhilippinesDaysel FatePas encore d'évaluation

- Francisco vs. Intermediate Appellate Court, 177 SCRA 527, G.R. No. 63996 September 15, 1989 PDFDocument6 pagesFrancisco vs. Intermediate Appellate Court, 177 SCRA 527, G.R. No. 63996 September 15, 1989 PDFDaysel FatePas encore d'évaluation

- Tuazon vs. Del Rosario-Suarez, 637 SCRA 728, G.R. No. 168325 December 13, 2010Document7 pagesTuazon vs. Del Rosario-Suarez, 637 SCRA 728, G.R. No. 168325 December 13, 2010Daysel FatePas encore d'évaluation

- Camporedondo Vs AznarDocument9 pagesCamporedondo Vs AznarDaysel FatePas encore d'évaluation

- Uy V CaDocument6 pagesUy V CaRose AnnPas encore d'évaluation

- Similarities in Dating ShowsDocument9 pagesSimilarities in Dating ShowsDaysel FatePas encore d'évaluation

- Office of The President V Cataquiz PDFDocument11 pagesOffice of The President V Cataquiz PDFDaysel FatePas encore d'évaluation

- Mendiola V People and SandigangbayanDocument10 pagesMendiola V People and SandigangbayanDaysel FatePas encore d'évaluation

- Tuazon vs. Del Rosario-Suarez, 637 SCRA 728, G.R. No. 168325 December 13, 2010Document7 pagesTuazon vs. Del Rosario-Suarez, 637 SCRA 728, G.R. No. 168325 December 13, 2010Daysel FatePas encore d'évaluation

- PNB Interest Rate Hikes Violated LawsDocument5 pagesPNB Interest Rate Hikes Violated LawsDaysel FatePas encore d'évaluation

- Office of The President V Cataquiz PDFDocument11 pagesOffice of The President V Cataquiz PDFDaysel FatePas encore d'évaluation

- Estrada Vs Sandigangbayan G.R. No. 148965. February 26, 2002Document15 pagesEstrada Vs Sandigangbayan G.R. No. 148965. February 26, 2002Daysel FatePas encore d'évaluation

- RA 7903 - Zamboanga City Special Economic Zone Act of 1995Document5 pagesRA 7903 - Zamboanga City Special Economic Zone Act of 1995Kristel YeenPas encore d'évaluation

- Interpretation of construction contracts based on commercial common senseDocument3 pagesInterpretation of construction contracts based on commercial common senseRanjith EkanayakePas encore d'évaluation

- Receipt of Letter of Award From MORTH (Company Update)Document2 pagesReceipt of Letter of Award From MORTH (Company Update)Shyam SunderPas encore d'évaluation

- EY-Point-of-view-auditor-reporting-February-2014 Ernst and Young PDFDocument5 pagesEY-Point-of-view-auditor-reporting-February-2014 Ernst and Young PDFMai RosaupanPas encore d'évaluation

- Faqs - MSC Finance (Jbims)Document42 pagesFaqs - MSC Finance (Jbims)Bhaskar MohanPas encore d'évaluation

- Agreement For Ip Packet Exchange (Ipx) Services 17 December 2014Document66 pagesAgreement For Ip Packet Exchange (Ipx) Services 17 December 2014temporal11Pas encore d'évaluation

- How To Register A Sole Proprietorship in The PhilippinesDocument5 pagesHow To Register A Sole Proprietorship in The PhilippinesAna Marie ValenzuelaPas encore d'évaluation

- Unit 2 3 - Lesson 8 - Calculating Market EquilibriumDocument7 pagesUnit 2 3 - Lesson 8 - Calculating Market Equilibriumapi-260512563Pas encore d'évaluation

- Professionalism and Ethics - A Quantity Surveying PerspectiveDocument10 pagesProfessionalism and Ethics - A Quantity Surveying PerspectiveKarutama SelarasPas encore d'évaluation

- Suitability and Declarations FormDocument5 pagesSuitability and Declarations FormMansoor MalikPas encore d'évaluation

- Chapter 2 - Approaches To Corporate GovernanceDocument8 pagesChapter 2 - Approaches To Corporate Governancemarygrace sadiaPas encore d'évaluation

- Tehnologii de PrelucrareDocument1 pageTehnologii de PrelucraretonyPas encore d'évaluation

- The Decline in Access To Correspondent Banking Services in Emerging Markets: Trends, Impacts, and SolutionsDocument56 pagesThe Decline in Access To Correspondent Banking Services in Emerging Markets: Trends, Impacts, and SolutionsforcetenPas encore d'évaluation

- QAA ManualDocument12 pagesQAA ManualSasi KumarPas encore d'évaluation

- .Document5 pages.Ana PopPas encore d'évaluation

- NQa Legal Research Updates on COVID-19Document15 pagesNQa Legal Research Updates on COVID-19Nea QuiachonPas encore d'évaluation

- Central Marks Department Issues Testing Scheme for Rubber Hawai ChappalsDocument7 pagesCentral Marks Department Issues Testing Scheme for Rubber Hawai ChappalsKalees KaleesPas encore d'évaluation

- MDI Product Catalog USDocument36 pagesMDI Product Catalog USKarim MohamedPas encore d'évaluation

- Basic Tax Principles ExplainedDocument46 pagesBasic Tax Principles Explained在于在Pas encore d'évaluation