Vous aimerez peut-être aussi

- Reviewer Finals Tax 301Document4 pagesReviewer Finals Tax 301Jana RamosPas encore d'évaluation

- Assignment 1 Taxes On IndividualsDocument7 pagesAssignment 1 Taxes On IndividualsMarynissa CatibogPas encore d'évaluation

- Acctg110 FinalsDocument21 pagesAcctg110 FinalsRoman Dominic LlanoPas encore d'évaluation

- Capital Budgeting Sample ProblemsDocument10 pagesCapital Budgeting Sample ProblemsMark Gelo WinchesterPas encore d'évaluation

- Cash Flow Statement StudentDocument60 pagesCash Flow Statement StudentJanine MosatallaPas encore d'évaluation

- Retained Earnings and Cost of Debentures: Presented by P. Madhuri Prinkle Jain Shersti JainDocument37 pagesRetained Earnings and Cost of Debentures: Presented by P. Madhuri Prinkle Jain Shersti JainPrinkle JainPas encore d'évaluation

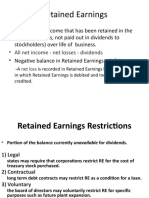

- Retained EarningsDocument30 pagesRetained EarningsPooja SreePas encore d'évaluation

- Corporate Income TaxDocument8 pagesCorporate Income TaxClaire BarbaPas encore d'évaluation

- Taxation 1-5Document6 pagesTaxation 1-5dimpy dPas encore d'évaluation

- Lab Chapter 17Document5 pagesLab Chapter 17Tran Kim Tram PhanPas encore d'évaluation

- Income Tax TableDocument6 pagesIncome Tax TableMarian's PrelovePas encore d'évaluation

- Taxation Situational ProblemsDocument32 pagesTaxation Situational ProblemsMilo MilkPas encore d'évaluation

- Case Study Accounting Oart2Document5 pagesCase Study Accounting Oart2Vero MinaPas encore d'évaluation

- SW05Document7 pagesSW05Nadi HoodPas encore d'évaluation

- Cash Flow Statement (Direct Method)Document3 pagesCash Flow Statement (Direct Method)Margarette RobiegoPas encore d'évaluation

- Chapter 5 - Statement of Comprehensive Income: Problem 5-1 (AICPA Adapted)Document20 pagesChapter 5 - Statement of Comprehensive Income: Problem 5-1 (AICPA Adapted)Asi Cas Jav100% (2)

- Accounting 2Document18 pagesAccounting 2cherryannPas encore d'évaluation

- Cash Flow Statement-ShortDocument27 pagesCash Flow Statement-ShortLaurene Delos ReyesPas encore d'évaluation

- Financial Statement Analysis Midterm Assignment AssignmentDocument5 pagesFinancial Statement Analysis Midterm Assignment AssignmentHaidar NuraPas encore d'évaluation

- UntitledDocument13 pagesUntitledAnne GuamosPas encore d'évaluation

- Homework N3Document24 pagesHomework N3Maiko KopadzePas encore d'évaluation

- Q1 Week5 Illustrative ProblemDocument3 pagesQ1 Week5 Illustrative ProblemIt’s yanaPas encore d'évaluation

- BTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsDocument21 pagesBTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsgatotkaPas encore d'évaluation

- Update: Intermediate Accounting 15EDocument10 pagesUpdate: Intermediate Accounting 15ENarissa Mae QuijanoPas encore d'évaluation

- Question No 1: A-Gross PayDocument6 pagesQuestion No 1: A-Gross PayArmaghan Ali MalikPas encore d'évaluation

- Analysis of Project Cash FlowsDocument16 pagesAnalysis of Project Cash FlowsTanmaye KapurPas encore d'évaluation

- CHAPTER 4 Consolidation Subse To Date of Acquisitio 2023Document12 pagesCHAPTER 4 Consolidation Subse To Date of Acquisitio 2023firaolmosisabonkePas encore d'évaluation

- Quiz Chapter 2 Statement of Comprehensive IncomeDocument13 pagesQuiz Chapter 2 Statement of Comprehensive Incomefinn mertensPas encore d'évaluation

- Acctg1205 - Chapter 8Document48 pagesAcctg1205 - Chapter 8Elj Grace BaronPas encore d'évaluation

- Optional Standard Deductions ExampleDocument7 pagesOptional Standard Deductions ExampleSandia EspejoPas encore d'évaluation

- Accounting Exercises On Cash FlowsDocument2 pagesAccounting Exercises On Cash FlowsMicaella GoPas encore d'évaluation

- Quiz 2.1 - Individual Taxpayers and Quiz 3.1 - INCOME TAX ON CORPORATIONSDocument5 pagesQuiz 2.1 - Individual Taxpayers and Quiz 3.1 - INCOME TAX ON CORPORATIONSHunternotPas encore d'évaluation

- Akm 3Document5 pagesAkm 3naylaphuiamazonaPas encore d'évaluation

- Straight Problems Income Tax Bsa2Document2 pagesStraight Problems Income Tax Bsa2dimpy dPas encore d'évaluation

- Individuals Assign3Document7 pagesIndividuals Assign3jdPas encore d'évaluation

- Assignment N3Document12 pagesAssignment N3Maiko KopadzePas encore d'évaluation

- Chapter 04-Syndicate 1Document5 pagesChapter 04-Syndicate 1Ahike HukatenPas encore d'évaluation

- Chapter 5Document15 pagesChapter 5Coursehero PremiumPas encore d'évaluation

- CZ21A MODEL Answer KeyDocument7 pagesCZ21A MODEL Answer KeymadhuPas encore d'évaluation

- Case Study - New Product LineDocument16 pagesCase Study - New Product LineJemarse GumpalPas encore d'évaluation

- QUIZ - CHAPTER 2 - Printing STATEMENT OF COMPREHENSIVE INCOMEDocument6 pagesQUIZ - CHAPTER 2 - Printing STATEMENT OF COMPREHENSIVE INCOMEAllen Kate Malazarte0% (1)

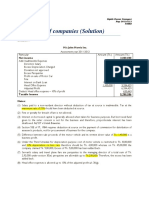

- Assessment of Companies (Solution) : Solution 1 M/s John Morris IncDocument8 pagesAssessment of Companies (Solution) : Solution 1 M/s John Morris IncIQBALPas encore d'évaluation

- Chapter 2 - Statement of Cash FlowsDocument23 pagesChapter 2 - Statement of Cash FlowsCholophrex SamilinPas encore d'évaluation

- Appendix Projected Profit & LossDocument3 pagesAppendix Projected Profit & LossDwirainita RamadhaniaPas encore d'évaluation

- Jawaban Quiz 2Document2 pagesJawaban Quiz 2Muhammad IrvanPas encore d'évaluation

- 8.6 Assignment - Regular Income Tax On CorporationsDocument3 pages8.6 Assignment - Regular Income Tax On CorporationsRoselyn LumbaoPas encore d'évaluation

- Taxable Income and Income Tax - Foreign Tax Credit - AdministrDocument52 pagesTaxable Income and Income Tax - Foreign Tax Credit - AdministrCharlotte MalgapoPas encore d'évaluation

- Cases Chapter 4 - Syndicate 8Document4 pagesCases Chapter 4 - Syndicate 8Ahike HukatenPas encore d'évaluation

- Ho2 SciDocument2 pagesHo2 SciAbdullah JulkanainPas encore d'évaluation

- Pr. 4-146-Income StatementDocument13 pagesPr. 4-146-Income StatementElene SamnidzePas encore d'évaluation

- Compre H in SiveDocument4 pagesCompre H in SiveTilahun GirmaPas encore d'évaluation

- Income Taxation - Regular Income Tax 2Document5 pagesIncome Taxation - Regular Income Tax 2Drew BanlutaPas encore d'évaluation

- AA367Document11 pagesAA367Meena DasPas encore d'évaluation

- Multi-Step GAAP Income StatementDocument3 pagesMulti-Step GAAP Income Statementmohammedbudul18Pas encore d'évaluation

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineD'EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LinePas encore d'évaluation

- The Valuation of Digital Intangibles: Technology, Marketing and InternetD'EverandThe Valuation of Digital Intangibles: Technology, Marketing and InternetPas encore d'évaluation

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryD'EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryPas encore d'évaluation

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineD'EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LinePas encore d'évaluation

- UG BComDocument43 pagesUG BComydhhPas encore d'évaluation

- CIR v. Toshiba Information Equipment (Phils.) IncDocument2 pagesCIR v. Toshiba Information Equipment (Phils.) IncEJ PajaroPas encore d'évaluation

- Itr 2018-19 PDFDocument1 pageItr 2018-19 PDFMalik MuzafferPas encore d'évaluation

- Chapter 10 and 11Document2 pagesChapter 10 and 11johnpenielmontalesPas encore d'évaluation

- Income Taxation 01 Chapter 1 Summary - CompressDocument7 pagesIncome Taxation 01 Chapter 1 Summary - CompressALTHEA REN'EE LIMPAOPas encore d'évaluation

- Howe Engineering Projects India PVT LTD: Earnings Amount Deductions Amount Perks/Other income/Exempton/RebatesDocument1 pageHowe Engineering Projects India PVT LTD: Earnings Amount Deductions Amount Perks/Other income/Exempton/RebatesSumantrra ChattopadhyayPas encore d'évaluation

- 2009 Form 6744Document192 pages2009 Form 6744Vita Volunteers WebmasterPas encore d'évaluation

- BT and FBT Full Specimen Exam Answers Correct Answer MarksDocument4 pagesBT and FBT Full Specimen Exam Answers Correct Answer MarksSothida SaromPas encore d'évaluation

- Inter Ca Syllabus 1Document5 pagesInter Ca Syllabus 1SamirPas encore d'évaluation

- 5310 16909 1 PBDocument13 pages5310 16909 1 PBgunaPas encore d'évaluation

- Sample PANDocument5 pagesSample PANArmie Lyn Simeon100% (1)

- Module 3 - Sources of IncomeDocument3 pagesModule 3 - Sources of IncomeMaryrose SumulongPas encore d'évaluation

- Composition Scheme Under GST ExplainedDocument3 pagesComposition Scheme Under GST ExplainedrgurvareddyPas encore d'évaluation

- Module 06 Capital Gains Taxation 2 2Document17 pagesModule 06 Capital Gains Taxation 2 2Joshua BazarPas encore d'évaluation

- Ramchandra Shahaji ChavanDocument1 pageRamchandra Shahaji ChavanPrashant PatilPas encore d'évaluation

- Chapter 23 IAS 12 Income TaxesDocument26 pagesChapter 23 IAS 12 Income TaxesKelvin Chu JY100% (1)

- Income Taxation 2015 Edition Solman PDFDocument53 pagesIncome Taxation 2015 Edition Solman PDFPrincess AlqueroPas encore d'évaluation

- Income and Business TaxationDocument24 pagesIncome and Business TaxationFerdinand Carlos B. DadoPas encore d'évaluation

- Analisis Pemotongan, Penyetoran Dan Pelaporan PPH Pasal 21 Bagi Pegawai Pada Pt. PkssDocument10 pagesAnalisis Pemotongan, Penyetoran Dan Pelaporan PPH Pasal 21 Bagi Pegawai Pada Pt. PkssMuhammad AfdholPas encore d'évaluation

- Certain Government Payments: Copy B For RecipientDocument2 pagesCertain Government Payments: Copy B For RecipientDylan Bizier-Conley100% (1)

- QuotationDocument1 pageQuotationsyed nizamuddenPas encore d'évaluation

- Aparna DecDocument1 pageAparna Decpraveen kumarPas encore d'évaluation

- GSTReturn Oct 2021Document1 pageGSTReturn Oct 2021Muhammad Ali Abdul RazzaquePas encore d'évaluation

- Vergara, Gian Bianca F. BSAT-4A Recitation: Compensation IncomeDocument3 pagesVergara, Gian Bianca F. BSAT-4A Recitation: Compensation Incomelena cpa100% (2)

- Sravani Medical Syndicate-Tenali (12x6) GST PDFDocument1 pageSravani Medical Syndicate-Tenali (12x6) GST PDFmytreyiPas encore d'évaluation

- KANJAKDocument1 pageKANJAKgajari gulPas encore d'évaluation

- RMC No. 69-2023 v2Document1 pageRMC No. 69-2023 v2Jomar CorunoPas encore d'évaluation

- Starter Checklist: Instructions For EmployersDocument2 pagesStarter Checklist: Instructions For EmployersTareqPas encore d'évaluation

- Taxes in Canada-Final 2010-4-07 Recovered)Document112 pagesTaxes in Canada-Final 2010-4-07 Recovered)DayarayanCanadaPas encore d'évaluation

- Taxation Ch3Document27 pagesTaxation Ch3sabit hussenPas encore d'évaluation