Vous aimerez peut-être aussi

- The Silenced Voices of The IncarceratedDocument19 pagesThe Silenced Voices of The IncarceratedHeidi McCafferty100% (1)

- The Business of Belonging: How to Make Community your Competitive AdvantageD'EverandThe Business of Belonging: How to Make Community your Competitive AdvantageÉvaluation : 4 sur 5 étoiles4/5 (1)

- Air Asia CompleteDocument18 pagesAir Asia CompleteAmy CharmainePas encore d'évaluation

- Uber MarketingDocument23 pagesUber MarketingKavya SathishPas encore d'évaluation

- Skills For Smart Industrial Specialization and Digital TransformationDocument342 pagesSkills For Smart Industrial Specialization and Digital TransformationAndrei ItemPas encore d'évaluation

- China-The Land That Failed To Fail PDFDocument81 pagesChina-The Land That Failed To Fail PDFeric_stPas encore d'évaluation

- Antiracist & Decolonized Teaching: A Call To ActionDocument28 pagesAntiracist & Decolonized Teaching: A Call To ActionAnamika Twyman-GhoshalPas encore d'évaluation

- Full ProgramDocument198 pagesFull Programceo_080% (1)

- 2018IPV1Document124 pages2018IPV1Arianna Rafaela LlumiquingaPas encore d'évaluation

- PRP Call For ApplicationsDocument4 pagesPRP Call For ApplicationsChari TawaPas encore d'évaluation

- Commentary On Protection of Privileged ESI.17TSCJ95Document112 pagesCommentary On Protection of Privileged ESI.17TSCJ95Charles XavierPas encore d'évaluation

- 2017 Application PDFDocument460 pages2017 Application PDFStephanie Robert MackPas encore d'évaluation

- Presentation Document: I. The North American Forum On Integration (NAFI)Document6 pagesPresentation Document: I. The North American Forum On Integration (NAFI)TheNafinaArchivePas encore d'évaluation

- Reclaiming Fair Use: How to Put Balance Back in Copyright, Second EditionD'EverandReclaiming Fair Use: How to Put Balance Back in Copyright, Second EditionPas encore d'évaluation

- The Intelligent Portfolio: Practical Wisdom on Personal Investing from Financial EnginesD'EverandThe Intelligent Portfolio: Practical Wisdom on Personal Investing from Financial EnginesPas encore d'évaluation

- Comey UNLV ContractDocument10 pagesComey UNLV ContractRiley SnyderPas encore d'évaluation

- Strategicplan2011 enDocument39 pagesStrategicplan2011 enherry.mdnPas encore d'évaluation

- Smith Rehaag&Farrow 2021 Access To Justice For Refugees ReportDocument44 pagesSmith Rehaag&Farrow 2021 Access To Justice For Refugees ReportHarroldPas encore d'évaluation

- A Business Plan: Cooperative Extension System National Center For DiversityDocument18 pagesA Business Plan: Cooperative Extension System National Center For DiversityWilliam MengPas encore d'évaluation

- June 2014Document80 pagesJune 2014ICCFA StaffPas encore d'évaluation

- Citizenship in a Connected Canada: A Research and Policy AgendaD'EverandCitizenship in a Connected Canada: A Research and Policy AgendaPas encore d'évaluation

- The Diaspora and Returnee Entrepreneurship Dynamics and Development in Post Conflict Economies Nick Williams Full ChapterDocument68 pagesThe Diaspora and Returnee Entrepreneurship Dynamics and Development in Post Conflict Economies Nick Williams Full Chapterclarence.dilworth587100% (3)

- Sharing: Pro Bono and Community ServiceDocument24 pagesSharing: Pro Bono and Community ServiceDwii RestyyPas encore d'évaluation

- Sloan - C International Conference On Online LearningDocument126 pagesSloan - C International Conference On Online LearningbygskyPas encore d'évaluation

- Alterman Loyalty Interior v8 WEB FULLDocument49 pagesAlterman Loyalty Interior v8 WEB FULLenlightening warriorPas encore d'évaluation

- Sponsorship LetterandrequestDocument3 pagesSponsorship Letterandrequestsharath haradyPas encore d'évaluation

- Summer/Fall 2020 Highlights and Community Update: New York Senator Rachel May 53rd State Senate DistrictDocument4 pagesSummer/Fall 2020 Highlights and Community Update: New York Senator Rachel May 53rd State Senate DistrictState Senator Rachel MayPas encore d'évaluation

- Donor Bill of Rights - Antioch UniversityDocument10 pagesDonor Bill of Rights - Antioch UniversityantiochpapersPas encore d'évaluation

- Brochure FINALDocument100 pagesBrochure FINALjhmason38Pas encore d'évaluation

- NBPLC 2012 Post-Conference Impact ReportDocument44 pagesNBPLC 2012 Post-Conference Impact ReportblackprelawPas encore d'évaluation

- Public Relations Simple SolutionsDocument17 pagesPublic Relations Simple SolutionswhitneyhollmanPas encore d'évaluation

- Law School Public LectureDocument2 pagesLaw School Public Lecturemark_loongPas encore d'évaluation

- Research Paper LiberiaDocument4 pagesResearch Paper Liberiacan8t8g5100% (1)

- In The Loop 6-13-12Document4 pagesIn The Loop 6-13-12Valerie F. LeonardPas encore d'évaluation

- This Is Our Canada: One Nation, Many FacesDocument50 pagesThis Is Our Canada: One Nation, Many FacesJohn Humphrey Centre for Peace and Human Rights100% (2)

- Environmentally Clean CommunitiesDocument5 pagesEnvironmentally Clean CommunitiesBrianPas encore d'évaluation

- Kircher Confidentiality BreachDocument2 pagesKircher Confidentiality BreachpegspiratePas encore d'évaluation

- Project News Bulletin: Draft Report Comment Period UnderwayDocument8 pagesProject News Bulletin: Draft Report Comment Period UnderwayYahdi AzzuhryPas encore d'évaluation

- Appealing To The Crowd The Ethical Political and Practical Dimensions of Donation Based Crowdfunding Jeremy Snyder Full ChapterDocument68 pagesAppealing To The Crowd The Ethical Political and Practical Dimensions of Donation Based Crowdfunding Jeremy Snyder Full Chaptertommy.villegas301100% (4)

- This Content Downloaded From 14.139.235.3 On Tue, 04 Jan 2022 11:42:34 UTCDocument7 pagesThis Content Downloaded From 14.139.235.3 On Tue, 04 Jan 2022 11:42:34 UTCRoddy89Pas encore d'évaluation

- A Comparison of International Housing Finance Systems: HearingDocument119 pagesA Comparison of International Housing Finance Systems: HearingScribd Government DocsPas encore d'évaluation

- Diversity InclusionDocument20 pagesDiversity InclusionMarco Ramirez100% (2)

- Document 5Document9 pagesDocument 5dekisolaPas encore d'évaluation

- ScivnsecondreportDocument10 pagesScivnsecondreportapi-241698816Pas encore d'évaluation

- American Philanthropic Foundations: Regional Difference and ChangeD'EverandAmerican Philanthropic Foundations: Regional Difference and ChangePas encore d'évaluation

- Yannaca Small, Catherine ArbitrationDocument790 pagesYannaca Small, Catherine ArbitrationAliaksandr SkalabanauPas encore d'évaluation

- Pro Bono Handbook - A Guide To Establishing A Pro Bono Program at Your Law Firm 3Document85 pagesPro Bono Handbook - A Guide To Establishing A Pro Bono Program at Your Law Firm 3Elba Gutiérrez CastilloPas encore d'évaluation

- Partners in BrotherhoodDocument4 pagesPartners in BrotherhoodDianne BishopPas encore d'évaluation

- October 2021 General Body AgendaDocument3 pagesOctober 2021 General Body AgendaLionel GreavesPas encore d'évaluation

- Islamophobiareport2009 2010Document68 pagesIslamophobiareport2009 2010Bosanski KongresPas encore d'évaluation

- Powering DiscoveryDocument176 pagesPowering DiscoveryThe Council of Canadian AcademiesPas encore d'évaluation

- Finance Monthly Report OctoberDocument2 pagesFinance Monthly Report OctoberaswsuvPas encore d'évaluation

- Bulletin Connecting: Elcome To The November Edition of The DSADocument7 pagesBulletin Connecting: Elcome To The November Edition of The DSAJake Dabang Dan-AzumiPas encore d'évaluation

- Young Inventors Association: Building A World Class ProgramDocument11 pagesYoung Inventors Association: Building A World Class ProgramaroyeahPas encore d'évaluation

- Thesis Symposium BelfastDocument8 pagesThesis Symposium Belfastjasmineculbrethwilmington100% (2)

- International Law - 100 Ways It Shapes Our Lives (ASIL Booklet)Document56 pagesInternational Law - 100 Ways It Shapes Our Lives (ASIL Booklet)Regina Ibragimova100% (1)

- Nov - Dec 2008 Trout Line Newsletter, Tualatin Valley Trout UnlimitedDocument8 pagesNov - Dec 2008 Trout Line Newsletter, Tualatin Valley Trout UnlimitedFriends of Tualatin Valley Trout UnlimitedPas encore d'évaluation

- Making The Law Work For EveryoneDocument108 pagesMaking The Law Work For Everyonekukuman1234Pas encore d'évaluation

- Hearing: Financial Services Issues: A Consumer'S PerspectiveDocument122 pagesHearing: Financial Services Issues: A Consumer'S PerspectiveScribd Government DocsPas encore d'évaluation

- 2017 ABA-SIL Miami Fall Meeting - ProgrammeDocument40 pages2017 ABA-SIL Miami Fall Meeting - ProgrammeaprotonPas encore d'évaluation

- Ipcc Newsletter Winter Issue 2016Document8 pagesIpcc Newsletter Winter Issue 2016aprotonPas encore d'évaluation

- Ipcc Newsletter Fall Winter 2018Document10 pagesIpcc Newsletter Fall Winter 2018aprotonPas encore d'évaluation

- The European Regulations 2016 - 1103 and 2016 - 1104Document4 pagesThe European Regulations 2016 - 1103 and 2016 - 1104aprotonPas encore d'évaluation

- ABA-SIL IPCCNewsletter July 2017Document13 pagesABA-SIL IPCCNewsletter July 2017aprotonPas encore d'évaluation

- AIJA 55th BIrthday Celebration 23-24 June 2017Document2 pagesAIJA 55th BIrthday Celebration 23-24 June 2017aprotonPas encore d'évaluation

- LJUBLJANA - Program 29 June - 1 July 2017Document8 pagesLJUBLJANA - Program 29 June - 1 July 2017aprotonPas encore d'évaluation

- ABA SIL - IPCC Newsletter - Spring2016Document8 pagesABA SIL - IPCC Newsletter - Spring2016aprotonPas encore d'évaluation

- ABA Presentation - Game of ThronesDocument12 pagesABA Presentation - Game of ThronesaprotonPas encore d'évaluation

- About The EU Regulation Related To International and Cross-Border SuccessionsDocument5 pagesAbout The EU Regulation Related To International and Cross-Border SuccessionsaprotonPas encore d'évaluation

- Brighton Aija ABA-SIL ProgramDocument8 pagesBrighton Aija ABA-SIL ProgramaprotonPas encore d'évaluation

- EU Regulation International Related To International SuccessionsDocument5 pagesEU Regulation International Related To International SuccessionsaprotonPas encore d'évaluation

- 2015 ABA-SIL AFRICA FORUM in Nairobi, Kenya - June 4-5Document7 pages2015 ABA-SIL AFRICA FORUM in Nairobi, Kenya - June 4-5aprotonPas encore d'évaluation

- 2015 Spring Symposia BrochureDocument24 pages2015 Spring Symposia BrochureaprotonPas encore d'évaluation

- Program AEA-EAL Gdansk 13-15 Juin 2013Document6 pagesProgram AEA-EAL Gdansk 13-15 Juin 2013aprotonPas encore d'évaluation

- 6davos ProgramDocument8 pages6davos ProgramaprotonPas encore d'évaluation

- Aba Sil Mipim FlyerDocument2 pagesAba Sil Mipim FlyeraprotonPas encore d'évaluation

- Program Congrès AEA-EAL 2014 CracowDocument6 pagesProgram Congrès AEA-EAL 2014 CracowaprotonPas encore d'évaluation

- AIJA50ème Anniversaire - Contribution APDocument3 pagesAIJA50ème Anniversaire - Contribution APaprotonPas encore d'évaluation

- Cannes MIPIM 2013 - ABA-SIL & AIJA Joint SeminarDocument8 pagesCannes MIPIM 2013 - ABA-SIL & AIJA Joint SeminaraprotonPas encore d'évaluation

- Programme Session Genève 2006Document2 pagesProgramme Session Genève 2006aprotonPas encore d'évaluation

- Rapport Général Et Raport National 2003Document38 pagesRapport Général Et Raport National 2003aprotonPas encore d'évaluation

- Ws PCC NR France 2010Document13 pagesWs PCC NR France 2010aprotonPas encore d'évaluation

- Rapport Général 2003Document10 pagesRapport Général 2003aprotonPas encore d'évaluation

- AIJA PCC Seminar - May 2009, 23.1Document2 pagesAIJA PCC Seminar - May 2009, 23.1aprotonPas encore d'évaluation

- AIJA PCC Seminar - May 2009, 23.1Document2 pagesAIJA PCC Seminar - May 2009, 23.1aprotonPas encore d'évaluation

- Dealing With Nouveau Super Riche (FV)Document1 pageDealing With Nouveau Super Riche (FV)aprotonPas encore d'évaluation

- WSC AIJA PARIS Academic Booklet 18 08 08Document1 pageWSC AIJA PARIS Academic Booklet 18 08 08aprotonPas encore d'évaluation

- Verbier ProgrammeDocument8 pagesVerbier ProgrammeaprotonPas encore d'évaluation

- Money, Banking, and Monetary Policy: ObjectivesDocument9 pagesMoney, Banking, and Monetary Policy: ObjectivesKamalpreetPas encore d'évaluation

- Manila City - Ordinance No. 8330 s.2013Document5 pagesManila City - Ordinance No. 8330 s.2013Franco SenaPas encore d'évaluation

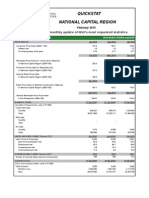

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocument3 pagesQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiPas encore d'évaluation

- Boat Bassheads 100 Wired Headset: Grand Total 439.00Document1 pageBoat Bassheads 100 Wired Headset: Grand Total 439.00Somsubhra GangulyPas encore d'évaluation

- Receipt ClerkDocument1 pageReceipt Clerksonabeta07Pas encore d'évaluation

- Quiz #2 - Week 03/08/2009 To 03/14/2009: 1. Indifference Curves Are Convex, or Bowed Toward The Origin, BecauseDocument6 pagesQuiz #2 - Week 03/08/2009 To 03/14/2009: 1. Indifference Curves Are Convex, or Bowed Toward The Origin, BecauseMoeen KhanPas encore d'évaluation

- 25-JUNE-2021: The Hindu News Analysis - 25 June 2021 - Shankar IAS AcademyDocument22 pages25-JUNE-2021: The Hindu News Analysis - 25 June 2021 - Shankar IAS AcademyHema and syedPas encore d'évaluation

- International Management+QuestionsDocument4 pagesInternational Management+QuestionsAli Arnaouti100% (1)

- SCHOOLDocument18 pagesSCHOOLStephani Cris Vallejos Bonite100% (1)

- Pay Slip For The Month of April 2018Document1 pagePay Slip For The Month of April 2018srini reddyPas encore d'évaluation

- Tugas Problem Set 5 Ekonomi ManajerialDocument3 pagesTugas Problem Set 5 Ekonomi ManajerialRuth AdrianaPas encore d'évaluation

- Congo Report Carter Center Nov 2017Document108 pagesCongo Report Carter Center Nov 2017jeuneafriquePas encore d'évaluation

- Mixed Use Traffic Impact StudyDocument77 pagesMixed Use Traffic Impact StudyusamaPas encore d'évaluation

- CV Siti Nur Najihah BT Nasir 1Document1 pageCV Siti Nur Najihah BT Nasir 1sitinurnajihah458Pas encore d'évaluation

- Indian Economic Social History Review-1979-Henningham-53-75Document24 pagesIndian Economic Social History Review-1979-Henningham-53-75Dipankar MishraPas encore d'évaluation

- Proforma Invoice No - SI20171103 of PONo. 02KINGDAINDEX-2017Document1 pageProforma Invoice No - SI20171103 of PONo. 02KINGDAINDEX-2017lê thu phươngPas encore d'évaluation

- Midc MumbaiDocument26 pagesMidc MumbaiparagPas encore d'évaluation

- Sbi Po QTN and AnsDocument6 pagesSbi Po QTN and AnsMALOTH BABU RAOPas encore d'évaluation

- Writing A Case Study ReportDocument9 pagesWriting A Case Study ReportjimzjPas encore d'évaluation

- Red Sun Travels in Naxalite Country by Sudeep Chakravarti PDFDocument218 pagesRed Sun Travels in Naxalite Country by Sudeep Chakravarti PDFBasu VPas encore d'évaluation

- Ker v. Lingad 38 SCRA 524Document1 pageKer v. Lingad 38 SCRA 524Kent UgaldePas encore d'évaluation

- Looting Ukraine - How East and West Teamed Up To Steal A CountryDocument24 pagesLooting Ukraine - How East and West Teamed Up To Steal A Countryvidovdan9852Pas encore d'évaluation

- Executive Summary of PJTDocument3 pagesExecutive Summary of PJTnani66215487100% (1)

- September October LD Debate Kritik (Neg)Document5 pagesSeptember October LD Debate Kritik (Neg)RhuiedianPas encore d'évaluation

- Power For All - ToolsDocument6 pagesPower For All - Toolsdan marchisPas encore d'évaluation

- Value ChainDocument31 pagesValue ChainNodiey YanaPas encore d'évaluation