[1 _[Neme oF te assessee g Indian 74

{a [address “tiigsaia House, SR, Bahadur Shah Zafar Ware, ~

| _ New Delhi 120 002

(3 [Paw [AAacyas5a,

: 4 a — =

(4. | Circle Exemption Circle-i(1), New Delhi

5. [Status Section 25 Company

& | Previous Vear ending | 31.03.2011

17. [Assessment Year "2011-42 ~ |

&. | Dates of Hearing Several dates as summarized in Table-2 of this order

Sj Order under section | 143(3)/147 of the 17 Act, 1962

| Date ofOrder 27.42.2017

ASSESSMENT ORDER

Brief Details of the Assessee and return of income for the year:

The assessee, Young Indian (¥Ij, an association, is registered as @ company on 23.13.2010 for

promoting abjects of the nature specified in clause (1) of sub-section (1) of section 25 of the Companies

‘Act 1956, The assessee was also granted registration u/s 124 read with section 12AA of the income Tax

‘Act, 1961 (the Act) vide order bearing no. DIT(E)/2011-12/100DEL-YR21296-06052011 dated 09.05.2022

wc, AY, 2011-12.The assessee was Incorporated with authorized share capital of 5,000 shares of Rs.

1100/- each and the paid-up share capital of the assessee as on 31.03.2011 was Rs. 5,00,000/-. The

company was granted license u/s 25 of the Companies Act, 1956 on 18.11.2010 to promote the objact of

the nature as specified in section 25, sub-section (1), clause (a) of the Companies Act, 1956.

1.2 AS per Memorandum of Association (MOA), Mr, Suman Dubey and Mr. Satyan Gangaram

Pitreda were the Founder Members and shareholders (subscribing 550 shares each). The assessee

company has disclosed fist of shareholders and directors of the Company during AY 2011-12 as under:

_ _ = Table-t

Name Position in Vi & No. of shares held

‘Mis. Sonia Gandhi Director since 22.01.2011

_ E _ 1900 shares (385) _

ir. Rahul Gandhi Director since 13.12.3010

- E -1900 shares (38%)

Mir. Moti tai Vora Director since 22.01.2031

Lo | 600 shares (12%) 7

[iar Oscar Fernandes Director since 22.01.2011

| ema -600 shares (1296)

Wir. Satyan Gangaram Pitrada @ Sam | Nirector since 23.11.2010 |

Pitrods Held 550 shares but transferred it to Mr. Oscar Fernandes

| ‘Mr. Suman Dubey Director since 23.11.2010

7 Held 550 shares but transferred it to Mr. Moti tal V

As per MOA, the main object.of the company was:

“(1) To inculcate in the mind of India’s youth commitment to the ideal of a democratic ond secuiar

society for its entire populace without any distinction as to religion, caste.or creed and to awaken

India’s youth to participate in activities that may promote the foregoing objective in any manner

whatsoever including, without limitation, participating in all démocratic activities through open

and transparent electoral process, s0 as to conform to the ideals of the founding fathers of India

Mahatma Gandhi and Pandit j, Jawahar Lal Nehru:

(2) No object of the company will be carried out without obtaining prior approval/ no objection

certificate from the concern competent authority wherever required and/or prescribed.”

Extracted from Memorandum of Association of the assessee dated 14.10.2010]

In addition to above, the MOA has also incorporated subsidiary objects incidental/ ancillary only

to the attairment of above referred main object.

1.3 After incorporation of the company, the assessee filed an application before Director of income

Tax (Exemption), now designated as Commissioner of Income Tax (Exemption) for registration u/s 12.

T.w.s. 12AA of the Income Tax Act, 1961 (the Act) and the registration was granted to-the assessee u/s

212A r.w.s. 12AA by the Director of Income Tax (E) vide order dated 69.05.2011 on G. No, 2011-

12/100DEL-/R21296-06052011 w.e.f. AY 2011-12 subject to following terms and conditions:

‘+ Order u/s 12A(a) read section 12AA(1)(b) does not conform any right of exemption upon the

applicant u/s 11, 12 and 13 of the Income Tax Act, 1961. Such exemption from taxation will be

available only after the Assessing Officer is satisfied about the genuineness of the activities

promised or claimed to be carried on in each Financial Year relevant to the Assessment Year

andall the provisions of faw acted upon.

‘+ The Trust/ Society/ Non-profit Company shall comply with the provision of section 139A(1)(Ii)

and (i) of the Act within one month of the date of this order to obtain a Permanent Account

Number and shall communicate the PAN to this office,

‘+The Trust/ Society/ Non-profit Company shall maintain accounts regularly and shall get these

audited in accordance with the provisions of section 12A(b) of the Income Tax Act, 1961.

Separate accounts in respect of each activity and specified in rhemorandum shall be maintained.

A copy of such account shall be submitted to the Assessing Officer. A public notice of the

activitles carried on/ to be submitted to the Assessing Officer. A public notice of the activities

carried on/ to be carried on and the target group(s) {intended beneficiaries) shall be duly

isplayed at the Registered/ Designated Office to the organization.

‘+ Separate books of accounts in respect of profits and gains of business incidental to attainment

of cbjects shall be maintained in compliance to section 11(4A) of the Income Tax Act 1964.

* All the Public Money so received including for Corpus or any contribution shall be

communicated to this office.

+ No change in the Trust Deed/, Memorandum of Association/ instrument shall be affected

without the approval of the jurisdictional High Court/ Appropriate Authority and it shall

continue to serve the main object of the-trust in further without any change.

* No asset shall be transferred without the knowledge of the undersigned to anyone, including to

any Trust/ Society/ Non-profit Company, etc.

+ The registered office or the principal piace of activity of the applicant should not be transferred

outside the national capital territory, Delhi except with the prior approval of the DIT(E), Delhi

If later on, it is found that the registration has been obtained fraudulently by misrepresensation

or suppression of any fact, thé Registration so granted is liable to be cancelled as per provisions

v/s L2AA(3) of the Act,

‘No fee or any other consideration shall be received which comes under the proviso to section

215) of the Income Tax Act.

It is pertinent to mention that on the basis of above referred registration u/s 12A of the Act, the

assessee had claimed exemption of the income u/s 11 and 12 of the Act for assessment years 2011-12 to

2016-17.

1.4 The assessee filed its return for AY 2011-12 on 11.10.2011 disclosing aloss of Rs. 51,99,276/-.

The case was processed u/s 143(1) of the Act on returned loss. Since, the YI was registered u/s 12A of

the Act, it was entitled for tax exemption.

Analysis of legal framework governing the Assesse

2. It is evident from the above discussion that the assessee was incorporated as nonprofit

organization to promote the object as stipulated under MOA and was granted license u/s 25 of the

Companies Act, 1956 on 18.11.2010. As discussed earlier, the main objects of the assessee as disclosed

under MOA were:

To inculcate in the mind of India’s youth commitment to ideals of a democratic and secular

society without any distinction as to religion, cast or creed, and

To awaken India’s youth to participate in activities that may promote the foregoing objective in

any manner by participating in all the democratic activities, so as to conform to the ideals of

founding fathers of India, Mahatma Gandhi and Pandit Jawahar Lal Nehru.

MOA also incorporate subsidiary objects incidental/ ancillary to the attainment of above referred

main object.

2.1 Keeping in view the above object of the assessee, it was registered u/s 25 of the Companies Act,

1956. The provision of section 25 reads as under:

“25. Pawer to dispense with” Limited” in name of charitable or other company.

(4) Where it is proved to the satisfactidn of the Central Government that an association-

{a} is cout to be formed as a limited company for promoting commerce, art, science, religion,

charity or any other useful object, and

{b) intends to apply its profits, if any, or other income in promoting its objects, and to prohibit the

payment of any dividend to its members, the Central Government may, by licence, direct that the

association may be registered as a company with limited liability, without the addition to its name

of the word" Limited" or the words" Private Limited".

(2) The association may thereupon be registered accordingly; and on registration shall enjoy all

the privileges, and (subject to the provisions of this section) be subject to all the obligations, of

limited companies.

(3) Where it is proved to the satisfaction of the Central Government-

“s

{g) thot the objects of a company registered under this Act as a limited company are restricted to

those specified in clause (a) of sub- sectian (2); and

(0) that by its constitution the company is required to apply its profits, if any, or other income in

Promoting its objects and is prohibited from paying any dividend to its members,

the Central Government may, by licence, authorise the company by a special resolution to change

its name, including or consisting of the omission of the word" Limited” or the words" Private

Limited’; and section 23 shall apply to a change of name under this sub- section as it applies to a

chonge of name under section 21

[AJA firs may be @ member of any association or company licensed under this section, but on the

dissolution of the firm, its membership of the association or company shall cease.

GIA licence may be granted by the Central Government under this section on such conditions ond

subject to such regulations os it thinks fit, and those conditions and regulations shall be binding on

the body to which the licence is granted, and where the grant is under sub- section (1), shall, if she

Central Government so directs, be inserted in the memorandum, or in the articles,

one and partly in the other.

{6] It shall not be necessary for a body to which a licence is so granted to use the word" Limited" or

the words" Private Limited” as any part of its name and, unless its articles otherwise provide, such

body shalt, if the Central Government by general or special. order so directs and to the extent

specified in the direction, be exempt from such of the provisions of this Act as may be specified

therein.]

(2) The Icence may at any time be revoked by the Central Government, and upon revocation, the

Registrar shall enter the word" Limited” or the words" Private Limited" at the end of the name

upon the register of the body to which it was granted: and the body shall cease to enjoy the

exemption granted by this section: Provided that, before a licence is so revoked, the Central

Government shall give notice in writing of its intention to the body, ond shall afford it an

opportunity of being heard in opposition to the revocation.

{8) (a) A body in respect of which a licence under this section is in force shall not alter the

provisions ofits memorandum with respect to its objects except with the previous approval of the

Centrol Government signified in writing.

(b) The Central Government may revoke the licence of such a body if it contravenes the provisions

of clause (a).

{cl In according the approval referred to in clause (a), the Central Government may vary tne

licence ty making it subject to such conditions and regulations as’ that Government thinks fit, in

lieu of, er in addition to, the conditions and regulations, if any, to which the licence was formerly

subject.

{d) Where the alteration proposed in the provisions of the memorandum of a body under this sub-

section is with respect to the objects of the body so far as may be required to enable it to do any of

the things specified in clauses (a) to (9) of sub- section (1) of section 17, the provisions of this su>-

section shail be in addition to, and not in derogation of, the provisions of that section.)

{21 Upon the revocation of a licence granted under this section to a body the name of which

contains the words" Chamber of Commerce", that body shall, within a period of three months from

the date of revocation or such longer period as the Central Government may think fit to allow,

change its name to a name which does not contain those words; and-

(a) the aotice to be given: under the proviso to sub- section (7) to that body shall include a

statement of the effect of the foregoing provisions of this sub- section; and

{6} section 23 shall apply to a change of name under this sub- section as it applies to a change of

name under section 21.

or partly in the

(10) If the body makes defoult in complying with the requirements of sub- section (9), it shall be

punishable with fine which may extend to five hundred rupees for every day during which the

default continues. Articles of Association.”

A careful perusal of provisions of section 25 of the Companies Act, 1956 has revealed that

registration u/s 25 of the Companies Act is subject to certain conditions and contravention of these

conditions will lead to punishment with fine.

2.2 The assessee was also granted a registration u/s 12A of the Act subject to certain conditions as

enlisted above. The assessee, on the basis of registration u/s 12A, had claimed tax exemption from AY

2011-12 onwards. Later on, CIT(E) has cancelled the registration granted to the assessee u/s 12A vide

order bearing F. No. CIT(E)/12A/2017-18 dated 26.10.2017 and had withdrawn exemption granted to

the assessee w.e.f. AY 2011-12 onwards. For the sake of convenience, relevant part of order u/s 124A(3}

is extracted below:

“18. In view of the above findings which remained uncontroverted by the assessee, | am satisfied

that the activities of assessee are not genuine and are not being carried out in accordance with its

objects. Accordingly, the exemption granted to the assessee u/s 12A read with section 12AA of the

Income-tax Act, 1961 bearing reference number G. No. DIT{E)/2011-12/100DEL-YR21256-

06052011 dated 09.05.2011 is hereby withdrawn with effect from AY 2011-12 and onwards.”

[Extracted from order u/s 12AA(3) on F. No. CIT(E)/12A/2017-18/169 dated 26.10.2017]

The effect of order of CIT(E) u/s 12AA(3) is that no tax exemption is available to the assessee

during year under consideration.

3. Brief details of reopening the assessment u/s 147 of the Act: In this case, the return of income

of the assessee for the year under consideration was processed u/s 143(1) of the Act and no assessment

‘was made in terms of sub-section (8) rw. sub-section (40) of section 2 of the Act. Subsequent to the

processing of return, an information was received from the Investigation Wing of the income Tax

Department, Delhi that the assessee had purchased loan of Indian National Congress (AICC) to

Associated Journals Ltd. (AJL) of Rs. 90.21 crore for a paltry sum of Rs. 50 lac and immediately after the

assignment of loan to the assessee, AJL allotted 99% of shares to the assessee in liew of the alleged loan

of Rs. 90.21 crore. in other words, the impugned transaction of purchase of loan was followed by

another trensaction of allotment of shares of AJL to the assessee leading to acquisition of properties of

AJL by the assessee as well as accrual of benefit from business assets of the AJL. After the receipt of the

information, the copies of the return of income and audited income & expenditure a/c for the year

under consideration were scrutinized and further enquiries were made from parties to the transaction

u/s 131 and 133(6) of the Act. The information was also called for from the Registrar of the Companies.

Taking intc account, the result of enquiry and facts of the case, it was noticed that income chargeable to

tax had escaped assessment during the year under consideration, Accordingly, the reassessment

proceedings u/s 147 were initiated by recording reasons to believe that income chargeable to tax had

escaped assessment for the year under consideration. For the sake of convenience, the relevant part of

reasons recorded for the issue of notice u/s 148 of the Act is extracted below:

reels

"6. Summaryof Escapement of Income

6.1it is evident from the enquiry u/s 133{1) of the Act as sequel to the information received

fram the Investigation Wing and other sources that following undisputed sequence of

events of this deal has token place in taking over of the AIL by the Yi

1) Shri Suman Dubey, Shri Satyan Gangaram Pitroda and Mr. Oscar Fernandes, found

members of M/s Young indian became directors of the AJL on 21.12.2010 and 17.06.2610

respectively along with Mr. Motilal Vora, Chairman of M/s AJL all close associates of Smt.

Sonia Gandhi.

2) A resolution was passed on 01.09.2010 to shift registered office of the AIL from Lucknow to

Delhi.

3) M/s Young Indian, a section 25 company was incorporated on 23.11.2010 with founder

members namely Sh. SumanDubey and Sh. Satyam Gangaram Pitroda who later transferred

their shares to Mrs. Sonia Gandhi, Rahul Gandhi, Motilal Vora and Oscar Fernandes having

office address of 5A, Bahadur Shah ZafarMarg, New Delhi (a property owned by the AIL)

with share capital of Rs. 5 lakh.

4) The alleged loan of fis. 90 crore was transferred by the AICC to M/s Young Indian on

16.12.2010 (within 25 days from date of incorporation) however the alleged loan was

assigned though a letter dated 28.12.2010 to M/s Young Indian.

5) Av the time when loan of Rs. 90 crores was assigned to M/s Young Indian for Rs. 50 lac it

had no fund to make payment of Rs. 50 lac. Later, it took loan of Rs. 1 crore from M/s

Dotex Merchandise Pvt. Ltd. on 15.02.2011 i.e. two months from the date of assignment of

Ican of Rs. 90 to M/s Young Indian.

6) 1V/s AIL allotted 9,02,16,898 shares to M/s Young India on 26.02.2011 in lieu of assignment

of loan of Rs. 90 crore to M/s Young Indian.

7) M/s Young Indian paid Rs. 50 lac to AICC on 01.03.2011 for loan of Rs. 90 crore which was

‘assigned to it on 16.12.2010.

8) M/s Young Indian did not disclose the transaction of loan of Rs. 90 crore at paltry sum of

Rs. 50 lac in its P&L A/c. The same was camouflaged as expenditure on prescribed object

of the M/s Young Indian.

9) The Young Indian citing object of the company obtained registration u/s 12A of the Income-

tax Act on 09.05.2011 so that value of all benefit from real estate business of the AiL get tax

exemption.

10) In order to achieve object of taking over 100 percent shares of the AIL by M/s Young

Indian and Smt. Sonia Gandhi, MP, Shri Rahul Gandhi, MP and Smt. Priyanka Gandhi

Vadhera also purchased addition 47,513 and 2,62,411 shares of the AJL through Rattan

Deep Trust and Janhit Nichi Trust respectively.

The above referred to sequence of events have been summarized in the following

table for the sake of clarity:

Sr. Date Details of Prima Facle

No. Event Purpose/

of Remark

| step ose _ :

1 02.04.2008 Business of publication of | Purpose was to use

newspaper closed and | property of M/s

vases

ory

GLa

a

we

2

VAS was offered to all

employees and the same

was accepted on |

92.04.2008

Associated Journals

Limited (the AlL) worth

of several thousand

crore for other

commercial purpose.

17.06.2010 ‘Mr. Oscar Fernandes, a | To facilitate takeover of

close associate of Smt. | the AlL by M/s Young

Sonia Gandhi and Sh. | Indian (the YY).

Rohul Gandhi and

Member of M/s Indian

National Congress (the

AICC) appointed as

. Director of Alt

"01.09.2010 Resolution was passed by | To facilitate takeover and

the Board of Directors to | to provide easy and

shift the Registered | efficient contro! by ‘Smt.

Office of the AL from | Sonia Gandhi and Sh.

pele Lucknow to Delhi. Rahul Gandhi. =

23.11.2010 The Yl, @ section 25 | It is evident from address

company, wos | of reaistered office of the

incorporated with Mr. | YI that since its

Suman Dubey, Mr. | incorporation, it had

Satyan Gangaram | started treating property

Pitroda with paltry | of the AlL as its own.

capital of Rs. 5 lacs

having registered office

at 54, Bahadur Shah

Zafar Marg, New Delhi, a

property of All.

13.12.2010 ‘Mr. Rahul Gandhi was |~Just three days before

appointed as Director of | assignment of alleged

the YI. Joan of Rs. 90 to the YI by

: the AICC for paltry sum of

. Rs, 50 lacs.

= 16.12.2010 The AICC claimed | it is not known how a

assigning its alleged loan | foan could be assigned

Of Rs, 90 crore with the | earlier to assignment

All to the YI for paltry | deed dated 28.12.2010

sum of Rs. $0 lacs vide | and when the YI had

assignment deed dated | capital of only Rs. 5 lacs

28.12.2010. ie. no capacity to pay

even paltry sum of 2s. 50

lacs.

21.12.2010 ir. Suman Dubey and

‘Mr. Sam Pitroda, Director

of the YI were also

appointed Director of the

‘Appointment of the

Director of YI as Director

of the Alt before

allotment of the share of

Paar?

All,

the AJL to the Yi defies ail

the established norms.

However, this step

provided total control of

the AJL to trusted man of

Gandhi Family (Mr. Oscar

Fernandes, Mr. Suman

Dubey ond Mr. Sam

Pitroda as director and

‘Mr. Motilal Vora as MO

of the AL)

28.12.2010

It was stated that loan

was assigned * by

assignment deed dated

28.12.2010. however, no

such deed was furnished

before the AO and only a

copy of letter dated

28.12.2010 was filed

assigning loan of Rs. 90

crore.

it is not known thet why

loan was transferred on

16.12.2010 much before

the date of assignment

deed? The letter dated

28.12.2010 proposing

assignment of loan was

not even acknowledged

by the AIL as token of

acceptance of such

transfer.

22.01.2011

‘Mis. Sonia Gandhi, Mr.

Motilal Vora and Mr.

Oscar Fernandes were

appointed as Director of

YI.

Control of the AN was

transferred to the YI by

way of common director |

before allotment of

shares.

10

15.02.2011

V1 claimed receiving loan

of Rs. 1 crore from M/s

Dotex Merchandise Pvt.

Ltd. to make payment of

Rs, $0 lacs to the AICC.

When the allegea loan

was assigned to the YI it

had no money to pay

consideration Rs. 50 lacs

for assignment of such

Joan and surprisingly, it

claimed taking loan of Rs.

1 crore after two months

from the date of

assignment of loan of Rs.

90 crore to it.

if

26.02.2011

The A aillotted

9,02,16,898 shares to the

Yiin lieu of assignment of

alleged loan of Rs. 90

crore to the YI for Rs. 50

lacs,

Allotment of shares which

constitute 99% of shares

of the AIL completed

tokeover of the AIL by the

Yh

12

(01.03.2021

The YI paid Rs. 50 lacs to

the AICC for assignment

of loan of Rs. 90 crore on

No prudent management

will ossign a loan of Rs.

90 crore for a paltry sum

6.2 Income from investment of Rs.

ase 19

of Rs. 50 lacs that too

| tos ceed spre gop

| of more than 2 months

from the date of

assignment.

Fone take note of the above referred to illogical sequence of events (e.g. step 8

should precede step 6, step 10 should precede step 6, step 12 should follow step 6

simultaneously, etc.) and the celerity at which these transactions were made by common

office bearers of the AJL, the YI and the AICC then conclusion is simple to guess that Mrs

Sonia Gandhi and Mr. Rahul Gandhi along with their trustworthy associates have taken over

property of more than Rs. 2000 crore for a paltry sum of Rs. 50 lacs,

50 lac

{tis evident from findings as recorded in para-5 that above referred to transactions/

arrangements were not real and genuine and were sham transactions. A pre-mediated

scheme was devised to obtain control aver immovable properties of the All worth of several

‘uncred crore by person who have incorporated Yi. The scheme consisted of following eight

steps to takeover immovable properties of the AIL without paying any taxes on benefits

accrued to the ¥I and its majority shareholders.

‘Step 1: It is evident from above referred to findings that as a first step the registered office

of Ail was shifted from Lucknow to Delhi and a new company, the YI was incorporated

wholly owned by some important persons (Smt. Sonia Gandhi, Sh. Rahul Gandhi, Sh. Motilal

Vora, Sh. Oscar Fernandes} who were also Office bearers of AICC of Indian National

Congress and Chairman and Directors of the AJL (Sh. Motilal Vora, Chairman and Sh. Oscar

Fernandes, Director).

Sten2: The newly incorporated company had no assets of its own except those transferred

by the AICC of indian National Congress ie, fund of Rs. 90.21 crore which was camouflaged

2s sale of loan of Rs 90.21 for meager sum of Rs. 50 lac and Rs. 1 croreewas arranged

through M/s Dotex Merchandise Pvt. Ltd, (prima facie by launtéering of own money of YI) a

company with dubious antecedents and the loan of Rs. 1 crore was also flagged os

Suspicious transaction in the STR by FIU, india. The amount of loan of Rs. 90.21 crore was

fixed in order to ensure that the amount is just sufficient to allot 99% of share of the AIL to

the Yl.

Sten 3: The Yi, which was registered u/s 25 of the Companies Act, 1956 for charitable

Purpose has no business or income ofits and had not carried out any activities for the object

Of the company in FY 2010-11 and FY 2011-12. It has carried out only adventure which wos

‘in nature of trade to takeover real estate business of the AL to its benefit.

Step_4: The alleged sale of loan of Rs. 90.21 crore to the Y! was not proved through

document because assignment of loan was not acknowledged and confirmed by the AIL. In

this context, itis important to highlight the quantum of alleged loan of Rs. 90.21 was also @

Pre-fixed amount which was just sufficient to allot 99 percent shares of the All to the YL

Even before transaction of purchase of loan of Rs. 90.21 crore could be complete by making

payment of Rs. 50 lac to the AICC, on 01.03.2014 the A/L increased its authorized capital

from 2 crore ordinary share having {foce value of Rs. 10) to 10 crore ordinary share {face

value of Rs. 10) and allotted 9.021 crore shares (99% of total paid up capital) to the Yi oa

26.C2.2011 on the basis of incomplete and undated share application forin

Stee S:The tokeover of the AJL was complete within three months from the date of

incorporation. After taking over all the immovable properties of the AJL in control, the YI

shifted to Herald House, Bahadur Shah Zofar Marg, New Delhi, one of prime properties of

the AIL worth of several hundred crore without paying any compensation for use of space to

the All Le. in reality the Yi used the property on the name of the AJL as its own property.

Stea 6. The ¥/ citing the object of the company obtained registration u/s 12 A of the Act

which entitled it to exemption on its income on 09.05.2011 so that value of all benefit from

realestate business of the All get tax exemption.

Step 7: In order to achieve object of holding 100 percent share of the AJL by the YI and its

majority shoreholders and their relative like Sh. Rahul Gandhi and Smt. Priyanka Gandh\

Vadhera hove purchased additional 47,513 and 2,62,411 shares through Rattan Deep Trust

‘andJanhit Nidhi Trust respectively.

Step 8: The V1 did not disclose the transaction of purchase of loan of Rs. 90.21 at the paltry

sum of RS. 50 lac in P&L A/c the Same wés camouflaged as expenditure on object of the YI

The value of 8.024 crore shares was also not disclosed in the balance sheet on the ground of

insignificant investment. The reason for above referred to accounting treatment was to hide

realtransaction,

For the purpose of deciding true character of above referred to pre-determined

scheme involving eight steps | have token note of aforementioned peculiar facts of this case

The Alt even though continues to remain a legal entity with a right to hold properties. The

tue character of the above transactions has to be judged by looking at reality ofter

removing or piercing the vell of these two companies and the AICC, as the above referred to

Citcumstances of the case justify such an exercise. The real purpose of the loan from Indian

National Congress and allotment of the share to the YI by the Alt in reality was only to

transfer immovable properties of the AJL to the YI along with full right over rental income

nd business income from real estate business of the AJL at paltry sum of Rs. 50 lac without

having paid any taxes. The above referred to-artificialy inserted steps have no business

Purbose except for evading taxes on income earned by the YI on the takeover of immovable

properties of the ALL.

In order to hide in above referred to pre-mediated scheme of tax evasion, the YI

resorted to unfair reporting of its financials like non-reporting of value of 9.021 crore shares

of the AIL in its balance sheet on the ground of insignificant investment. How come full

takeover of a company having property of worth of Rs. 1600 crore or more could be on

insignificant investment? The answer stare ot one’s face that actual reason for suppressing

the cransaction in P&L A/c and balance sheet was a conscious effort to avoid detection of

real transaction leading to payment of tax.

Page [30

in view of above, | have reasons to believe that income of the YI u/s 28{iv) rw.s

2423) had escaped assessment for AY 2011-12.At this point of time, cost of investman, of Bs.

32 ac by the Yi is known, however, Fair Market Value (FMV) of properties of the AL crs

26.02.2011 are not available due to non-cooperation by parties to transactions, buon

{heugh Metropolitan Court, Delhi has taken cognize of FMV of properties of the AIL above

£5, 1000 crore, the exact FMV of the all properties on the name of the AIL in India Is neg

known at the time of recording of reasons accordingly, the quantum of income u/s 2Blivjie.

fate of benefit accrued to the Yi from these assets minus cost of investment of Rs. 50 could

be not computed with the precision which shall be determined during reassessment

proceeding.

6.3 Unexplained loan of Rs, 1 Crore from M/s Dotex Merchandise Put, Ltd.

i

The Yi claimed taking a loan of Rs. 1 Crore from M/s Dotex Merchandise Put. Ltd,

Kolcata, a company known for providing bogus entries. The transaction is alse notified in

the STR of FIU India. The YI did not furnish any evidence of genuineness of the loom Prima

Jacie, it appears that the amount (Rs. 1 Crore) which appears to be money taundering of

been oney of ¥I as discussed earlier is an unexplained credit, as the source of which has not

been explained properly. The amount is required to be toxed u/s 68 of 7. Act. In views of

fhese facts, | have reason to believe that income of Rs. 1 crore has escaped assessment for

AY 2011-12,

6:4 Expenditure of Rs, 50 Lac by the Yi outside the Aims & Objects

As discussed above, the YI has paid an amount of Rs. 50 Lacs to the AICC for

Gcauiring the alleged loan from the AIL. Since making payments for acquiring loon to

takeover a real estate company do not form part of application of income for charitable

purposes, | have reason to believe that such expenditure isto be disallowed and added back

to the income of the YI for AY 2011-12. I have therefore reason to believe that income

amounting to Rs. §0,00,000/- has also escaped assessment,”

(Apart of reason extracted from reason recorded for issue of notice u/s 148 of the Act]

‘The notice u/s 148 along with reasons recorded for issue of the notice was issued and served on

the assessee on 10.01.2017 i.e: within the prescribed period of time.

2 not nee the receipt of notice u/s 148 along with reasons recorded, the assessee raised objection

aBainst the reasons so recorded for the issue of notice u/s 148 of the Act. The objections of the assessee

Geant the issue of notice u/s 148 were disposed off by the undersigned by way of « speaking order

dated 21.03.2017 and the same was served on the assessee on the same date.

3.2 Later on, the assessee filed a writ petition bearing no. (WP(C) No. 4087/2017) before Hon'ble

Delhi High Court against the initiation of reassessment proceedings u/s 147 of the Act. Hon'ble Delhi

High Court after having heard the objection of the assessee dismissed the wit Petition as withdrawn

vide orderdated 12.05.2017.The order of Hon'ble High Court is extracted below for ease ef reference:

“ORDER

% 12.05.2017

CM No. 17944 of 2017 [for exemption,

1. Allowed subject to just exceptions.

W.P-(C) 4087/2017 &CM No, 17942 of 2017 (for stay) & CM No. 17943 of 2017 (for permission to

file long synopsis) and CM No.18108/2017 (for placing on record correct documents)

2 OF, A.M. Singhvi, learned Senior counsel for the Petitioner, on instructions seeks leave

to withdraw this petition by stating that the Petitioner reserves liberty to urge before the

Assessing Officer (AO) ail pleas available to the Petitioner including questioning the conclusion of

the AQ that there are reasons to believe that income for the relevant Assessment Year escaped

assessment.

3. In view of the above statement, and expressing no opinion on merits, the Court dismisses the writ

petition as withdrawn with the liberty as prayed for. The AO will consider all pleas of the Petitioner

(on merits in accordance with law. The applications are disposed of

S.MURALIDHAR, J

CHANDER SHEKHAR, J

MAY 12, 2017"

Details of opportunities allowed to the assessee during the course of assessmént proceedi

4, ___Records of Assessment Proceedings: During the course of re-assessment proceedings, the

assessee was given opportunities of being heard u/s 143(2), 142(1) and 143(3) of the Act. The enqul

were also made u/s 133(6), 131 and 142(1) of the Act. in response to these notices, initially Shri Ankit

Aggarwal, CA attended the proceedings and later on, written replies were filed. Many times, the

assessee, instead of furnishing reply in responsé to the statutory notices had questioned legality of issue

of notice and power of the AO to call for information and the requisite information was not filed. The

details of notices issued and response of the assessee has been summarized as under

Table-2

Date of Particulars requested and details furnished

notice/

hearing 7 z

14.07.2015 __| Notice u/s 133(6) of the Act seeking information issued to the assesses.

21.07.2015 _| The assessee filed objection against the notice u/s 133(6) of the Act.

nnn The assessee further objected treating notice u/s 133(6) as invalid and how the

oe information called for is required for the purposes of the Act.

[27.07.2015 | PisPosing the objection, the assessee was requested to comply to the notice u/s

| 133(6) dated 14.07.2015. a 7 _ _ |

7 The assessee requested for a copy of approval of CIT for issue of notice u/s 133(6)

31.07.2015

of the Act -

(03.08.2015 _| The assessee was conveyed of such approval for Issue of notice u/s 133(6) of the

i Act by the CIT(Exemption), New Delhi

07.08.2015 | The assessee again objected requesting the copy of such approval

46.08.2015 | TRE assessee requested for inspection of records pertaining to the requisiion

issued by this o 7 :

12.08.2015 ‘The assessee again filed objection against the notice u/s 133(6) of the Act.

10.01.2017 | Notice u/s 148 of the Act along with the reasons recorded issued. _

30.09 3 The assessee filed submissions along with a request seeking the copy of th

09.02.2017

= sanction letter of the approving authority. 7

17.02.2017 | The documents requested vide letter dated 09.02.2017 was furnished to the

Pope 2

A

Xe

23.0

017

Preliminary dbjedons fled by the asessea.

21.03.2017 | The objections filed by the assessee were disposed off. Notices u/s 1430) &

g 142{1) of the Act along with the 14 point questionnaire issued

7 | The assessec requested four weeks time after disposal of the objections so that

30.03.2017

i appropriate remedy can be taken under law.

{47.04.2017 The request of the assessee for adjournment was accepted.

| The assessee submitted that it was in process of filing Writ Petition before the |

16.04.2017 | Hon'ble Delhi High Court. _

| 01.08.2017 As no further communication was received, the assessee was asked to submit

response to the questionnaire dated 21.03.2017.

03.05.2017 | Te assessee submitted that it had filed Writ Petition (WP [Diary] No, 217301 of

2017) before the Hon‘ble Court.

05.05.2017

As no confirmation about the writ petition was received, the assessee was asked

to comply by 09.05.2017.

05.05.2017

‘The AR of the assessee sought adjournment of 10 days as the matter is before

the Hon'ble Court.

the AR of the assessee filed the paper book containing the wek petition,

Copy of the order of Hon'ble Delhi High Court against the assessee’s writ

23.05.2017 __| petition (WP(C) No. 4087/2017 dated 12.05.2017) received dismissing the writ

__| as withdrawn, a 7

24.05.2017 _| Letter issued to the assessee for compliance to the reassessment proceedings

and was asked to submit response to the questionnaire dated 21.03.2017.

| 30.05.2017 | Part reply to the questionnaire dated 21.03.2017 was submitted in this office,

07.06.2017 | Further part details in reply to the questionnaire dated 21.03.2017 was

submitted 7 i 7

x Another set of part details in reply to the questionnaire dated 21.03.2017 was

13.06.2017

submitted. _

21.06.2017 Further part reply to the queries was received in this off _ |

28.06.2017 Adjournment sought and allowed. aa

x | The assessee further filed the part details as per the questionnaire dated

11072017 | 31032017.

38.07.2017 | The assessee again raised objections to the reassessment proceedings as well as

{28° submitted part details as per the questionnaire dated 21.03.2017. _

: ‘The additional objections raised were disposed off and the assessee was asked to

28.07.2017 __| submit the balance reply as per the questionnaire dated 21.03.2017 fixing the

case of hearing on 10.08.2017.

10.08.2017 __| The assessee reiterated the objections and again submitted the part reply te the

dated 21.03.2017. _ __

110.2017 __| Notice u/s 142(1) of the Act issued seeking details of all the assets own by M/s

a = _| The Associated Journals Limited as on 26.02.2011. a

20102017 | Te Feply of the assessee received denying its obligation to furnish any

_| information as sought vide notice dated 11.10.2017. a

‘Valuation report received from the Valuation Officers of Delhi, Lucknow, Patna

08.11.2017

and Panchkula confronted to the assessee.

13112017 _ | Valuation report received from the Valuation Officer of Mumbai and the

recalculated valuation on the basis of the information received from the o/o Jt.

‘Dist Reglitrar, Mumbai was conffonted to the assousee 7

15.11.2017 |The assessee requested for reasonable time (o respond on the issue ~

; The request of the assessee was accepted and the matter was adjourned to

teanzor7 | aaar2017, _ __}

20.11.2017 | TRE assessee requested for reasonable time OF one weak to respond on the

valuation report pertaining to Mumbai. -

Z The revised valuation report received from the Valuation Officer of Mumbal was

21.11.2017

2 confronted to the assessee

he ct i i

22.11.2017 | The assessee filed objection to the Valuation Reports pertaining to Delhi,

Lucknow, Patna and Panchkula.

27.11.2017 | The 235essee filed objection to the Valuation Report pertaining to Mumbai

jotice uy, Ae ith the final 5 notice i

08.12.2017 _ | Notice u/s 142[1) of the Act along with the final show cause notice issued to the

assessee. _ .

45.12.2017 __| The assessee filed reply vide weiten submission dated 154.2017.

18.12.2017 __| The assessee filed additional reply vide written submission dated 187.2017

“total 44 opportunities spread over 890 days,

It is evident from the details as summarized in the above table that even though 44

pportunities were allowed to the assessee and parties to transaction within a period of 890 days,

however, on several occasions, the assessee and AIC (a party to transaction) either challenged the

validity of notice and or had challenged right of the undersigned to call for information and on many

'ssues either no information or cryptic information were filed. This non-cooperative attitude of assessee

and parties to transaction has created huge problem in completing investigation and frame the

assessment order within a reasonable period of time, however, all the efforts were made to dispose off

all the objections of the assessee and parties to transaction with regard to the power of the AO to cal

for information to complete both investigation and assessment of income. The request of the assessee

Seeking multiple adjournments has also been allowed in order to enable it to file reply within time

period suitable to it.

'ssue 1: Deliberate non-compliance by the assessee during the course of assessment proceeding

5. In this case, parties to the transactions have made every effort to withhold the information

relevant for the assessment for one reason or the another as evident from a representative exarrple in

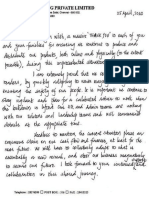

form of the scanned copy of fetter dated 21.07.2015

age 1

Exhibit 1

PP July 24, 2015,

ge a5

‘ShviD.S. Rawat A

Oy. Commissioner of income Tax (E}

Circle ~ 1(4)

Pratyaksh Kar Bhawan p

E2 Block, 24” Floor, Room No, 2618

Or SP. Mutter Civie Cents, JLN Marg

* Now Delhi 170002

St,

Res: ¥bung indian

PAN: AAACY 48250

Communication Ws. 1336) ofthe income Tex Aut, ‘95 1tHe Act) dated July

14, 2015

‘THe refs tothe captioned commnicatn ecelved by us on the same date

'n elation therato we submit as fellows:

2 + fhe ed communication seeks infamalon for vous years ‘tating with

® Previous Year 2010-11, ‘The years that are open for neral assessment aro

& et ans eeate 2013-14 and later years. Aso, na prdossdings undo ee

& Act are panding for any ofthe years plore AY 2018-48, Mays inate your

& Fomatos tte ete capined ormureaten you hve soe

information fr years for no aasessmant proceedngs or any proesedings are |

° pending under the Act

2 TAG brovons of secon 186) empower the Assessing Ofer sex

k Th hat noe celle Purposes oft Ac’ The said tao the ponies

é “Te Ack rasa tered by Courts to mean proooecings pending sale

& the Act, spas Bron of secson 183) can only be eck nape

ypieedings pending under te Act in sean rabanes paced ora

following decisions

* Hien Singh end ancterv. assistant Dector of lnvetgaton (246 TR

368) (MP)

© TPH 2s lays down te prnpe that ny inguy us. 121(1) and

TaIUA sf ai ectn under some provision of the Aa. hues Kad

Spee et the tom er the purposes of the At is rat exes

oe 2 pron sa wal stied principle Bata the stations

‘must ael tr thé purpose ofthe sate,

mre Gane we Vu wo wat 18 prowasa wm saaton Tt(T) that Ue

powers thereunder can only be exercised for ta purposes of fe ft

strat the term “or the purposes of the Act" must mean for the

proceedings pending under the Act

+ Jamnadas Madhavi & Co. V. Panchal 70 (162 ITR 334) (Bor)

sartwas he tat the powers us. 1918) could be exerisa byan oflear

‘only i proceedings are pending before such officer

43, the Hght ofthe foregoing, sins, nour cas, no proceedings are pending N

Maspodt of the years pir to AY 2013-14 no infomation ean tfuly be

‘sought under section 1336) in respect of ase years

44 Nowitnstansing the foraging lest pestion, you may nota that by vanens

ee rricatione inte past, we nad vont Fed wih you othe ings

creat nrmaten coveing abost af the Rems on wich you have re

nye aM complares: your ready reste, VE

re yements by You oes In tis rpocl are atached Hereieh, F

: ae rertore, appear, wih cespet, that you have fsuad fhe requersrt

{Ger secton 1336) wnat eppeaton of ‘mind in relation 10 Information

|, sroady available with you ove ast one yea!

5, Our assessment pending wih yous fom the AY. 2018-14, A rtereton

oe tee old show tat exorce of owes heron a on BS eh

the purposes ofthe Act’. Its our regret 10 recall that 2 so-called political

or poe pean ering on & campaign fr wichvhunt andthe mans Ne

ets oth ase! malar of prceadngs before ta Howble Hh Cou

TN May we, therefore, respedtufy cal upon you to ‘on the

osston reasonable nexus wih your tls a ou Assessing OSES

As submited eater, you eve rained a requirement orton te patio’

fs eapmenen no procesing ae ponding. Ths turer

Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- CFD factFindingCommittee ReportDocument49 pagesCFD factFindingCommittee ReportPGurus100% (1)

- Madurai HC Palani Temple JudgmentDocument22 pagesMadurai HC Palani Temple JudgmentPGurus100% (2)

- Subramanian Swamy's Letter To Speaker On Sonia Faking Qualifications Sept 28, 2020Document3 pagesSubramanian Swamy's Letter To Speaker On Sonia Faking Qualifications Sept 28, 2020PGurusPas encore d'évaluation

- Dr. K Kathirvel vs. CBI (Status Report)Document20 pagesDr. K Kathirvel vs. CBI (Status Report)PGurus100% (1)

- Letter To Prime Minister On AIIMS Investigation of SSRDocument3 pagesLetter To Prime Minister On AIIMS Investigation of SSRPGurusPas encore d'évaluation

- Letter To Prime MinisterDocument2 pagesLetter To Prime MinisterPGurus100% (1)

- Subramanian Swamy's Letter To Foreign Sec On Defmation Action Against UN Under Sec May 20, 2013Document3 pagesSubramanian Swamy's Letter To Foreign Sec On Defmation Action Against UN Under Sec May 20, 2013PGurus100% (2)

- Section 144 DetailsDocument2 pagesSection 144 DetailsPGurusPas encore d'évaluation

- Swamy Legal Notice To Indian ExpressDocument12 pagesSwamy Legal Notice To Indian ExpressPGurusPas encore d'évaluation

- APPWW Opposition To St. Paul ResolutionDocument3 pagesAPPWW Opposition To St. Paul ResolutionPGurusPas encore d'évaluation

- Subramanian Swamy's Letter To PM On Uttarakhand Temple Board May 27, 2020Document2 pagesSubramanian Swamy's Letter To PM On Uttarakhand Temple Board May 27, 2020PGurusPas encore d'évaluation

- MHA Order Dt. 30.5.2020 With Guidelines On Extension of LD in Containment Zones and Phased ReopeningDocument8 pagesMHA Order Dt. 30.5.2020 With Guidelines On Extension of LD in Containment Zones and Phased ReopeningPGurusPas encore d'évaluation

- MHA Order Dt. 17.5.2020 On Extension of Lockdown Till 31.5.2020 With Guidelines On Lockdown MeasuresDocument9 pagesMHA Order Dt. 17.5.2020 On Extension of Lockdown Till 31.5.2020 With Guidelines On Lockdown MeasuresThe Indian Express75% (16)

- Lockdown Extension & Guidelines - Press Release - 1st MayDocument7 pagesLockdown Extension & Guidelines - Press Release - 1st MayPGurusPas encore d'évaluation

- Telegraph 1Document1 pageTelegraph 1PGurusPas encore d'évaluation

- The Hindu Group Salary Cuts LetterDocument2 pagesThe Hindu Group Salary Cuts LetterPGurus100% (1)

- PM Speech On March 24, 2020Document6 pagesPM Speech On March 24, 2020PGurusPas encore d'évaluation

- Delhi Govt SuggestionsDocument7 pagesDelhi Govt SuggestionsPGurusPas encore d'évaluation

- Journalist UnionsDocument6 pagesJournalist UnionsPGurusPas encore d'évaluation

- Press Note 1Document6 pagesPress Note 1PGurusPas encore d'évaluation

- Press Note 2Document7 pagesPress Note 2PGurusPas encore d'évaluation

- Dr. Shiva Ayyadurai's Letter To President Donald TrumpDocument4 pagesDr. Shiva Ayyadurai's Letter To President Donald TrumpPGurus96% (24)

- GuidelinesDocument6 pagesGuidelinesThe Indian ExpressPas encore d'évaluation

- CM Letter PalgharDocument4 pagesCM Letter PalgharPGurusPas encore d'évaluation

- CommerceMin DirectiveDocument4 pagesCommerceMin DirectivePGurusPas encore d'évaluation

- Tax Department Notice To NDTVDocument32 pagesTax Department Notice To NDTVThe WirePas encore d'évaluation

- Indian Express CEO LetterDocument3 pagesIndian Express CEO LetterPGurusPas encore d'évaluation

- HMO Directives On The 21-Day Lock DownDocument1 pageHMO Directives On The 21-Day Lock DownPGurusPas encore d'évaluation

- 04 - Press Release On FM's Comments On SBI ChairmanDocument2 pages04 - Press Release On FM's Comments On SBI ChairmanPGurus0% (2)

- DR Swamy S Letter To PM 2020 03 20Document6 pagesDR Swamy S Letter To PM 2020 03 20PGurus100% (3)