Vous aimerez peut-être aussi

- Lifting of The Corporate VeilDocument7 pagesLifting of The Corporate VeilAmit Grover100% (1)

- Lifting of The Corporate VeilDocument6 pagesLifting of The Corporate VeilRishabh DubeyPas encore d'évaluation

- Company Law Incorporation Solomon V SoloDocument7 pagesCompany Law Incorporation Solomon V SoloPedro SegundoPas encore d'évaluation

- Lifting of The Corporate VeilDocument8 pagesLifting of The Corporate Veilitrisha3004Pas encore d'évaluation

- Lifting Corporate Veil ExplainedDocument7 pagesLifting Corporate Veil ExplainedJyothish Tj100% (1)

- Company Law Revision Part 2Document16 pagesCompany Law Revision Part 2bennyv1990Pas encore d'évaluation

- Lifting of The Corporate VeilDocument7 pagesLifting of The Corporate Veilguliasahil9588Pas encore d'évaluation

- Lifting the Corporate Veil: Piercing Entities to Prevent FraudDocument5 pagesLifting the Corporate Veil: Piercing Entities to Prevent FraudRahull DandotiyaPas encore d'évaluation

- Salomon V SalomonDocument11 pagesSalomon V SalomonDani ShaPas encore d'évaluation

- Analysis of Seperate Legal Entity Using Solomon. Solomon CaseDocument8 pagesAnalysis of Seperate Legal Entity Using Solomon. Solomon CaseHariharan ShekarPas encore d'évaluation

- Lifting of Corporate VeilDocument8 pagesLifting of Corporate VeilSupriya Prakash LimanPas encore d'évaluation

- Is a one-man company genuinely a companyDocument5 pagesIs a one-man company genuinely a companycwt721Pas encore d'évaluation

- LIFTING OF CORPORATE VIELDocument5 pagesLIFTING OF CORPORATE VIELRyan TapiseniPas encore d'évaluation

- Commercial V Social Veil LiftingDocument3 pagesCommercial V Social Veil LiftingMuhammad Aaqil Umer MemonPas encore d'évaluation

- Separate Legal Personality and Lifting The VeilDocument4 pagesSeparate Legal Personality and Lifting The Veilkusha100% (2)

- Lifting the Corporate Veil: A Discussion of Salomon and its ExceptionsDocument7 pagesLifting the Corporate Veil: A Discussion of Salomon and its ExceptionsHarri KrshnnanPas encore d'évaluation

- Lifting of Corporate VeilDocument12 pagesLifting of Corporate VeilHumanyu KabeerPas encore d'évaluation

- Assignment Company CompleteDocument24 pagesAssignment Company CompleteIzman Rozaidi75% (4)

- Piercing The Corporate Veil-Case DigestDocument3 pagesPiercing The Corporate Veil-Case DigestWalter OchiengPas encore d'évaluation

- Facts: Salomon V SalomonDocument4 pagesFacts: Salomon V SalomonSaumya AllapartiPas encore d'évaluation

- 1Document14 pages1Michelle HewPas encore d'évaluation

- End of Corporate PersonalityDocument12 pagesEnd of Corporate PersonalityNamamm fnfmfdnPas encore d'évaluation

- Law Term PaperDocument5 pagesLaw Term PaperLusajo MwakibingaPas encore d'évaluation

- Lifting of The Corporate VeilDocument4 pagesLifting of The Corporate VeilUmer UsmanPas encore d'évaluation

- Lifting of Corporate Veil-Ll B Iv 26-4-1Document9 pagesLifting of Corporate Veil-Ll B Iv 26-4-1Aritraa DasguptaPas encore d'évaluation

- Conceptual Analysis of Lifting the Corporate VeilDocument3 pagesConceptual Analysis of Lifting the Corporate VeilRahull Dandotiya100% (1)

- CL Tutorial FinalDocument8 pagesCL Tutorial Final璇詠Pas encore d'évaluation

- Companies Act 2006 Today. Although The Principle of Separate Legal Personality WasDocument9 pagesCompanies Act 2006 Today. Although The Principle of Separate Legal Personality WasGoo XuanxuanPas encore d'évaluation

- Salmon v. Salmon Case NotesDocument8 pagesSalmon v. Salmon Case Notesvasundhara dagaPas encore d'évaluation

- Corporate VeilDocument8 pagesCorporate VeilKaran BindraPas encore d'évaluation

- Renaldo Ramjohn 816024242 940790 1222522114Document6 pagesRenaldo Ramjohn 816024242 940790 1222522114ramjohnrenaldo46Pas encore d'évaluation

- Lifting The Corporate VeilDocument48 pagesLifting The Corporate VeilalexanderdroushiotisPas encore d'évaluation

- Company Law 1ST Internal AssismentDocument13 pagesCompany Law 1ST Internal Assismentnupur jhodPas encore d'évaluation

- UK Company Law Case Law Lists 2017Document25 pagesUK Company Law Case Law Lists 2017Ryan WongPas encore d'évaluation

- THE APPLICATION OF THE PIERCING OF THE CORPORATE VEIL RULE IN ZIMBABWE - Revised EditionDocument9 pagesTHE APPLICATION OF THE PIERCING OF THE CORPORATE VEIL RULE IN ZIMBABWE - Revised EditionTakudzwa Larry G ChiwanzaPas encore d'évaluation

- Separate Legal PersonalityDocument25 pagesSeparate Legal PersonalityKumar NaveenPas encore d'évaluation

- Siddhi Pawar 17010126474Document11 pagesSiddhi Pawar 17010126474Siddhi PawarPas encore d'évaluation

- Lifting The Corporate VeilDocument7 pagesLifting The Corporate Veilgaurav singh100% (1)

- (E) Separate Legal PersonalityDocument4 pages(E) Separate Legal PersonalityZhi Shen ChiahPas encore d'évaluation

- Company Law Third AssesmentDocument7 pagesCompany Law Third AssesmentMaharshi SharmaPas encore d'évaluation

- Assignment 3Document5 pagesAssignment 3Winging FlyPas encore d'évaluation

- KSLU Company Law Unit 1 and 2 Q and ADocument69 pagesKSLU Company Law Unit 1 and 2 Q and AMG MaheshBabuPas encore d'évaluation

- Lifting The Corporate VeilDocument8 pagesLifting The Corporate VeilJack YongPas encore d'évaluation

- (254306109) SSRN-id2352489Document22 pages(254306109) SSRN-id2352489Anirudh AroraPas encore d'évaluation

- Companies LawDocument12 pagesCompanies LawToo YunHangPas encore d'évaluation

- Company LawDocument4 pagesCompany LawAbhijithPas encore d'évaluation

- The Doctrine of Separate Legal Entity - A Case of Salomon Vs Salomon Co LTD T-1Document11 pagesThe Doctrine of Separate Legal Entity - A Case of Salomon Vs Salomon Co LTD T-1Munyaradzi Sean KatsandePas encore d'évaluation

- Coperate PersonalityDocument10 pagesCoperate PersonalitySimon PaulPas encore d'évaluation

- Salomon v. Salomon: Establishing the Separate Legal Personality of a CompanyDocument8 pagesSalomon v. Salomon: Establishing the Separate Legal Personality of a CompanyRashi MishraPas encore d'évaluation

- Introduction to Lifting the Corporate VeilDocument10 pagesIntroduction to Lifting the Corporate VeilZiko2billion100% (1)

- Salomon V A Salomon and Co LTD (1897) AC 22 Case Summary The Requirements of Correctly Constituting A Limited CompanyDocument5 pagesSalomon V A Salomon and Co LTD (1897) AC 22 Case Summary The Requirements of Correctly Constituting A Limited CompanyDAVID SOWAH ADDO0% (1)

- Corporate Law: By, Sanjana S Bhat 1812033Document16 pagesCorporate Law: By, Sanjana S Bhat 1812033Sanjana BhatPas encore d'évaluation

- Corporate Law NotesDocument71 pagesCorporate Law NotesKeyur Shah100% (1)

- Salomon V Salomon - Case SummaryDocument4 pagesSalomon V Salomon - Case SummaryParag KabraPas encore d'évaluation

- (Summary) Salomon V A Salomon - Co LTDDocument4 pages(Summary) Salomon V A Salomon - Co LTDNgọc Hân LêPas encore d'évaluation

- Compiled Case Summary Corporate Basics 1-2Document13 pagesCompiled Case Summary Corporate Basics 1-2Priya KulkarniPas encore d'évaluation

- Company Law Assignment DeadlineDocument8 pagesCompany Law Assignment Deadlinegherasimcosmina3014Pas encore d'évaluation

- CHAPTER THREE: The Legal Status of A Registered CompanyDocument5 pagesCHAPTER THREE: The Legal Status of A Registered CompanyYwani Ayowe KasilaPas encore d'évaluation

- MFM-Corporate Law NotesDocument72 pagesMFM-Corporate Law NotesjyotijagtapPas encore d'évaluation

- The Karnataka Stamp Act 1957Document55 pagesThe Karnataka Stamp Act 1957BasantPalsiPas encore d'évaluation

- Application For Cancellation and Registration of A Plan (Converson Plan)Document3 pagesApplication For Cancellation and Registration of A Plan (Converson Plan)Conveyancers DirectoryPas encore d'évaluation

- Transpo Assigned CaseDocument8 pagesTranspo Assigned CaseAyban NabatarPas encore d'évaluation

- Commercial Lease Agreement for Stall No. 2Document4 pagesCommercial Lease Agreement for Stall No. 2Patrick BacongalloPas encore d'évaluation

- Seremba - Notice of Motion 2Document4 pagesSeremba - Notice of Motion 2Mugero Maybach DuncanPas encore d'évaluation

- Republic Act No 1224Document1 pageRepublic Act No 1224sigfridmontePas encore d'évaluation

- Ylarde vs. AquinoDocument1 pageYlarde vs. AquinoClark LimPas encore d'évaluation

- Kiini v. Victoria's Secret - Bikinis PDFDocument36 pagesKiini v. Victoria's Secret - Bikinis PDFMark JaffePas encore d'évaluation

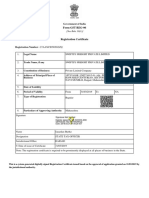

- Form GST REG-06: Government of IndiaDocument3 pagesForm GST REG-06: Government of Indiaswiftsy freight pvt ltdPas encore d'évaluation

- Succession Assignment 2Document3 pagesSuccession Assignment 2Natsu DragneelPas encore d'évaluation

- Association of Customs Brokers vs. Municipal Board of ManilaDocument5 pagesAssociation of Customs Brokers vs. Municipal Board of ManilaRaquel DoqueniaPas encore d'évaluation

- Rule 70Document71 pagesRule 70Red VelvetPas encore d'évaluation

- Board Minutes 30.01Document3 pagesBoard Minutes 30.01api-3835069Pas encore d'évaluation

- Insurance Code My ReviewDocument13 pagesInsurance Code My ReviewPursha Monte CaraPas encore d'évaluation

- Sample Pre Trial Brief AnnulmentDocument4 pagesSample Pre Trial Brief AnnulmentAnonymous VtsflLix1Pas encore d'évaluation

- Stronghold Insurance CompanyDocument2 pagesStronghold Insurance CompanyDiane UyPas encore d'évaluation

- Percentage BasicsDocument32 pagesPercentage BasicsAndreea Cristina100% (3)

- Section 58 in The Indian Partnership Act, 1932Document2 pagesSection 58 in The Indian Partnership Act, 1932shivashankari86Pas encore d'évaluation

- Samar Mining CoDocument3 pagesSamar Mining CoMJ FermaPas encore d'évaluation

- Delay in Filing WS After 90 Days Cannot Be Condoned Routinely - Only in Rare and Exceptional Cases 2009 SCDocument6 pagesDelay in Filing WS After 90 Days Cannot Be Condoned Routinely - Only in Rare and Exceptional Cases 2009 SCSridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್Pas encore d'évaluation

- Fundamental Clauses in Commercial ContractsDocument4 pagesFundamental Clauses in Commercial ContractsKim Ngân Nguyễn ThịPas encore d'évaluation

- Article On Ruling of Cal HC On Applicability of Stamp Duty On Mergers and AmalgamationDocument2 pagesArticle On Ruling of Cal HC On Applicability of Stamp Duty On Mergers and AmalgamationPayel JainPas encore d'évaluation

- Punjab Professions, Trades, Callings and Employments Taxation PDFDocument2 pagesPunjab Professions, Trades, Callings and Employments Taxation PDFLatest Laws TeamPas encore d'évaluation

- Sample Gold's Membership Form 2Document2 pagesSample Gold's Membership Form 2Smart Telecoms GoldsGymPas encore d'évaluation

- Sales Case Digest - Atty. CasinoDocument3 pagesSales Case Digest - Atty. CasinoJamaica Cabildo ManaligodPas encore d'évaluation

- Principles in Legal WritingDocument11 pagesPrinciples in Legal WritingAlbert BolantePas encore d'évaluation

- Hakkasan LV v. Hakim v. Hakkasan LVDocument172 pagesHakkasan LV v. Hakim v. Hakkasan LVJuancarlos Gómez-Montejano100% (1)

- Transfer of Ownership PackageDocument12 pagesTransfer of Ownership PackageMichael Schulte100% (4)

- Assured Return Agreement-3800 (4th Dec)Document10 pagesAssured Return Agreement-3800 (4th Dec)rohit_jnPas encore d'évaluation

- Sample Legal OpinionDocument2 pagesSample Legal Opinionjuleii0875% (4)