Vous aimerez peut-être aussi

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Deminimis BenefitsDocument24 pagesDeminimis Benefitsdaryl canoza100% (1)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Tax Deductions GuideDocument10 pagesTax Deductions GuideSjaneyPas encore d'évaluation

- EMI Calculator For Home LoanDocument5 pagesEMI Calculator For Home LoankeshavsainiPas encore d'évaluation

- CPA's Statement on the Itemized Assets and Estate Tax Due of the Decedent Romana Serafico OrtizDocument1 pageCPA's Statement on the Itemized Assets and Estate Tax Due of the Decedent Romana Serafico OrtizBaldovino Ventures100% (1)

- True or False 1Document13 pagesTrue or False 1Mary DenizePas encore d'évaluation

- Sale of Segregated Portion of LandDocument2 pagesSale of Segregated Portion of LandStephanie ViolaPas encore d'évaluation

- An Introduction To Oracle R12 E-Business TaxDocument46 pagesAn Introduction To Oracle R12 E-Business TaxDavid Sparks100% (5)

- Tax Review Class-Msu Case DigestDocument156 pagesTax Review Class-Msu Case DigestShiena Lou B. Amodia-RabacalPas encore d'évaluation

- Swedish Match Phil vs. Treasurer of City of Manila.Document2 pagesSwedish Match Phil vs. Treasurer of City of Manila.michelle m. templadoPas encore d'évaluation

- FABM2 Q2 MOD3 Income and Business Taxation 1Document27 pagesFABM2 Q2 MOD3 Income and Business Taxation 1Minimi Lovely33% (3)

- PennDocument1 pagePennBecca Oken-TatumPas encore d'évaluation

- ILottery Petition For ReviewDocument34 pagesILottery Petition For ReviewBecca Oken-TatumPas encore d'évaluation

- Request For Qualified Submissions, Front Street, SteeltonDocument7 pagesRequest For Qualified Submissions, Front Street, SteeltonBecca Oken-TatumPas encore d'évaluation

- Utility Rate Changes Effect 7-1-18Document1 pageUtility Rate Changes Effect 7-1-18Becca Oken-TatumPas encore d'évaluation

- Harrisburg Recovery Coordinator REVISED Exit PlanDocument92 pagesHarrisburg Recovery Coordinator REVISED Exit PlanPennLivePas encore d'évaluation

- Impact Insufficient Retirement SavingsDocument91 pagesImpact Insufficient Retirement SavingsBecca Oken-TatumPas encore d'évaluation

- RFQS Development of Hummelstown Municipal ComplexDocument7 pagesRFQS Development of Hummelstown Municipal ComplexBecca Oken-TatumPas encore d'évaluation

- Keystone Biofuels Indictment, January 2018Document23 pagesKeystone Biofuels Indictment, January 2018Becca Oken-TatumPas encore d'évaluation

- Request For Proposals - Brewpub Restaurant Dated Dec 28 2017 - Due Feb 5 2018Document5 pagesRequest For Proposals - Brewpub Restaurant Dated Dec 28 2017 - Due Feb 5 2018Becca Oken-TatumPas encore d'évaluation

- RFP Health Sciences Project - HU - Nov. 16 2017Document30 pagesRFP Health Sciences Project - HU - Nov. 16 2017Becca Oken-TatumPas encore d'évaluation

- Arun Kumar Salary 2019-10Document1 pageArun Kumar Salary 2019-10Rizwan AhmadPas encore d'évaluation

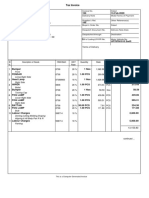

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Mehul RathorePas encore d'évaluation

- 稅務局 Inland Revenue Department: Business Registration Fee and Levy TableDocument1 page稅務局 Inland Revenue Department: Business Registration Fee and Levy Table彭黑郎Pas encore d'évaluation

- Name of Business Projected Income Statement For The Years Ended December 31,2017-2021Document10 pagesName of Business Projected Income Statement For The Years Ended December 31,2017-2021Aries Gonzales CaraganPas encore d'évaluation

- Tax Invoice Parts RepairDocument2 pagesTax Invoice Parts RepairJayant OjhaPas encore d'évaluation

- Taxation Question BankDocument3 pagesTaxation Question BankRishikesh BhujbalPas encore d'évaluation

- InvoiceDocument2 pagesInvoiceRK userPas encore d'évaluation

- 10 Activity 1 MRLFJRDDocument1 page10 Activity 1 MRLFJRDMurielle FajardoPas encore d'évaluation

- 1 Basic SardaDocument12 pages1 Basic Sardaniko.tpPas encore d'évaluation

- CV Raun Sintiya Daftar Akun Periode 31 Desember 2021Document4 pagesCV Raun Sintiya Daftar Akun Periode 31 Desember 2021BeertyavrillianPas encore d'évaluation

- Employee Declaration Form FY 2020-21Document2 pagesEmployee Declaration Form FY 2020-21Harsha I100% (2)

- Radzi & Co Profile - June 2017Document11 pagesRadzi & Co Profile - June 2017MohdRsysPas encore d'évaluation

- GSTDocument4 pagesGSTThendralzeditzPas encore d'évaluation

- 74824bos60500 cp15Document90 pages74824bos60500 cp15soni12c2004Pas encore d'évaluation

- LSPU Provides Quality Education Through Responsive InstructionDocument4 pagesLSPU Provides Quality Education Through Responsive InstructionJhervhee A. ArapanPas encore d'évaluation

- Special Topics & Updates TaxationDocument7 pagesSpecial Topics & Updates TaxationMhadzBornalesMpPas encore d'évaluation

- Winebrenner-Inigo-Insurance-Brokers-Inc-v-CIRDocument24 pagesWinebrenner-Inigo-Insurance-Brokers-Inc-v-CIRDarrel John SombilonPas encore d'évaluation

- Settlement Commissionb Tax FDDocument15 pagesSettlement Commissionb Tax FDhani diptiPas encore d'évaluation

- Capital Gains and Losses: Schedule D (Form 1120)Document1 pageCapital Gains and Losses: Schedule D (Form 1120)IRSPas encore d'évaluation

- Tax Invoice BillDocument1 pageTax Invoice BillAbhay Pratap SinghPas encore d'évaluation