Vous aimerez peut-être aussi

- AFAR Assessment 2Document5 pagesAFAR Assessment 2JoshelBuenaventuraPas encore d'évaluation

- Cvp-Analysis AbsvarcostingDocument13 pagesCvp-Analysis AbsvarcostingGwy PagdilaoPas encore d'évaluation

- 1.20PP Partnership Formation and DissolutionDocument16 pages1.20PP Partnership Formation and DissolutionMarcley BataoilPas encore d'évaluation

- Bustamante TAX CDocument19 pagesBustamante TAX CJean Rose Tabagay BustamantePas encore d'évaluation

- Finals Exercise 2 - WC Management InventoryDocument3 pagesFinals Exercise 2 - WC Management Inventorywin win0% (1)

- MAS Monitoring ExamDocument12 pagesMAS Monitoring ExamPrincess Claris Araucto0% (1)

- Chapter 9Document13 pagesChapter 9ppantin0430Pas encore d'évaluation

- AFAR - Corporate LiquidationDocument1 pageAFAR - Corporate LiquidationKent Raysil PamaongPas encore d'évaluation

- Reviewer Incremental Analysis 1Document5 pagesReviewer Incremental Analysis 1Shaira Rehj RiveraPas encore d'évaluation

- Dayag - Chapter 5 PDFDocument25 pagesDayag - Chapter 5 PDFKen ZafraPas encore d'évaluation

- Quizzer-Cost-Behavior - Docx Regression Analysis Least SquaresDocument1 pageQuizzer-Cost-Behavior - Docx Regression Analysis Least SquareslastjohnPas encore d'évaluation

- Quiz 5 Problems Second Semester AY2223 With AnswersDocument4 pagesQuiz 5 Problems Second Semester AY2223 With AnswersManzano, Carl Clinton Neil D.Pas encore d'évaluation

- Relevant Costing Simulated Exam Ans KeyDocument5 pagesRelevant Costing Simulated Exam Ans KeySarah BalisacanPas encore d'évaluation

- AFAR-07 (Home-Office & Branch Accounting)Document7 pagesAFAR-07 (Home-Office & Branch Accounting)mysweet surrenderPas encore d'évaluation

- Financial Accounting: Share-Based Compensation Share-Based Compensation Book Value Per ShareDocument11 pagesFinancial Accounting: Share-Based Compensation Share-Based Compensation Book Value Per ShareairaPas encore d'évaluation

- By Via Samantha de Austria: (Down Payment) (Face Value of Note) (Substantially Performed) (No Substantial Performance)Document6 pagesBy Via Samantha de Austria: (Down Payment) (Face Value of Note) (Substantially Performed) (No Substantial Performance)Via Samantha de AustriaPas encore d'évaluation

- Partnership Operations: Problem CDocument3 pagesPartnership Operations: Problem CJoeneil DamalerioPas encore d'évaluation

- Fischer - Pship LiquiDocument7 pagesFischer - Pship LiquiShawn Michael DoluntapPas encore d'évaluation

- MAS - 1416 Profit Planning - CVP AnalysisDocument24 pagesMAS - 1416 Profit Planning - CVP AnalysisAzureBlazePas encore d'évaluation

- Chapter 8 Consideration of Internal Control in An InformatiDocument32 pagesChapter 8 Consideration of Internal Control in An Informatichristiansmilaw100% (1)

- Incometaxation1 PDFDocument543 pagesIncometaxation1 PDFmae annPas encore d'évaluation

- Partnership ReviewDocument5 pagesPartnership ReviewAirille CarlosPas encore d'évaluation

- Cma/Cfm: Preparatory ProgramDocument42 pagesCma/Cfm: Preparatory Programpaperdollsx0% (2)

- Afar SolutionsDocument8 pagesAfar Solutionspopsie tulalianPas encore d'évaluation

- CTT Review October 2022 - Week 1 To Week 3Document334 pagesCTT Review October 2022 - Week 1 To Week 3Rose Anne ChewPas encore d'évaluation

- Calypso Canvas Makes Canvas Window Awnings You Have Been AskedDocument1 pageCalypso Canvas Makes Canvas Window Awnings You Have Been AskedAmit PandeyPas encore d'évaluation

- Acct 3Document25 pagesAcct 3Diego Salazar100% (1)

- Prelim Exam PDFDocument6 pagesPrelim Exam PDFPaw VerdilloPas encore d'évaluation

- Bus Combination 2Document8 pagesBus Combination 2Angelica AllanicPas encore d'évaluation

- LTCC Exam PDF FreeDocument5 pagesLTCC Exam PDF FreeMichael Brian TorresPas encore d'évaluation

- General de Jesus CollegeDocument12 pagesGeneral de Jesus CollegeErwin Labayog MedinaPas encore d'évaluation

- Book 9Document2 pagesBook 9Actg SolmanPas encore d'évaluation

- Chapter 4 GEDocument12 pagesChapter 4 GEYenny Torro100% (1)

- Exam in Taxation Exam in Taxation: Business Tax (Naga College Foundation) Business Tax (Naga College Foundation)Document29 pagesExam in Taxation Exam in Taxation: Business Tax (Naga College Foundation) Business Tax (Naga College Foundation)jhean dabatosPas encore d'évaluation

- Auditing Theory Finals PDF FreeDocument11 pagesAuditing Theory Finals PDF FreeMichael Brian TorresPas encore d'évaluation

- N. Cruz-Course Material For Strategic Cost ManagementDocument134 pagesN. Cruz-Course Material For Strategic Cost ManagementEmmanuel VillafuertePas encore d'évaluation

- LTCC 1Document3 pagesLTCC 1Jamie RamosPas encore d'évaluation

- What Is AccountingDocument76 pagesWhat Is AccountingMa Jemaris Solis0% (1)

- Cpa Review School of The Philippines Mani LaDocument2 pagesCpa Review School of The Philippines Mani LaAljur SalamedaPas encore d'évaluation

- Mock 2nd Eval - TOADocument7 pagesMock 2nd Eval - TOAPatrick Powell100% (1)

- Audit of PPE Comprehensive QuizzerDocument9 pagesAudit of PPE Comprehensive QuizzerAlice WuPas encore d'évaluation

- App 1 ModuleDocument15 pagesApp 1 ModuleJaemine GuecoPas encore d'évaluation

- Studet Practical Accounting Ch17 PPE AcquisitionDocument16 pagesStudet Practical Accounting Ch17 PPE Acquisitionsabina del montePas encore d'évaluation

- Quiz Results: Week 12: Standard Costing and Variance AnalysisDocument25 pagesQuiz Results: Week 12: Standard Costing and Variance Analysismarie anicetePas encore d'évaluation

- CE On Quasi-ReorganizationDocument1 pageCE On Quasi-ReorganizationalyssaPas encore d'évaluation

- PFRS 15, Franchise Accounting, and Consignment SalesDocument7 pagesPFRS 15, Franchise Accounting, and Consignment SalesPaupauPas encore d'évaluation

- Equity Test BanksDocument34 pagesEquity Test BanksHea Jennifer AyopPas encore d'évaluation

- Module 8 AgricultureDocument9 pagesModule 8 AgricultureTrine De LeonPas encore d'évaluation

- 68125672575bdf96fc857f403531f1c9-copyDocument9 pages68125672575bdf96fc857f403531f1c9-copyyour unreal0% (1)

- TAX Final-PB FEUDocument9 pagesTAX Final-PB FEUkarim abitagoPas encore d'évaluation

- Income & Business Taxation QB3Document8 pagesIncome & Business Taxation QB3Keahlyn Boticario0% (1)

- Accounting Gov ReviewerDocument20 pagesAccounting Gov ReviewerShane TorriePas encore d'évaluation

- TH Quiz No.1: Income Taxation (TAX 101)Document4 pagesTH Quiz No.1: Income Taxation (TAX 101)Maricel MielPas encore d'évaluation

- Assignment No. 2 Business Combination Stock Acquisition Part 1.2Document4 pagesAssignment No. 2 Business Combination Stock Acquisition Part 1.2Aivan De LeonPas encore d'évaluation

- Foreign Currency Transactions2019Document6 pagesForeign Currency Transactions2019Jeann MuycoPas encore d'évaluation

- PartnershipDocument43 pagesPartnershipIvhy Cruz EstrellaPas encore d'évaluation

- Polytechnic University of The Philippines College of AccountancyDocument11 pagesPolytechnic University of The Philippines College of AccountancyRonel CacheroPas encore d'évaluation

- At PDF FreeDocument15 pagesAt PDF FreemaekaellaPas encore d'évaluation

- Responsibility Accounting and Profitability RatiosDocument13 pagesResponsibility Accounting and Profitability RatiosKhrystal AbrioPas encore d'évaluation

- HO6 - Responsibility Accounting and Transfer Pricing PDFDocument9 pagesHO6 - Responsibility Accounting and Transfer Pricing PDFPATRICIA PEREZPas encore d'évaluation

- GlobalprotectDocument6 pagesGlobalprotectRambell John RodriguezPas encore d'évaluation

- Deep Sea Adventure RulesDocument1 pageDeep Sea Adventure RulesDalionzoPas encore d'évaluation

- Bang RulesDocument12 pagesBang Rulesmar1ne100% (1)

- Color PDFDocument13 pagesColor PDFRambell John RodriguezPas encore d'évaluation

- Template 2018 (2) 2724698897725593047Document2 pagesTemplate 2018 (2) 2724698897725593047Rambell John RodriguezPas encore d'évaluation

- Rambell Rodriguez PDS (Nov)Document4 pagesRambell Rodriguez PDS (Nov)Rambell John RodriguezPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2020 Cinemalaya Philippine Independent Film FestivalDocument2 pages2020 Cinemalaya Philippine Independent Film FestivalCyrus PanganibanPas encore d'évaluation

- Job Posting: Position BC/Department Group QualificationsDocument20 pagesJob Posting: Position BC/Department Group QualificationsFrancia Mae BuenoPas encore d'évaluation

- C 3746 B 9 ADocument15 pagesC 3746 B 9 AJoan RosalesPas encore d'évaluation

- Straight To The Point Emil Vohlert PDFDocument34 pagesStraight To The Point Emil Vohlert PDFSA023Pas encore d'évaluation

- 1987 Philippine Constitution (With Highlights) PDFDocument41 pages1987 Philippine Constitution (With Highlights) PDFRambell John RodriguezPas encore d'évaluation

- Unstable Unicorns RuledlkfkfDocument4 pagesUnstable Unicorns RuledlkfkfRambell John RodriguezPas encore d'évaluation

- 18 Filing Rules For Proper Alphabetizing: Rule 1Document6 pages18 Filing Rules For Proper Alphabetizing: Rule 1Faraz NassajianPas encore d'évaluation

- Rodriguez, Rambell John A.: 909 Hilerang Kawayan ST., Lawa, Obando, Bulacan 3021Document3 pagesRodriguez, Rambell John A.: 909 Hilerang Kawayan ST., Lawa, Obando, Bulacan 3021Rambell John RodriguezPas encore d'évaluation

- Civil Service Exam Complete Reviewer Philippines 2017Document46 pagesCivil Service Exam Complete Reviewer Philippines 2017JJ Torres84% (434)

- 18 Filing Rules For Proper Alphabetizing: Rule 1Document6 pages18 Filing Rules For Proper Alphabetizing: Rule 1Faraz NassajianPas encore d'évaluation

- PremiumContributionTable PDFDocument1 pagePremiumContributionTable PDFRambell John RodriguezPas encore d'évaluation

- Rodriguez, Rambell John A.: 909 Hilerang Kawayan ST., Lawa, Obando, Bulacan 3021Document3 pagesRodriguez, Rambell John A.: 909 Hilerang Kawayan ST., Lawa, Obando, Bulacan 3021Rambell John RodriguezPas encore d'évaluation

- POM Chapter 5 PDFDocument46 pagesPOM Chapter 5 PDFRambell John RodriguezPas encore d'évaluation

- Rodriguez, Rambell John A.: 909 Hilerang Kawayan ST., Lawa, Obando, Bulacan 3021Document3 pagesRodriguez, Rambell John A.: 909 Hilerang Kawayan ST., Lawa, Obando, Bulacan 3021Rambell John RodriguezPas encore d'évaluation

- ArianneDocument2 pagesArianneRambell John RodriguezPas encore d'évaluation

- CBRC WaiverDocument2 pagesCBRC WaiverRambell John RodriguezPas encore d'évaluation

- Syllabus: MK 300: Principles of MarketingDocument6 pagesSyllabus: MK 300: Principles of MarketingRambell John RodriguezPas encore d'évaluation

- Book ReferencesDocument5 pagesBook ReferencesRambell John RodriguezPas encore d'évaluation

- Good Gov and Soc. ResDocument4 pagesGood Gov and Soc. ResRambell John RodriguezPas encore d'évaluation

- College of Accountancy and Business Administration College of Accountancy and Business AdministrationDocument1 pageCollege of Accountancy and Business Administration College of Accountancy and Business AdministrationRambell John RodriguezPas encore d'évaluation

- Festival 2018: Sta Maria ChoralDocument1 pageFestival 2018: Sta Maria ChoralRambell John RodriguezPas encore d'évaluation

- Philippine Administrative System (PAS) - ORIGINALDocument31 pagesPhilippine Administrative System (PAS) - ORIGINALAPIDSRU Surveillance100% (4)

- JTN FY16 Guidelines - FINALDocument9 pagesJTN FY16 Guidelines - FINALYaacov MaymanPas encore d'évaluation

- Basic Training Manual Updated 09-05-14Document68 pagesBasic Training Manual Updated 09-05-14PamelaJacksonPas encore d'évaluation

- 1 - NOPSSCEA Operations ManualDocument33 pages1 - NOPSSCEA Operations ManualJohna Mae Dolar Etang50% (2)

- SAP Funds Management Configuration-FMDocument59 pagesSAP Funds Management Configuration-FMLiordi74% (27)

- Boston Creamery, IncDocument10 pagesBoston Creamery, IncAto SumartoPas encore d'évaluation

- Alsip April 19 2010 BoardDocument6 pagesAlsip April 19 2010 BoardMy Pile of Strange 2013 Election CollectionPas encore d'évaluation

- Fresh Pick Wet Market Enterprise Business Plan PDFDocument105 pagesFresh Pick Wet Market Enterprise Business Plan PDFshafiq100% (5)

- A3 BSBFIM501 Manage Budgets and Financial PlansDocument5 pagesA3 BSBFIM501 Manage Budgets and Financial PlansMaya Roton0% (1)

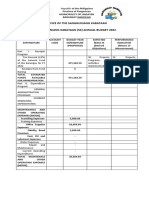

- Office of The Sangguniang Kabataan Sangguniang Kabataan (SK) Annual Budget 2022Document11 pagesOffice of The Sangguniang Kabataan Sangguniang Kabataan (SK) Annual Budget 2022John Reybren Malogan100% (1)

- Chapter 09 Testbank Solution Manual Management AccountingDocument47 pagesChapter 09 Testbank Solution Manual Management AccountingTrinh LêPas encore d'évaluation

- Key Findings in The Forensic Investigation of The Public DebtDocument21 pagesKey Findings in The Forensic Investigation of The Public DebtRob G.Pas encore d'évaluation

- Controlling-2012 20130211075746.531 XDocument217 pagesControlling-2012 20130211075746.531 XSatyadev PulipakaPas encore d'évaluation

- Sample Fresher MBA ResumeDocument6 pagesSample Fresher MBA ResumeAshish ChauhanPas encore d'évaluation

- Reston Association: Review of The Tetra/Lake House Project, StoneTurn Group, February 28, 2017Document31 pagesReston Association: Review of The Tetra/Lake House Project, StoneTurn Group, February 28, 2017Terry MaynardPas encore d'évaluation

- 8508Document9 pages8508ZunairaAslamPas encore d'évaluation

- Tutorial Budget StudentDocument4 pagesTutorial Budget StudentDanial NorazmanPas encore d'évaluation

- Financial Management Operations Manual (Fmom)Document29 pagesFinancial Management Operations Manual (Fmom)Tawagin Mo Akong MertsPas encore d'évaluation

- Budgetary ControlDocument29 pagesBudgetary ControlJagadeesh MohanPas encore d'évaluation

- International Organisations QuestionsDocument22 pagesInternational Organisations QuestionsparapiripoPas encore d'évaluation

- Personal Financial Planning 14th Edition Billingsley Test BankDocument56 pagesPersonal Financial Planning 14th Edition Billingsley Test BankBen Williams100% (37)

- Treasury Regulations: For Departments, Constitutional Institutions and Public EntitiesDocument75 pagesTreasury Regulations: For Departments, Constitutional Institutions and Public EntitiesHoward CohenPas encore d'évaluation

- Financial Management in The Sport Industry 2nd Brown Solution Manual DownloadDocument12 pagesFinancial Management in The Sport Industry 2nd Brown Solution Manual DownloadElizabethLewisixmt100% (41)

- Top 20 Financial KPIs Every CFO Dashboard Should HaveDocument5 pagesTop 20 Financial KPIs Every CFO Dashboard Should HavekPrasad80% (1)

- Request For Proposals: 2017 Lodging Tax FundDocument16 pagesRequest For Proposals: 2017 Lodging Tax FundPratitiPas encore d'évaluation

- Cma QuizDocument2 pagesCma QuizKurt SoriaoPas encore d'évaluation

- PSG Ex - 8.2PSG Ex - 8.2 - Monthly Report Template - Monthly Report TemplateDocument25 pagesPSG Ex - 8.2PSG Ex - 8.2 - Monthly Report Template - Monthly Report TemplateJohn WilliamsPas encore d'évaluation

- Case Studies Internal ControlDocument3 pagesCase Studies Internal Controlakq153Pas encore d'évaluation

- Accounting For Decision Making Notes Lecture Notes Lectures 1 13Document11 pagesAccounting For Decision Making Notes Lecture Notes Lectures 1 13HiếuPas encore d'évaluation

- Planning Tools and Techniques: With Duane WeaverDocument24 pagesPlanning Tools and Techniques: With Duane WeaverAbdirahmanPas encore d'évaluation

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeD'EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeÉvaluation : 4.5 sur 5 étoiles4.5/5 (88)

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverD'EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverÉvaluation : 4.5 sur 5 étoiles4.5/5 (186)

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoD'Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoÉvaluation : 5 sur 5 étoiles5/5 (23)

- $100M Leads: How to Get Strangers to Want to Buy Your StuffD'Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffÉvaluation : 5 sur 5 étoiles5/5 (18)

- Summary of Noah Kagan's Million Dollar WeekendD'EverandSummary of Noah Kagan's Million Dollar WeekendÉvaluation : 5 sur 5 étoiles5/5 (1)

- 12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurD'Everand12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurÉvaluation : 4 sur 5 étoiles4/5 (2)

- Broken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterD'EverandBroken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterÉvaluation : 5 sur 5 étoiles5/5 (3)

- Fascinate: How to Make Your Brand Impossible to ResistD'EverandFascinate: How to Make Your Brand Impossible to ResistÉvaluation : 5 sur 5 étoiles5/5 (1)

- Speaking Effective English!: Your Guide to Acquiring New Confidence In Personal and Professional CommunicationD'EverandSpeaking Effective English!: Your Guide to Acquiring New Confidence In Personal and Professional CommunicationÉvaluation : 4.5 sur 5 étoiles4.5/5 (74)

- The First Minute: How to start conversations that get resultsD'EverandThe First Minute: How to start conversations that get resultsÉvaluation : 4.5 sur 5 étoiles4.5/5 (57)