Vous aimerez peut-être aussi

- Islamic Banking And Finance for Beginners!D'EverandIslamic Banking And Finance for Beginners!Évaluation : 2 sur 5 étoiles2/5 (1)

- Banking India: Accepting Deposits for the Purpose of LendingD'EverandBanking India: Accepting Deposits for the Purpose of LendingPas encore d'évaluation

- 180 Sample-Chapter PDFDocument15 pages180 Sample-Chapter PDFhanumanthaiahgowdaPas encore d'évaluation

- Chinu KumariDocument46 pagesChinu KumariVikas ShahPas encore d'évaluation

- Introduction To BankingDocument59 pagesIntroduction To Bankingshahyashr100% (1)

- Financial Performance of BankDocument14 pagesFinancial Performance of BankManjunath ShettyPas encore d'évaluation

- Deepak 1Document65 pagesDeepak 1PRO FilmmakerPas encore d'évaluation

- Bank of IndiaDocument22 pagesBank of IndiaLeeladhar Nagar100% (1)

- BankingDocument15 pagesBankingNEERAJA UNNIPas encore d'évaluation

- Bank - Commercial BankDocument12 pagesBank - Commercial BankShalini Singh IPSAPas encore d'évaluation

- Functions of Commercial Banks: Primary and Secondary FunctionsDocument3 pagesFunctions of Commercial Banks: Primary and Secondary FunctionsPavan Kumar SuralaPas encore d'évaluation

- 7 P's of Private Sector BankDocument21 pages7 P's of Private Sector BankMinal DalviPas encore d'évaluation

- Ifs Cia 3Document11 pagesIfs Cia 3Rohit GoyalPas encore d'évaluation

- COMMERCIALDocument15 pagesCOMMERCIALBadbitchPas encore d'évaluation

- BANKING AWAREESS: Different Types of Bank: 1. Commercial BanksDocument12 pagesBANKING AWAREESS: Different Types of Bank: 1. Commercial BanksKumar KushPas encore d'évaluation

- Banking Law Previous SemesterDocument10 pagesBanking Law Previous Semesteralpesh upadhyayPas encore d'évaluation

- Summer Training Report FOR Union Bank of IndiaDocument29 pagesSummer Training Report FOR Union Bank of IndiaRavina MehtaPas encore d'évaluation

- Nikil Kapoor 1 - For MergeDocument76 pagesNikil Kapoor 1 - For MergeNikhil KapoorPas encore d'évaluation

- Q1 Banking 1Document18 pagesQ1 Banking 1Adarsh ShetPas encore d'évaluation

- Commercial Banking & Customer - Banker Relationship - Unit IiDocument13 pagesCommercial Banking & Customer - Banker Relationship - Unit IiGame ProfilePas encore d'évaluation

- A Study On Financial Analysis of Punjab National BankDocument11 pagesA Study On Financial Analysis of Punjab National BankJitesh LadgePas encore d'évaluation

- Centurion University of Technology and Management: Project Report OnDocument23 pagesCenturion University of Technology and Management: Project Report OnKING ZIPas encore d'évaluation

- Economics FinalDocument36 pagesEconomics FinalPratham PrahaladkaPas encore d'évaluation

- Merchant Banking and Financial ServicesDocument41 pagesMerchant Banking and Financial ServicesknpunithrajPas encore d'évaluation

- Fim Module 5Document29 pagesFim Module 5Hasnoor's CreationsPas encore d'évaluation

- Sem V2019 PatternDocument41 pagesSem V2019 PatternAayushi ViraniPas encore d'évaluation

- Banking N FinanceDocument27 pagesBanking N FinancetechworkpressPas encore d'évaluation

- SAJAHAN Full ProjectDocument45 pagesSAJAHAN Full Projecttn63 villanPas encore d'évaluation

- By-Harihar - J, Utkarsha. S,: Aaditya. R Ashish.BDocument30 pagesBy-Harihar - J, Utkarsha. S,: Aaditya. R Ashish.BAshish BaswantePas encore d'évaluation

- Icici Bank Project-Black BookDocument55 pagesIcici Bank Project-Black BookMaria Nunes56% (9)

- Fundamental of BankingDocument55 pagesFundamental of BankingSubodh RoyPas encore d'évaluation

- Banking Structure in India Banking:: 1.central Bank 3.specialized Bank 4.cooperative BankDocument5 pagesBanking Structure in India Banking:: 1.central Bank 3.specialized Bank 4.cooperative BankKandaroliPas encore d'évaluation

- Banking ServicesDocument26 pagesBanking ServicesHarin Lydia100% (1)

- Pt. D.D.U.M.C: Customer Preference Towards Private Sector Banks and Public Sector BanksDocument105 pagesPt. D.D.U.M.C: Customer Preference Towards Private Sector Banks and Public Sector BankssknagarPas encore d'évaluation

- State BanksDocument6 pagesState BanksVikram LodhaPas encore d'évaluation

- Home Loans: Submission To Guru Jambheshwar UniversityDocument11 pagesHome Loans: Submission To Guru Jambheshwar Universitysamy7541Pas encore d'évaluation

- Structure of Banking System in IndiaDocument34 pagesStructure of Banking System in IndiaAyushi SinghPas encore d'évaluation

- Private Sector Banks: Icici BankDocument13 pagesPrivate Sector Banks: Icici BankAshishVarghesePas encore d'évaluation

- Retail Banking Project BOIDocument107 pagesRetail Banking Project BOIPooja Mathur100% (1)

- What Is Bank?: Indian Banking SystemDocument67 pagesWhat Is Bank?: Indian Banking SystemamitPas encore d'évaluation

- 2nd ChapterDocument30 pages2nd ChapterAnantha KrishnaPas encore d'évaluation

- Meaning of Banking: 1. Central BanksDocument6 pagesMeaning of Banking: 1. Central BanksMuskanPas encore d'évaluation

- Indian Banking SystemDocument67 pagesIndian Banking SystemTejas MakwanaPas encore d'évaluation

- Chapter 1 Introduction: Prahladrai Dalmia Lions College of Commerce & EconomicsDocument69 pagesChapter 1 Introduction: Prahladrai Dalmia Lions College of Commerce & EconomicsTYBBI 3007 DHIVAR ANKITAPas encore d'évaluation

- Commercial Banking in IndiaDocument3 pagesCommercial Banking in IndiaPallavi PatelPas encore d'évaluation

- Document 1Document67 pagesDocument 1editorialfreelancers19Pas encore d'évaluation

- Functions of Commercial Banks of IndiaDocument5 pagesFunctions of Commercial Banks of Indiajunaid sayyedPas encore d'évaluation

- Union Bank of IndiaDocument58 pagesUnion Bank of Indiadivyesh_variaPas encore d'évaluation

- ACAD EDGE Edition 7 (Banking)Document29 pagesACAD EDGE Edition 7 (Banking)Damanjot SinghPas encore d'évaluation

- Final Study of Internet Banking in IndiaDocument44 pagesFinal Study of Internet Banking in IndiaHemlatas RangoliPas encore d'évaluation

- Black Book (Sarika)Document56 pagesBlack Book (Sarika)Smruti VasavadaPas encore d'évaluation

- e BankingDocument61 pagese BankingRiSHI KeSH GawaIPas encore d'évaluation

- "Credit Risk Management in State Bank of India": Title of The ProjectDocument43 pages"Credit Risk Management in State Bank of India": Title of The Projectswarali deshmukhPas encore d'évaluation

- Icici Fyfm Efs ProjectDocument9 pagesIcici Fyfm Efs ProjectMihir DeliwalaPas encore d'évaluation

- Final ProjectDocument73 pagesFinal ProjectShilpa NikamPas encore d'évaluation

- A Study On Financial Services of Commercial Bank With Reference To ICICI Bank (Final)Document56 pagesA Study On Financial Services of Commercial Bank With Reference To ICICI Bank (Final)geetha_kannan32Pas encore d'évaluation

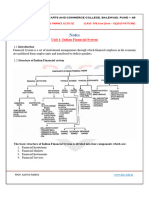

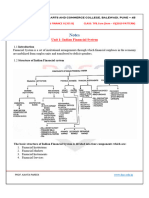

- Fin Mkts Unit II Lec NotesDocument6 pagesFin Mkts Unit II Lec Notesprakash.pPas encore d'évaluation

- Banking Sector: Madhurima Mitra 11712303911Document43 pagesBanking Sector: Madhurima Mitra 11712303911mollymitraPas encore d'évaluation

- Banking OmbudsmanDocument73 pagesBanking OmbudsmanmoregauravPas encore d'évaluation

- TN Shops Establishments Act AmendmentDocument3 pagesTN Shops Establishments Act Amendmentakshay khartePas encore d'évaluation

- Death in The Workplace PDFDocument5 pagesDeath in The Workplace PDFakshay khartePas encore d'évaluation

- Death in The Workplace PDFDocument5 pagesDeath in The Workplace PDFakshay khartePas encore d'évaluation

- Corporate Crime and The Criminal Liability of Corporate EntitiesDocument10 pagesCorporate Crime and The Criminal Liability of Corporate Entitiesakshay khartePas encore d'évaluation

- The Turn To Corporate Criminal Liability For International CrimesDocument79 pagesThe Turn To Corporate Criminal Liability For International Crimesakshay khartePas encore d'évaluation

- CompendiumDocument33 pagesCompendiumakshay khartePas encore d'évaluation

- Criminal Liability of Corporation An Ind PDFDocument17 pagesCriminal Liability of Corporation An Ind PDFakshay khartePas encore d'évaluation

- Corporate Crime and Sentencing in India: Required Amendments in LawDocument17 pagesCorporate Crime and Sentencing in India: Required Amendments in Lawakshay khartePas encore d'évaluation

- T N N S: Amil ADU Ational Law ChoolDocument17 pagesT N N S: Amil ADU Ational Law Choolakshay khartePas encore d'évaluation

- Underwriting of Securities in India: Submission in The Subject of Corporate Finance LawDocument22 pagesUnderwriting of Securities in India: Submission in The Subject of Corporate Finance Lawakshay khartePas encore d'évaluation

- New Doc 2018-10-31 14.16.52 - 1Document1 pageNew Doc 2018-10-31 14.16.52 - 1akshay khartePas encore d'évaluation

- Tax Literacy and Its Impact On The Individual Taxpayers With Reference To Indian Tax PayersDocument9 pagesTax Literacy and Its Impact On The Individual Taxpayers With Reference To Indian Tax Payersakshay khartePas encore d'évaluation

- First Draft EDITEDDocument10 pagesFirst Draft EDITEDakshay khartePas encore d'évaluation

- Copyleft, Creative Commons and The Need For Change: The Tamilnadu National Law School, TrichirapalliDocument18 pagesCopyleft, Creative Commons and The Need For Change: The Tamilnadu National Law School, Trichirapalliakshay khartePas encore d'évaluation

- Measures of Central TendencyDocument36 pagesMeasures of Central Tendencyakshay kharte100% (3)

- Revised Ciruclar (Prospective V Year)Document1 pageRevised Ciruclar (Prospective V Year)akshay khartePas encore d'évaluation

- Marriage Under Private International LawDocument13 pagesMarriage Under Private International Lawakshay khartePas encore d'évaluation

- Restitution of Conjugal Rights Faimly Law 1Document17 pagesRestitution of Conjugal Rights Faimly Law 1akshay kharte100% (1)

- Tamil Nadu National Law School: Rights and Liberty of Animals and Birds SubmittedDocument9 pagesTamil Nadu National Law School: Rights and Liberty of Animals and Birds Submittedakshay khartePas encore d'évaluation

- Marriage Under Private International LawDocument32 pagesMarriage Under Private International LawAmudha Mony64% (22)

- Virginia Law Review Is Collaborating With JSTOR To DigitizeDocument12 pagesVirginia Law Review Is Collaborating With JSTOR To Digitizeakshay khartePas encore d'évaluation

- Sutherland TheoryDocument27 pagesSutherland TheoryPraveen VijayPas encore d'évaluation

- Right To Be Forgotten - ECJ Ruling.Document3 pagesRight To Be Forgotten - ECJ Ruling.Charters and CaldecottPas encore d'évaluation

- Schools of CriminologyDocument70 pagesSchools of CriminologyPraveen Vijay100% (1)

- Human Rights CyberspaceDocument40 pagesHuman Rights Cyberspaceakshay khartePas encore d'évaluation

- Human Rights CyberspaceDocument40 pagesHuman Rights Cyberspaceakshay khartePas encore d'évaluation

- ACFrOgDt2vplQz8XM1H5qY qnmW0SnyPn09RZlxu-8 B55pRrm7Gk6uB2VfCPjL-QiKJXYCMlxusvqQmK67ov3tGvihIk0Bj3tYhUfBi77xScKpGtcntksH9nUT8K YDocument5 pagesACFrOgDt2vplQz8XM1H5qY qnmW0SnyPn09RZlxu-8 B55pRrm7Gk6uB2VfCPjL-QiKJXYCMlxusvqQmK67ov3tGvihIk0Bj3tYhUfBi77xScKpGtcntksH9nUT8K YPraveen VijayPas encore d'évaluation

- ACFrOgDQ9P5zFMlerB4559s6WpK3CCqiRuVMZOGsfetcQA dehqiTcK 5F7dQ1 - aPyGQGS86FdOIIR246XGy9gxF6PNUbyPG - FqXGic 04M1hkEhG 8lVsCHJ4R4G - GDocument7 pagesACFrOgDQ9P5zFMlerB4559s6WpK3CCqiRuVMZOGsfetcQA dehqiTcK 5F7dQ1 - aPyGQGS86FdOIIR246XGy9gxF6PNUbyPG - FqXGic 04M1hkEhG 8lVsCHJ4R4G - Gakshay khartePas encore d'évaluation

- Mid-Semester Examinations (Even-Semester), April 2018Document2 pagesMid-Semester Examinations (Even-Semester), April 2018akshay khartePas encore d'évaluation

- First Draft EDITEDDocument10 pagesFirst Draft EDITEDakshay khartePas encore d'évaluation

- IPS AIO - DSI - MWPA - 100Rs Per Day - 15LCIDocument2 pagesIPS AIO - DSI - MWPA - 100Rs Per Day - 15LCIvikas pallaPas encore d'évaluation

- Cash Journal: Month - Agency - Fund - Sheet No.Document4 pagesCash Journal: Month - Agency - Fund - Sheet No.Ivy Michelle HabagatPas encore d'évaluation

- UntitledDocument3 pagesUntitledrasool mehrjooPas encore d'évaluation

- Genmath 11 Humss San Gulliermo de AquitaniaDocument3 pagesGenmath 11 Humss San Gulliermo de AquitaniaMiraflorPas encore d'évaluation

- Life Insurance Industry Executive Summary SummaryDocument2 pagesLife Insurance Industry Executive Summary SummaryHitesh prajapatiPas encore d'évaluation

- Tahlia Kaleas S5093903 1006GBS Why Money MattersDocument6 pagesTahlia Kaleas S5093903 1006GBS Why Money MattersTahlia KaleasPas encore d'évaluation

- SV 3e PPT Chap13-NewDocument40 pagesSV 3e PPT Chap13-NewNHI HUYNH MANPas encore d'évaluation

- Expected Credit Loss Analysis For Non Banking Financial Companies PDFDocument29 pagesExpected Credit Loss Analysis For Non Banking Financial Companies PDFAnandPas encore d'évaluation

- Lembar Kerja Buku Besar UD. BUANA P3Document10 pagesLembar Kerja Buku Besar UD. BUANA P3HusniBaroqPas encore d'évaluation

- Sage X3 - Reports Examples 2008 - CHKREG (Check Register) PDFDocument4 pagesSage X3 - Reports Examples 2008 - CHKREG (Check Register) PDFcaplusinc100% (1)

- IA3 Statement of Financial PositionDocument36 pagesIA3 Statement of Financial PositionHello HiPas encore d'évaluation

- 04-Lic Credit CardDocument25 pages04-Lic Credit Cardinammurad12Pas encore d'évaluation

- Introduction To Personal FinanceDocument15 pagesIntroduction To Personal FinanceMa'am Katrina Marie MirandaPas encore d'évaluation

- Susquehanna Equipment Rentals (Group D) - PresentationDocument13 pagesSusquehanna Equipment Rentals (Group D) - PresentationNoman APas encore d'évaluation

- BNL StoresDocument4 pagesBNL Storesshanul gawshindePas encore d'évaluation

- Overview of Functions and Operations BSPDocument2 pagesOverview of Functions and Operations BSPKarla GalvezPas encore d'évaluation

- Auditing Theory Review Course Pre-Board Exam - Answer KeyDocument11 pagesAuditing Theory Review Course Pre-Board Exam - Answer KeyROMAR A. PIGAPas encore d'évaluation

- CAF-07 FAR-II Q. Paper (Final)Document5 pagesCAF-07 FAR-II Q. Paper (Final)APas encore d'évaluation

- RBI Assistant 2015 Finalcopy ExampunditDocument84 pagesRBI Assistant 2015 Finalcopy Exampunditdwaragnath100% (1)

- Incentive-Based Compensation, Contingent Commissions and Required Broker Disclosures: Is There A Meeting of The Minds?Document12 pagesIncentive-Based Compensation, Contingent Commissions and Required Broker Disclosures: Is There A Meeting of The Minds?ACELitigationWatchPas encore d'évaluation

- Goat Project NewDocument15 pagesGoat Project NewmrigendrarimalPas encore d'évaluation

- Credit Management: Hagos MirachDocument115 pagesCredit Management: Hagos Mirachዝምታ ተሻለPas encore d'évaluation

- 1178-Addendum-Change in Sponsor - HDFC LTD To HDFC Bank - July 1, 2023Document3 pages1178-Addendum-Change in Sponsor - HDFC LTD To HDFC Bank - July 1, 2023Jai Shree Ambe EnterprisesPas encore d'évaluation

- Assignment of Resource Mobilisation and Portfolio Management in HDFC BankDocument13 pagesAssignment of Resource Mobilisation and Portfolio Management in HDFC Bankashish bansalPas encore d'évaluation

- T.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Document13 pagesT.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Kadam KartikeshPas encore d'évaluation

- Impact of Digital Banks On Incumbents in SingaporeDocument20 pagesImpact of Digital Banks On Incumbents in SingaporeVarun MittalPas encore d'évaluation

- Test PracticeDocument26 pagesTest PracticeStephanie NaamaniPas encore d'évaluation

- Reflection 10Document1 pageReflection 10Rowel CampolloPas encore d'évaluation

- Other Comprehensive IncomeDocument11 pagesOther Comprehensive IncomeJoyce Ann Agdippa BarcelonaPas encore d'évaluation

- Profit TestingDocument16 pagesProfit TestingBrian KipngenoPas encore d'évaluation