Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Notification Coal India Limited General Manager PostsDocument4 pagesNotification Coal India Limited General Manager PostsRohitRajakPas encore d'évaluation

- Bhamashah FormDocument6 pagesBhamashah FormAYUSH JOSHIPas encore d'évaluation

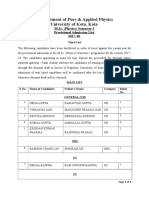

- 55 Third List M.sc. (Physics) Sem-I 21.7.17Document4 pages55 Third List M.sc. (Physics) Sem-I 21.7.17AYUSH JOSHIPas encore d'évaluation

- Exam Date RPSC Asst EngineerDocument1 pageExam Date RPSC Asst EngineerAYUSH JOSHIPas encore d'évaluation

- Study highlights prospects and challenges of GST implementation in IndiaDocument4 pagesStudy highlights prospects and challenges of GST implementation in IndiamainakroniPas encore d'évaluation

- 06 Social Science History Key Notes Ch06 Kingdoms Kings and and Early RepublicDocument2 pages06 Social Science History Key Notes Ch06 Kingdoms Kings and and Early RepublicAYUSH JOSHIPas encore d'évaluation

- Mrpabhilash 170610105224Document46 pagesMrpabhilash 170610105224AYUSH JOSHIPas encore d'évaluation

- Researchreportongst 170415155452Document48 pagesResearchreportongst 170415155452AYUSH JOSHIPas encore d'évaluation

- 2614 7775 2 PBDocument18 pages2614 7775 2 PBAYUSH JOSHIPas encore d'évaluation

- 06 Social Science History Key Notes Ch02 On The Trail of The Earliest PeopleDocument2 pages06 Social Science History Key Notes Ch02 On The Trail of The Earliest PeopleAYUSH JOSHIPas encore d'évaluation

- A Major Project Report: Master of Business AdministrationDocument71 pagesA Major Project Report: Master of Business AdministrationAYUSH JOSHIPas encore d'évaluation

- Mangalam Cement Ltd. Published by Riyaz Ahmad MBA (Brand Equity of Birla Uttam Cement)Document74 pagesMangalam Cement Ltd. Published by Riyaz Ahmad MBA (Brand Equity of Birla Uttam Cement)Riyaz Ahmad80% (5)

- Final Report ON NTPC (Ankit Doveriyal, 15) PDFDocument89 pagesFinal Report ON NTPC (Ankit Doveriyal, 15) PDFRonakKhandelwalPas encore d'évaluation

- Employee SatisfactionDocument84 pagesEmployee SatisfactionPrithviraj Kumar100% (1)

- Employee SatisfactionDocument84 pagesEmployee SatisfactionPrithviraj Kumar100% (1)

- Application Form OBC-SBC - Caste - New 28-10-2015 PDFDocument4 pagesApplication Form OBC-SBC - Caste - New 28-10-2015 PDFAYUSH JOSHIPas encore d'évaluation

- Recruitment Selection at Big BazaarDocument70 pagesRecruitment Selection at Big BazaarRAJ KUMAR MALHOTRAPas encore d'évaluation

- A Seminar Report On: "Thermal Power Plant "Document57 pagesA Seminar Report On: "Thermal Power Plant "AYUSH JOSHIPas encore d'évaluation

- Application Form OBC-SBC - Caste - New 28-10-2015 PDFDocument4 pagesApplication Form OBC-SBC - Caste - New 28-10-2015 PDFAYUSH JOSHIPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Data Flow DiagramDocument20 pagesData Flow DiagramAnkur MittalPas encore d'évaluation

- SWI FT MT940 - Understanding FORMAT: Statement Date Bank Account Number Statement NumberDocument5 pagesSWI FT MT940 - Understanding FORMAT: Statement Date Bank Account Number Statement NumbersrinivasPas encore d'évaluation

- Advantages and Disadvantages of Truck TransportationDocument2 pagesAdvantages and Disadvantages of Truck TransportationSherry ShuklaPas encore d'évaluation

- Supply Chain Management of Big BazaarDocument49 pagesSupply Chain Management of Big Bazaarnilma pais67% (3)

- Postal delivery bill for airmail from Malaysia to AustraliaDocument1 pagePostal delivery bill for airmail from Malaysia to AustraliaIda Bagus Gede PalgunaPas encore d'évaluation

- Health Financing Overview: Resource Mobilization, Risk Pooling and AllocationDocument15 pagesHealth Financing Overview: Resource Mobilization, Risk Pooling and AllocationLydia ladislausPas encore d'évaluation

- Bookkeeping Essentials For Small BusinessDocument17 pagesBookkeeping Essentials For Small BusinessAccounts and Legal100% (5)

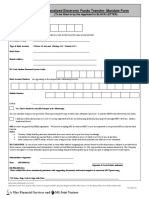

- NEFT MandateDocument1 pageNEFT MandateGirishPas encore d'évaluation

- Case Study 3 Week 9 A Case of Late DeliveriesDocument6 pagesCase Study 3 Week 9 A Case of Late DeliveriesSuraj ChoursiaPas encore d'évaluation

- GFS Setup BR100 ApDocument62 pagesGFS Setup BR100 ApAmaravathiPas encore d'évaluation

- RBI LoduDocument2 pagesRBI Lodussfd sdfsPas encore d'évaluation

- Project Report GSTDocument36 pagesProject Report GSThaz002Pas encore d'évaluation

- Employer'S Guide To Pay As You Earn (PAYE)Document20 pagesEmployer'S Guide To Pay As You Earn (PAYE)Curter Lance LusansoPas encore d'évaluation

- Mepco Full BillDocument1 pageMepco Full Billfaheemhashmi7050Pas encore d'évaluation

- Nilson Report Issue 1175 - 0036Document10 pagesNilson Report Issue 1175 - 0036John MulderPas encore d'évaluation

- Data Migration StrategyDocument16 pagesData Migration Strategyakhyar ahmadPas encore d'évaluation

- Cash BookDocument6 pagesCash BookPavan100% (2)

- EstatementDocument2 pagesEstatementjosealex134Pas encore d'évaluation

- Siklus CahayaDocument27 pagesSiklus CahayaBangYonnPas encore d'évaluation

- Rental Agreement-Terms & ConditionsDocument1 pageRental Agreement-Terms & ConditionsEasy HandPas encore d'évaluation

- Miss Jane Citizen Level 1, 8 Name Street Sydney NSW 2000: Account Details Account DetailsDocument3 pagesMiss Jane Citizen Level 1, 8 Name Street Sydney NSW 2000: Account Details Account DetailsYoutube MasterPas encore d'évaluation

- Zoom Meeting JuneDocument2 pagesZoom Meeting JuneVIRAMA KARYA - KimtaruPas encore d'évaluation

- This Is The Department Which The Customers Approach When They Are in Need of Loans. The Department IsDocument12 pagesThis Is The Department Which The Customers Approach When They Are in Need of Loans. The Department Israahul7Pas encore d'évaluation

- Oracle SCM process flowDocument12 pagesOracle SCM process flowVenkatPas encore d'évaluation

- NCMC: National Common Mobility CardDocument15 pagesNCMC: National Common Mobility CardSharad KumarPas encore d'évaluation

- Inter Company Invoicing ProcessDocument1 pageInter Company Invoicing Processaj9055537Pas encore d'évaluation

- Extras de Cont / Account StatementDocument4 pagesExtras de Cont / Account StatementSilvia Georgiana Mazilu100% (1)

- Documento PDFDocument6 pagesDocumento PDFangye08vivasPas encore d'évaluation

- Budget Cash Flow SpreadsheetDocument18 pagesBudget Cash Flow SpreadsheetSonya TkachmanPas encore d'évaluation

- SOP Resto - Cash ReceiptsDocument11 pagesSOP Resto - Cash ReceiptsGangsar PrayogiPas encore d'évaluation