Vous aimerez peut-être aussi

- Coa - M2013-004 Cash Exam Manual PDFDocument104 pagesCoa - M2013-004 Cash Exam Manual PDFAnie Guiling-Hadji Gaffar88% (8)

- Casestudy 4Document3 pagesCasestudy 4Shubhangi AgrawalPas encore d'évaluation

- Request For NOC To Avail LoanDocument3 pagesRequest For NOC To Avail LoanShirish63% (8)

- Summer Training Report - RitikaDocument69 pagesSummer Training Report - Ritikaritika_honey2377% (30)

- Financial Analysis of JSW SteelDocument71 pagesFinancial Analysis of JSW Steelkarunakar vPas encore d'évaluation

- Risk Analysis of TATA SteelDocument21 pagesRisk Analysis of TATA SteelAshok KumarPas encore d'évaluation

- Vogue 1965 Set ProductDocument16 pagesVogue 1965 Set ProductPaulina WegrzynPas encore d'évaluation

- Fundamental Analysis IDFC, Tata SteelDocument43 pagesFundamental Analysis IDFC, Tata SteelharshleePas encore d'évaluation

- Financial Analysis of Tata Steel and Jindal Steel and Power Ltd.Document34 pagesFinancial Analysis of Tata Steel and Jindal Steel and Power Ltd.O.p. SharmaPas encore d'évaluation

- MTI 7.8.19 RevisedDocument173 pagesMTI 7.8.19 RevisedomganesaPas encore d'évaluation

- JSW Steel Financial AnalysisDocument12 pagesJSW Steel Financial AnalysisAadya SuriPas encore d'évaluation

- 37 Ijmperdapr201937Document12 pages37 Ijmperdapr201937TJPRC PublicationsPas encore d'évaluation

- Rashtriya Ispat Nigam Ltd. Balance Sheet and Profit & Loss DetailsDocument2 pagesRashtriya Ispat Nigam Ltd. Balance Sheet and Profit & Loss DetailsRavi ChandPas encore d'évaluation

- Steel Industry: A Project ReportDocument13 pagesSteel Industry: A Project ReportVijendra SinghPas encore d'évaluation

- 163heg ArDocument136 pages163heg ArAmit JawadePas encore d'évaluation

- CASE Krakatau Steel (A)Document20 pagesCASE Krakatau Steel (A)Ariq LoupiasPas encore d'évaluation

- NSSMC en Ar 2013 All V Nippon SteelDocument56 pagesNSSMC en Ar 2013 All V Nippon SteelJatin KaushikPas encore d'évaluation

- Financial Statement Analysis TATA Steel and JSW SteelDocument22 pagesFinancial Statement Analysis TATA Steel and JSW Steelshivam kumarPas encore d'évaluation

- JSW Steel Full 2010Document106 pagesJSW Steel Full 2010Nishant SharmaPas encore d'évaluation

- Executive Summary Industry OverviewDocument5 pagesExecutive Summary Industry OverviewVarun SinghPas encore d'évaluation

- Company Name: Shivalik Bimetal Controls LTDDocument4 pagesCompany Name: Shivalik Bimetal Controls LTDSandyPas encore d'évaluation

- Financial Reporting Statement Analysis Project Report: Name of The Company: Tata SteelDocument35 pagesFinancial Reporting Statement Analysis Project Report: Name of The Company: Tata SteelRagava KarthiPas encore d'évaluation

- SAIL Performance Declines in 2015-16Document11 pagesSAIL Performance Declines in 2015-16Bloomy devasiaPas encore d'évaluation

- PunnuDocument9 pagesPunnuPurnanand SathuaPas encore d'évaluation

- Ezz Steel Strategic Auditing PDFDocument24 pagesEzz Steel Strategic Auditing PDFhanan100% (1)

- Siemens: CMP: INR655 TP: INR746Document8 pagesSiemens: CMP: INR655 TP: INR746spatel1972Pas encore d'évaluation

- Analysis & Financial Performnce of AccDocument25 pagesAnalysis & Financial Performnce of Accneeks818100% (1)

- Fluidomat BSE CAREDocument5 pagesFluidomat BSE CAREayushidgr8Pas encore d'évaluation

- Financial Performance Analysis of Exide IndustriesDocument11 pagesFinancial Performance Analysis of Exide IndustriesAnupriya SenPas encore d'évaluation

- Mid Cap Ideas - Value and Growth Investing 250112 - 11 - 0602120242Document21 pagesMid Cap Ideas - Value and Growth Investing 250112 - 11 - 0602120242Chetan MaheshwariPas encore d'évaluation

- Equity Asset Valuation Mughal SteelsDocument11 pagesEquity Asset Valuation Mughal SteelsHabiba PashaPas encore d'évaluation

- Angel Broking: Bharat Heavy ElectricalsDocument27 pagesAngel Broking: Bharat Heavy ElectricalsChintan JethvaPas encore d'évaluation

- AWI investor presentation highlights cost cuts and emerging markets focusDocument31 pagesAWI investor presentation highlights cost cuts and emerging markets focushelix126Pas encore d'évaluation

- Buy JSW Steel CMP 317Document5 pagesBuy JSW Steel CMP 317Deepak GPas encore d'évaluation

- Contents:-: BR R R R RDocument13 pagesContents:-: BR R R R RShahib ZadPas encore d'évaluation

- Arcelormittal Sa: Summary of Rated InstrumentsDocument6 pagesArcelormittal Sa: Summary of Rated Instrumentspavan reddyPas encore d'évaluation

- Financial Ratio Analysis of Indus Motor Company LTDDocument40 pagesFinancial Ratio Analysis of Indus Motor Company LTDAurang ZaibPas encore d'évaluation

- Mathematical Modeling With Sem - PLS in Elimination of Six Big Losses To Reduce Production Cost of Steel FactoriesDocument6 pagesMathematical Modeling With Sem - PLS in Elimination of Six Big Losses To Reduce Production Cost of Steel FactoriesInternational Journal of Innovative Science and Research TechnologyPas encore d'évaluation

- Comparative Analysis of SailDocument60 pagesComparative Analysis of SailKajal YadavPas encore d'évaluation

- Indian Steel Companies: Financial Restructuring Key To Turnaround"Document6 pagesIndian Steel Companies: Financial Restructuring Key To Turnaround"Khushboo GuptaPas encore d'évaluation

- Exide Industries: Performance HighlightsDocument12 pagesExide Industries: Performance HighlightsAngel BrokingPas encore d'évaluation

- National Thermal Power Corporation LimitedDocument15 pagesNational Thermal Power Corporation Limitedprathamesh tawarePas encore d'évaluation

- Shaily Engineering Plastics Limited-09-25-2019Document4 pagesShaily Engineering Plastics Limited-09-25-2019Ashutosh Gupta100% (1)

- Steel CRGPDocument7 pagesSteel CRGPPrakhar RatheePas encore d'évaluation

- Hindalco Full Annual Report 2015 16Document200 pagesHindalco Full Annual Report 2015 16neettiyath1Pas encore d'évaluation

- Increase Market Share with New StrategiesDocument21 pagesIncrease Market Share with New StrategiesjilnaPas encore d'évaluation

- Financial Statement Analysis On JSW STEEL LTDDocument10 pagesFinancial Statement Analysis On JSW STEEL LTDSanthosh KcPas encore d'évaluation

- Developing A Growth Strategy For The CompanyDocument11 pagesDeveloping A Growth Strategy For The CompanyAbhinandan ChatterjeePas encore d'évaluation

- Valuation of Meghna GroupDocument23 pagesValuation of Meghna GroupFarzana Fariha Lima0% (1)

- Cost Leadership Strategy of TATA Steel in the Global Steel IndustryDocument8 pagesCost Leadership Strategy of TATA Steel in the Global Steel IndustryTabrej KhanPas encore d'évaluation

- SIIL - Annual Report 2010-11Document188 pagesSIIL - Annual Report 2010-11SwamiPas encore d'évaluation

- Hindalco Industries Limited: Investor Presentation on Novelis' Successful Turnaround StoryDocument46 pagesHindalco Industries Limited: Investor Presentation on Novelis' Successful Turnaround StoryPulkit GuptaPas encore d'évaluation

- Ace Designers-R-05042018 PDFDocument7 pagesAce Designers-R-05042018 PDFkachadaPas encore d'évaluation

- MarketingDocument40 pagesMarketingnprash123Pas encore d'évaluation

- Jindal Steel & Power LimitedDocument6 pagesJindal Steel & Power Limitedbhargavi2023Pas encore d'évaluation

- Vedanta GrowthDocument38 pagesVedanta Growthsudeep khandelwalPas encore d'évaluation

- Case Study: Industry: Steel Company: AmrelisteelsDocument15 pagesCase Study: Industry: Steel Company: AmrelisteelswaleedPas encore d'évaluation

- BYD Annual Report 2011Document106 pagesBYD Annual Report 2011krabadiPas encore d'évaluation

- Tata Steel FSA - Final PresentationDocument35 pagesTata Steel FSA - Final Presentationapi-3712367100% (1)

- Metal Heat Treating World Summary: Market Values & Financials by CountryD'EverandMetal Heat Treating World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Industrial Gases, Type World Summary: Market Values & Financials by CountryD'EverandIndustrial Gases, Type World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Nonmetallic Coated Abrasive Products, Buffing & Polishing Wheels & Laps World Summary: Market Sector Values & Financials by CountryD'EverandNonmetallic Coated Abrasive Products, Buffing & Polishing Wheels & Laps World Summary: Market Sector Values & Financials by CountryPas encore d'évaluation

- Alternators, Generators & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryD'EverandAlternators, Generators & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Aluminum & Copper Semi-Finished Supplies World Summary: Market Values & Financials by CountryD'EverandAluminum & Copper Semi-Finished Supplies World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Carburettors, Fuel Injection & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryD'EverandCarburettors, Fuel Injection & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryPas encore d'évaluation

- ICreate MillionsDocument84 pagesICreate Millionsapi-3802837100% (4)

- Grant Application GuideDocument2 pagesGrant Application GuideMunish Dogra100% (1)

- Chapter 10a - Long Term Finance - BondsDocument6 pagesChapter 10a - Long Term Finance - BondsTAN YUN YUNPas encore d'évaluation

- NIB Bank Internship ReportDocument41 pagesNIB Bank Internship ReportAdnan Khan Alizai86% (7)

- Money CreationDocument28 pagesMoney Creationathirah jamaludinPas encore d'évaluation

- KFSLetter 2Document2 pagesKFSLetter 2unni kuttanPas encore d'évaluation

- Residential Property Development Real Estate Management ProjectDocument11 pagesResidential Property Development Real Estate Management ProjectRahul DuttPas encore d'évaluation

- History of BankingDocument6 pagesHistory of Bankinglianna mariePas encore d'évaluation

- EG2P PhilippinesDocument40 pagesEG2P PhilippinespuppeteyesPas encore d'évaluation

- Contracts Course Outline Revised BQS 112Document7 pagesContracts Course Outline Revised BQS 112MichaelKipronoPas encore d'évaluation

- Go MS 129 GST 30122018Document2 pagesGo MS 129 GST 30122018hussain100% (1)

- List of APOnline ServicesDocument2 pagesList of APOnline ServicesAnonymous uIJIBNaFIPas encore d'évaluation

- Standard Procedure For Empanelment of ValuersDocument21 pagesStandard Procedure For Empanelment of ValuersEr Rajesh KumarPas encore d'évaluation

- J.P. Morgan - Taking EM Asia's Pulse PDFDocument7 pagesJ.P. Morgan - Taking EM Asia's Pulse PDFkumarrajdeepbsrPas encore d'évaluation

- Loans and Deposits ExplainedDocument8 pagesLoans and Deposits ExplainedVsgg NniaPas encore d'évaluation

- Annual Report HighlightsDocument424 pagesAnnual Report Highlightsborisg3Pas encore d'évaluation

- True / False Questions: Liquidity RiskDocument25 pagesTrue / False Questions: Liquidity Risklatifa hnPas encore d'évaluation

- 4 Journal EntriesDocument2 pages4 Journal Entriesapi-299265916Pas encore d'évaluation

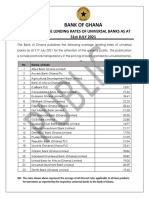

- Average Lending Rates As at July 2021Document1 pageAverage Lending Rates As at July 2021Fuaad DodooPas encore d'évaluation

- Legislation and RegulationsDocument6 pagesLegislation and RegulationsSrini VasanPas encore d'évaluation

- Ach Code CardDocument2 pagesAch Code CardSankaetPathakPas encore d'évaluation

- FI/CO Reports GuideDocument4 pagesFI/CO Reports GuideVinoth Kumar PeethambaramPas encore d'évaluation

- DPC PRJCT 9th SemDocument8 pagesDPC PRJCT 9th SemStuti BaradiaPas encore d'évaluation

- Financial Planning Part 2Document33 pagesFinancial Planning Part 2Carlsberg AndresPas encore d'évaluation