Vous aimerez peut-être aussi

- The Nakshatra of Vedic AstrologyDocument9 pagesThe Nakshatra of Vedic Astrologyashishbhagoria100% (1)

- 144 SQRRDocument19 pages144 SQRRcaptainamerica201390% (20)

- LARCA Audit & RecommendationsDocument34 pagesLARCA Audit & RecommendationsTerry Maynard100% (1)

- Company Law and PracticeDocument608 pagesCompany Law and PracticeosaiePas encore d'évaluation

- Vijay Malik Template v2Document38 pagesVijay Malik Template v2KiranPas encore d'évaluation

- Organic Farm Business Plan PDFDocument31 pagesOrganic Farm Business Plan PDFv30003v100% (1)

- Dependency Form PDFDocument5 pagesDependency Form PDFVivek VenugopalPas encore d'évaluation

- The Salvage Law Act No. 2616: Sanilyn V. Ramirez Llb3Document9 pagesThe Salvage Law Act No. 2616: Sanilyn V. Ramirez Llb3Syannil ViePas encore d'évaluation

- 00 MS Excel Practical Questions-11257Document6 pages00 MS Excel Practical Questions-11257Soumyaranjan Thakur50% (2)

- Cluster Acceptance Preparation - Rev1 (DT Oss Kpi Achievement)Document17 pagesCluster Acceptance Preparation - Rev1 (DT Oss Kpi Achievement)BamsPas encore d'évaluation

- Introduction To Regular Income TaxDocument25 pagesIntroduction To Regular Income TaxShelley TabadaPas encore d'évaluation

- Trading With Time Time SampleDocument12 pagesTrading With Time Time SampleRasmi Ranjan100% (1)

- Gann, W.D. - On Cycles & Trading - Forecasting RulesDocument5 pagesGann, W.D. - On Cycles & Trading - Forecasting Rulesrpetrs100% (3)

- Kurva RPM THDDocument3 pagesKurva RPM THDWulan MaharaniPas encore d'évaluation

- Disb ProjectionsDocument2 pagesDisb ProjectionsAnshuman GuptaPas encore d'évaluation

- Two-Wheeler Sales To Rise in FY23 Margins To Remain Under PressureDocument4 pagesTwo-Wheeler Sales To Rise in FY23 Margins To Remain Under Pressurechinmay.patilPas encore d'évaluation

- Power Demand of West-DiscomDocument9 pagesPower Demand of West-DiscomAmit Kumar SinghPas encore d'évaluation

- Contoh Biaya ProduksiDocument6 pagesContoh Biaya ProduksiRobbenWPas encore d'évaluation

- Contoh Biaya ProduksiDocument6 pagesContoh Biaya ProduksiRobbenWPas encore d'évaluation

- CFM Lbo ModelDocument3 pagesCFM Lbo ModelReusPas encore d'évaluation

- District 103 DonaldDocument58 pagesDistrict 103 DonaldJeremy Cromwell MPas encore d'évaluation

- NPV and Irr Rules: The Discount Rate Is 10%Document8 pagesNPV and Irr Rules: The Discount Rate Is 10%cizarPas encore d'évaluation

- Contoh Biaya ProduksiDocument6 pagesContoh Biaya Produksijenifir marchPas encore d'évaluation

- BV Practical ProblemsDocument18 pagesBV Practical ProblemsSaloni Jain 1820343Pas encore d'évaluation

- Assumptions: Target MarketDocument6 pagesAssumptions: Target MarketКамиль БайбуринPas encore d'évaluation

- Lenovo PresentationDocument21 pagesLenovo PresentationAneel Amdani100% (1)

- Worksheet in GlobalFree-CashBank - Case Study - 2018Document2 pagesWorksheet in GlobalFree-CashBank - Case Study - 2018rashmianand712Pas encore d'évaluation

- HW CHP 1Document8 pagesHW CHP 1Ava AvaPas encore d'évaluation

- República Bolivariana de Venezuela Instituto Universitario Politécnico "Santiago Mariño" Control de Calidad San Cristóbal - Edo TáchiraDocument4 pagesRepública Bolivariana de Venezuela Instituto Universitario Politécnico "Santiago Mariño" Control de Calidad San Cristóbal - Edo Táchirajhonatan rosalesPas encore d'évaluation

- Institute of Business ManagementDocument3 pagesInstitute of Business ManagementAli KhanPas encore d'évaluation

- Samsung QN65QN90ADocument3 pagesSamsung QN65QN90ADavid KatzmaierPas encore d'évaluation

- Bank Customer ChurnDocument715 pagesBank Customer ChurnTố NiênPas encore d'évaluation

- SC2005 09Document39 pagesSC2005 09Jonathan WuPas encore d'évaluation

- ATHREPAPR2022Document19 pagesATHREPAPR2022prabhuPas encore d'évaluation

- Team7 FMPhase2 Trent SENIORSDocument75 pagesTeam7 FMPhase2 Trent SENIORSNisarg Rupani100% (1)

- CHART BY LINE (March)Document5 pagesCHART BY LINE (March)Fabio GonzalezPas encore d'évaluation

- Led UsbDocument1 pageLed UsbwillkinsonthomyPas encore d'évaluation

- Consultancy: Resource Generation (Testing & Consultancy)Document1 pageConsultancy: Resource Generation (Testing & Consultancy)RajPas encore d'évaluation

- Economia Empresarial Mod 2Document8 pagesEconomia Empresarial Mod 2Isaam DomínguezPas encore d'évaluation

- MAU207Document6 pagesMAU207csclzPas encore d'évaluation

- CPB - Technical - Catalogue 510Document1 pageCPB - Technical - Catalogue 510rajPas encore d'évaluation

- Annual Report 2015Document150 pagesAnnual Report 2015Ajuma OnyangoPas encore d'évaluation

- Vizio M65Q7-J01 CNET Review Calibration ResultsDocument3 pagesVizio M65Q7-J01 CNET Review Calibration ResultsDavid KatzmaierPas encore d'évaluation

- A Brave New World of Great Viewing ChoicesDocument11 pagesA Brave New World of Great Viewing ChoicesNamrata JainPas encore d'évaluation

- Form Pccs StrokeDocument1 pageForm Pccs Strokeegan diarjoPas encore d'évaluation

- March GragphDocument3 pagesMarch GragphsucijaPas encore d'évaluation

- Book 1Document9 pagesBook 1Hajar HajarPas encore d'évaluation

- Actual 2018 Per Club - OperationDocument59 pagesActual 2018 Per Club - OperationAnonymous 3QWXb5qxfNPas encore d'évaluation

- 0 - 10000 1-Jan-17 1 3500 15-Feb-18 2 4500 1-Mar-19 3 6500 25-Mar-20 4 7000 15-Mar-21 5 7500 5-Mar-22 Discount Rate 10% 41.93% Mirr 28%Document15 pages0 - 10000 1-Jan-17 1 3500 15-Feb-18 2 4500 1-Mar-19 3 6500 25-Mar-20 4 7000 15-Mar-21 5 7500 5-Mar-22 Discount Rate 10% 41.93% Mirr 28%Alpana RastogiPas encore d'évaluation

- Atten S7 CeDocument1 pageAtten S7 CeKmw18 ce013Pas encore d'évaluation

- Unit 1: Regression StatisticsDocument6 pagesUnit 1: Regression StatisticsAnisa Mutia UlfaPas encore d'évaluation

- Total Income - Annual: Sales Sales YoyDocument16 pagesTotal Income - Annual: Sales Sales YoyKshatrapati SinghPas encore d'évaluation

- Key Indicators: Analysis of EFSA Report FYE 30 June 2014Document16 pagesKey Indicators: Analysis of EFSA Report FYE 30 June 2014mostafaPas encore d'évaluation

- Managerial Economics 7Document6 pagesManagerial Economics 7John karlo TarigaPas encore d'évaluation

- PD 957: BP 220 SpecsDocument1 pagePD 957: BP 220 SpecsGDLT ytPas encore d'évaluation

- Boeing Current Market Outlook 2012 2031 PDFDocument43 pagesBoeing Current Market Outlook 2012 2031 PDFSani SanjayaPas encore d'évaluation

- Sample Test Result AnalysisDocument5 pagesSample Test Result AnalysisMARISSA L. BAROROPas encore d'évaluation

- April YTD BudgetDocument2 pagesApril YTD Budgetjarrett_renshaw5850100% (1)

- Aalberts 2015Document108 pagesAalberts 2015jasper laarmansPas encore d'évaluation

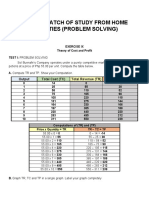

- Second Batch of Study From Home Activities (Problem Solving)Document8 pagesSecond Batch of Study From Home Activities (Problem Solving)Carmela Kristine JordaPas encore d'évaluation

- Equty Analysis by Rameez Fazal Tayyeba JayanthDocument17 pagesEquty Analysis by Rameez Fazal Tayyeba JayanthtayyebaPas encore d'évaluation

- Company Background:: West Coast Paper Mills Ltd. BuyDocument4 pagesCompany Background:: West Coast Paper Mills Ltd. BuyPravin YeluriPas encore d'évaluation

- Mark Allocation-HY 1Document6 pagesMark Allocation-HY 1abdurrobawsPas encore d'évaluation

- 2014-2018 Batch Resut Analysis Up To I-I With I-I Revaluation ResultsDocument200 pages2014-2018 Batch Resut Analysis Up To I-I With I-I Revaluation ResultsKrishna Murthy100% (1)

- SDR Activit y SouthDocument22 pagesSDR Activit y SouthAdil MuradPas encore d'évaluation

- Cost SteetDocument5 pagesCost SteetGaurav KhannaPas encore d'évaluation

- BCG MatrixDocument1 pageBCG MatrixFritz IgnacioPas encore d'évaluation

- Jan - Mars 20 Jan - Mai 20 Jan - Juin 20 Jan - Juil 20 Jan-Juil/LFR (%)Document6 pagesJan - Mars 20 Jan - Mai 20 Jan - Juin 20 Jan - Juil 20 Jan-Juil/LFR (%)DahBellahiPas encore d'évaluation

- Indian Auto SectorDocument14 pagesIndian Auto SectorAnkur Sharda100% (19)

- TenLawsOfTrading PDFDocument12 pagesTenLawsOfTrading PDFRasmi RanjanPas encore d'évaluation

- Misbehaving The Making of Behavioral EcoDocument8 pagesMisbehaving The Making of Behavioral EcoAlex SiaPas encore d'évaluation

- IMV Equity Report GSFCDocument4 pagesIMV Equity Report GSFCRasmi RanjanPas encore d'évaluation

- Zee Entertainment - Elara Securities - 19 August 2020Document10 pagesZee Entertainment - Elara Securities - 19 August 2020Rasmi RanjanPas encore d'évaluation

- Ffirmff L: LimitedDocument1 pageFfirmff L: LimitedRasmi RanjanPas encore d'évaluation

- LME Trading Calendar 2018 2028Document2 pagesLME Trading Calendar 2018 2028Rasmi RanjanPas encore d'évaluation

- Here Are The Stocks and Sectors That Are Likely To Lead The Next Bull Run - The Economic TimesDocument7 pagesHere Are The Stocks and Sectors That Are Likely To Lead The Next Bull Run - The Economic TimesRasmi RanjanPas encore d'évaluation

- Taher Badshah On How A Contra Investor Can Make Money in A Crowded Trade - The Economic TimesDocument4 pagesTaher Badshah On How A Contra Investor Can Make Money in A Crowded Trade - The Economic TimesRasmi RanjanPas encore d'évaluation

- Innovation 2015Document13 pagesInnovation 2015elisaPas encore d'évaluation

- Kajaria CeraDocument3 pagesKajaria CeraRasmi RanjanPas encore d'évaluation

- The Triple F' (Food, Fodder and Fuel) Crop Sweet Potato (Ipomoea Batatas (L.) Lam.)Document11 pagesThe Triple F' (Food, Fodder and Fuel) Crop Sweet Potato (Ipomoea Batatas (L.) Lam.)Rasmi RanjanPas encore d'évaluation

- En 2012 1000487 PDFDocument173 pagesEn 2012 1000487 PDFRasmi RanjanPas encore d'évaluation

- 1453852098IOP Presentation March 2018Document22 pages1453852098IOP Presentation March 2018Rasmi RanjanPas encore d'évaluation

- MOST 80349200 Value-Presentation-March-2018Document33 pagesMOST 80349200 Value-Presentation-March-2018Rasmi RanjanPas encore d'évaluation

- AgricultureDocument111 pagesAgricultureRasmi RanjanPas encore d'évaluation

- 384140093PMS Communique - March 2018Document6 pages384140093PMS Communique - March 2018Rasmi RanjanPas encore d'évaluation

- A Category Shares NSEDocument6 pagesA Category Shares NSERajesh RamPas encore d'évaluation

- Probable Marketing Strategies of Fly Ash Bricks in West BengalDocument25 pagesProbable Marketing Strategies of Fly Ash Bricks in West Bengal87krishanPas encore d'évaluation

- AgricultureDocument111 pagesAgricultureRasmi RanjanPas encore d'évaluation

- Fundamentals of Internet:: 323Document17 pagesFundamentals of Internet:: 323sachinPas encore d'évaluation

- Internet BasicsDocument9 pagesInternet BasicsromaPas encore d'évaluation

- Investment Analysis and Portfolio Management 2010Document166 pagesInvestment Analysis and Portfolio Management 2010johnsm2010Pas encore d'évaluation

- Computer FundamentalsDocument126 pagesComputer Fundamentalsntrdas100% (16)

- HSL PCG GIC Housing Finance LTD - Dec 2017Document13 pagesHSL PCG GIC Housing Finance LTD - Dec 2017Rasmi RanjanPas encore d'évaluation

- Ifive Inc.: 8/F Zeta Tower Robinsons Bridgetowne C5 Road, Ugong Norte, 1110 Quezon CityDocument1 pageIfive Inc.: 8/F Zeta Tower Robinsons Bridgetowne C5 Road, Ugong Norte, 1110 Quezon CityReymar BanaagPas encore d'évaluation

- Mission & VisionDocument41 pagesMission & Visionparthshah123456789Pas encore d'évaluation

- Evidencia 5 Summary Export Import Theory V2Document6 pagesEvidencia 5 Summary Export Import Theory V2Alexis Montoya ObandoPas encore d'évaluation

- Organizational Analysis: Week 4 Questions (Agency Theory)Document5 pagesOrganizational Analysis: Week 4 Questions (Agency Theory)api-25897035Pas encore d'évaluation

- MergerDocument41 pagesMergerarulselvi_a9100% (1)

- SUGI Report - III - 2018Document87 pagesSUGI Report - III - 2018KevinPas encore d'évaluation

- Government Accounting and AuditingDocument190 pagesGovernment Accounting and AuditingCharles John Palabrica CubarPas encore d'évaluation

- Impact of Financial Leverage On Financial Performance: Special Reference To John Keells Holdings PLC in Sri LankaDocument6 pagesImpact of Financial Leverage On Financial Performance: Special Reference To John Keells Holdings PLC in Sri Lankarobert0rojerPas encore d'évaluation

- Acknowledgment For Request For New PAN Application (881030119090704)Document1 pageAcknowledgment For Request For New PAN Application (881030119090704)Mahesh YadaPas encore d'évaluation

- Chapters 5-8 Microeconomics Test Review QuestionsDocument157 pagesChapters 5-8 Microeconomics Test Review Questionscfesel4557% (7)

- Chapter 4: Applying Excel: Chapter 4 Cost-Volume-Profit Relationships - Solution Manual ContentDocument9 pagesChapter 4: Applying Excel: Chapter 4 Cost-Volume-Profit Relationships - Solution Manual ContentMan Tran Y NhiPas encore d'évaluation

- Finance Act 2013Document12 pagesFinance Act 2013Tapia MelvinPas encore d'évaluation

- Net Present Value (NPV) Definition - Calculation - ExamplesDocument3 pagesNet Present Value (NPV) Definition - Calculation - ExamplesKadiri OlanrewajuPas encore d'évaluation

- ECU 302 Introductory Notes and Course OutlineDocument21 pagesECU 302 Introductory Notes and Course OutlineCivil EngineeringPas encore d'évaluation

- G.O.Ms - No.39, Dated24.06.2020new G.O PAYMENT OF SALARIES - GO - FINALDocument2 pagesG.O.Ms - No.39, Dated24.06.2020new G.O PAYMENT OF SALARIES - GO - FINALvaranasirk1Pas encore d'évaluation

- Form Template Format Slip Gaji Karyawan Swasta Sederhana Dalam ExcelDocument1 pageForm Template Format Slip Gaji Karyawan Swasta Sederhana Dalam ExcelGita RahmayaniPas encore d'évaluation

- CH 7Document41 pagesCH 7Abdulrahman AlotaibiPas encore d'évaluation

- Prof SB Salter 6815 Quiz 2: Q - Total Fixed Costs ProfitDocument10 pagesProf SB Salter 6815 Quiz 2: Q - Total Fixed Costs Profitmae KuanPas encore d'évaluation

- Pricing DecisionsDocument3 pagesPricing DecisionsMarcuz AizenPas encore d'évaluation

- PFRS 3, Business CombinationsDocument39 pagesPFRS 3, Business Combinationsjulia4razoPas encore d'évaluation

- Medium Term Business Plan 3Document16 pagesMedium Term Business Plan 3Ravi HettigePas encore d'évaluation

- Unit 1: IATA Accreditation Requirements: Learning Objectives Key Learning PointsDocument1 pageUnit 1: IATA Accreditation Requirements: Learning Objectives Key Learning PointsSitakanta AcharyaPas encore d'évaluation

- What Are The Indirect TaxesDocument3 pagesWhat Are The Indirect Taxesatmiya2010Pas encore d'évaluation

- Exercise 05 (Individual Graded)Document2 pagesExercise 05 (Individual Graded)nininini2923Pas encore d'évaluation