Vous aimerez peut-être aussi

- Abscbn Broadcasting Corp. v. Cta DigestDocument3 pagesAbscbn Broadcasting Corp. v. Cta DigestkathrynmaydevezaPas encore d'évaluation

- RP Vs City of KadapawenDocument2 pagesRP Vs City of KadapawenHonorio Bartholomew ChanPas encore d'évaluation

- CIR v. Hedcor Sibulan, Inc.Document2 pagesCIR v. Hedcor Sibulan, Inc.SophiaFrancescaEspinosa100% (1)

- Gatchalian Vs NaldozaDocument2 pagesGatchalian Vs NaldozaPatrick Ramos100% (3)

- CIR Vs Hambrecht and Quist PhilDocument2 pagesCIR Vs Hambrecht and Quist PhilElerlenne Lim100% (1)

- Taganito vs. Commissioner (1995)Document2 pagesTaganito vs. Commissioner (1995)cmv mendozaPas encore d'évaluation

- FDCP vs. Colon Heritage DigestDocument4 pagesFDCP vs. Colon Heritage DigestGeorge Almeda44% (9)

- Renato Diaz v. Secretary of Finance: VAT on Tollway FeesDocument2 pagesRenato Diaz v. Secretary of Finance: VAT on Tollway FeesDexter MantosPas encore d'évaluation

- ALEXANDER HOWDEN & CO., LTD Vs CIRDocument2 pagesALEXANDER HOWDEN & CO., LTD Vs CIRMariz GalangPas encore d'évaluation

- NPC vs City of Cabanatuan rules on LGU authority to tax govt corpsDocument3 pagesNPC vs City of Cabanatuan rules on LGU authority to tax govt corpsMa Gabriellen Quijada-Tabuñag100% (1)

- Jardeleza V. PeopleDocument4 pagesJardeleza V. PeopleGrace0% (2)

- Gerbert Corpuz Vs Daisylyn Tirol StoDocument2 pagesGerbert Corpuz Vs Daisylyn Tirol StoopislotoPas encore d'évaluation

- CIR Vs CTA DigestDocument2 pagesCIR Vs CTA DigestAbilene Joy Dela Cruz83% (6)

- RA 7167 Effective DateDocument1 pageRA 7167 Effective DateTani AngubPas encore d'évaluation

- 40 Nippon Life V CIRDocument2 pages40 Nippon Life V CIRMae SampangPas encore d'évaluation

- Procter & Gamble vs. Commissioner of Customs, 23 SCRA 691 (1968) DigestDocument3 pagesProcter & Gamble vs. Commissioner of Customs, 23 SCRA 691 (1968) Digestchingxetolle100% (1)

- CIR vs CTA and Smith Kline - Deduction of Home Office Overhead Expenses Not Limited to Contract AmountDocument1 pageCIR vs CTA and Smith Kline - Deduction of Home Office Overhead Expenses Not Limited to Contract AmountMini U. SorianoPas encore d'évaluation

- CTA upholds Fortune Tobacco tax refundDocument1 pageCTA upholds Fortune Tobacco tax refundlenvfPas encore d'évaluation

- Philamlife V Cta Case DigestDocument2 pagesPhilamlife V Cta Case DigestAnonymous BvmMuBSwPas encore d'évaluation

- Southern Cross Cement Corporation vs. Cement Manufacturers Association of The PhilippinesDocument9 pagesSouthern Cross Cement Corporation vs. Cement Manufacturers Association of The PhilippinesAmiel Arrieta ArañezPas encore d'évaluation

- Deutsche Bank V CIR (Digest)Document2 pagesDeutsche Bank V CIR (Digest)Cecille Mangaser67% (9)

- Film Development Council of The Philippines vs. ColonDocument1 pageFilm Development Council of The Philippines vs. ColonElaine Honrade100% (1)

- Tax Doctrine on Willful BlindnessDocument4 pagesTax Doctrine on Willful BlindnessKatPas encore d'évaluation

- PCGG Vs CojuangcoDocument3 pagesPCGG Vs CojuangcoChic PabalanPas encore d'évaluation

- I.3 Gaston Vs Republic Planter GR No. 77194 03151988 PDFDocument3 pagesI.3 Gaston Vs Republic Planter GR No. 77194 03151988 PDFbabyclaire17Pas encore d'évaluation

- Atlas Consolidated Mining Vs CIR, GR 159471, Jan. 26, 2011Document2 pagesAtlas Consolidated Mining Vs CIR, GR 159471, Jan. 26, 2011katentom-1Pas encore d'évaluation

- Bar Matter No. 553 Ulep Vs Legal ClinicDocument14 pagesBar Matter No. 553 Ulep Vs Legal ClinicEunice NavarroPas encore d'évaluation

- Philippines vs Que Po Lay Case Digest on Publication of Bank CircularsDocument1 pagePhilippines vs Que Po Lay Case Digest on Publication of Bank CircularsMiley LangPas encore d'évaluation

- 77 Misamis Oriental Association of Coco Traders Vs Dept of Finance SecretaryDocument1 page77 Misamis Oriental Association of Coco Traders Vs Dept of Finance SecretaryMalolosFire BulacanPas encore d'évaluation

- Collector V USTDocument4 pagesCollector V USTCamille Britanico100% (1)

- CIR v. Philippine Airlines Tax RefundDocument2 pagesCIR v. Philippine Airlines Tax RefundSarah RosalesPas encore d'évaluation

- Elegado Vs Cta DigestDocument2 pagesElegado Vs Cta DigestJames Amiel Vergara67% (3)

- People Vs LiceraDocument1 pagePeople Vs LiceralyleregenciaPas encore d'évaluation

- CIR vs. Hantex - DigestDocument2 pagesCIR vs. Hantex - DigestZiazel Therese67% (3)

- American Airlines Tax CaseDocument6 pagesAmerican Airlines Tax CaseDarrel John Sombilon100% (1)

- 5 - CIR vs. Hon. Raul M. GonzalezDocument6 pages5 - CIR vs. Hon. Raul M. GonzalezJaye Querubin-FernandezPas encore d'évaluation

- Fernandez vs. FernandezDocument1 pageFernandez vs. FernandezKitchie San PedroPas encore d'évaluation

- Fallo Prevails Over Decision BodyDocument2 pagesFallo Prevails Over Decision BodyVirnadette LopezPas encore d'évaluation

- Nippon Life Insurance Co., Inc. v. CIR, CTA Case No. 6142, February 4, 2002Document21 pagesNippon Life Insurance Co., Inc. v. CIR, CTA Case No. 6142, February 4, 2002EnzoGarcia100% (1)

- CIR vs. LA FLOR DEla ISABELA, 2019Document3 pagesCIR vs. LA FLOR DEla ISABELA, 2019Fenina Reyes0% (1)

- BIR Vs CA and Sps. ManlyDocument1 pageBIR Vs CA and Sps. ManlyJayPas encore d'évaluation

- Fort Bonifacio Dev Corp Vs CIR DigestDocument1 pageFort Bonifacio Dev Corp Vs CIR DigestChristian John Dela CruzPas encore d'évaluation

- Mining Claim DisputeDocument2 pagesMining Claim DisputeMa. Cristel Ann Sy100% (1)

- Tañada v Tuvera ruling on publicationDocument1 pageTañada v Tuvera ruling on publicationJazem Ansama71% (7)

- Case Digest of CIR v. Aichi ForgingDocument4 pagesCase Digest of CIR v. Aichi ForgingJeng Pion100% (1)

- Cui VS CuiDocument2 pagesCui VS CuiKamille Villalobos100% (1)

- Republic V Aquafresh SeafoodDocument2 pagesRepublic V Aquafresh SeafoodRia Evita RevitaPas encore d'évaluation

- DIGEST John Hay Peoples Alternative Coalition Vs Lim DigestDocument2 pagesDIGEST John Hay Peoples Alternative Coalition Vs Lim DigestDhin Carag100% (5)

- VRB Tax Authority and Municipal Boundary Changes ChallengedDocument9 pagesVRB Tax Authority and Municipal Boundary Changes ChallengedErick Jay InokPas encore d'évaluation

- BIR Ruling (DA-287-07) May 8, 2007Document3 pagesBIR Ruling (DA-287-07) May 8, 2007Raiya AngelaPas encore d'évaluation

- Umali Vs EstanislaoDocument2 pagesUmali Vs EstanislaoReyna RemultaPas encore d'évaluation

- Republic vs. AblazaDocument1 pageRepublic vs. Ablazarcmj_supremo3193100% (2)

- BIR vs. CA, Sps. Antonio Villan Manly (Digest)Document1 pageBIR vs. CA, Sps. Antonio Villan Manly (Digest)Darwin Dionisio ClementePas encore d'évaluation

- CIR v. Citytrust Investment Phils., Inc. and Asiabank Corporation v. CIRDocument3 pagesCIR v. Citytrust Investment Phils., Inc. and Asiabank Corporation v. CIRAila Amp100% (1)

- People V Kintanar Case DigestDocument3 pagesPeople V Kintanar Case DigestaiceljoyPas encore d'évaluation

- Cir VS BurroughDocument2 pagesCir VS BurroughMP ManliclicPas encore d'évaluation

- CASE 08 - CIR v. Burroughs 1986Document2 pagesCASE 08 - CIR v. Burroughs 1986bernadeth ranolaPas encore d'évaluation

- ABS-CBN v. CTA, G.R. No. L-52306, 12 October 1981Document10 pagesABS-CBN v. CTA, G.R. No. L-52306, 12 October 1981Jennilyn Gulfan YasePas encore d'évaluation

- Abs-Cbn V CTADocument2 pagesAbs-Cbn V CTASocPas encore d'évaluation

- 8 ABS CBN Broadcasting Corp. Vs CTADocument14 pages8 ABS CBN Broadcasting Corp. Vs CTAMargarette Pinkihan SarmientoPas encore d'évaluation

- 2018 Labor Law and Social Legislation Bar Examinatons Questionnaire (From SC - Judiciary.gov - PH)Document10 pages2018 Labor Law and Social Legislation Bar Examinatons Questionnaire (From SC - Judiciary.gov - PH)Ernest Talingdan CastroPas encore d'évaluation

- 2018 Politcial and International Law Bar Exam Questions (From SC - Judiciary.gov - PH)Document10 pages2018 Politcial and International Law Bar Exam Questions (From SC - Judiciary.gov - PH)Ernest Talingdan CastroPas encore d'évaluation

- Labor Relations List of CasesDocument3 pagesLabor Relations List of CasesErnest Talingdan CastroPas encore d'évaluation

- Commrev Ipl and Transpo LecturesDocument12 pagesCommrev Ipl and Transpo LecturesErnest Talingdan CastroPas encore d'évaluation

- Doctrine of Separate Personality and Piercing Corporate VeilDocument10 pagesDoctrine of Separate Personality and Piercing Corporate VeilErnest Talingdan Castro100% (2)

- Annual Taxable Income 2018 2023 ONWARDSDocument4 pagesAnnual Taxable Income 2018 2023 ONWARDSErnest Talingdan CastroPas encore d'évaluation

- Insurance Case DigestDocument3 pagesInsurance Case DigestErnest Talingdan CastroPas encore d'évaluation

- 2014-2016 Merc QuestionsDocument37 pages2014-2016 Merc QuestionsErnest Talingdan CastroPas encore d'évaluation

- New Applicants MaleDocument4 pagesNew Applicants MaleErnest Talingdan CastroPas encore d'évaluation

- New ApplicantsDocument6 pagesNew ApplicantsRon Jesus VillacampaPas encore d'évaluation

- Doctrine of Separate Personality and Piercing Corporate VeilDocument10 pagesDoctrine of Separate Personality and Piercing Corporate VeilErnest Talingdan Castro100% (2)

- Additional Cases in Insurance LawDocument1 pageAdditional Cases in Insurance LawErnest Talingdan CastroPas encore d'évaluation

- 2017 Ethics Syllabus Compared PDFDocument4 pages2017 Ethics Syllabus Compared PDFCharm FerrerPas encore d'évaluation

- Poli 2017Document12 pagesPoli 2017BrunxAlabastroPas encore d'évaluation

- Great PacificDocument1 pageGreat PacificErnest Talingdan CastroPas encore d'évaluation

- Malayan Case DigestDocument2 pagesMalayan Case DigestErnest Talingdan CastroPas encore d'évaluation

- 02 Labor Law Syllabus 2018 PDFDocument6 pages02 Labor Law Syllabus 2018 PDFRobert WeightPas encore d'évaluation

- Mercantile Law Syllabus 2018 PDFDocument16 pagesMercantile Law Syllabus 2018 PDFjanezahrenPas encore d'évaluation

- Poli 2017Document12 pagesPoli 2017BrunxAlabastroPas encore d'évaluation

- Civil Law SyllabusDocument8 pagesCivil Law SyllabusElmo DecedaPas encore d'évaluation

- 2017 Ethics Syllabus Compared PDFDocument4 pages2017 Ethics Syllabus Compared PDFCharm FerrerPas encore d'évaluation

- 06 Criminal Law Syllabus 2018 PDFDocument4 pages06 Criminal Law Syllabus 2018 PDFErnest Talingdan CastroPas encore d'évaluation

- 02 Labor Law Syllabus 2018 PDFDocument6 pages02 Labor Law Syllabus 2018 PDFRobert WeightPas encore d'évaluation

- 06 Criminal Law Syllabus 2018 PDFDocument4 pages06 Criminal Law Syllabus 2018 PDFErnest Talingdan CastroPas encore d'évaluation

- Mercantile Law Syllabus 2018 PDFDocument16 pagesMercantile Law Syllabus 2018 PDFjanezahrenPas encore d'évaluation

- Commercial Law Review - Atty. Ceniza - Corporation Law Cases - #megenern1Document10 pagesCommercial Law Review - Atty. Ceniza - Corporation Law Cases - #megenern1Ernest Talingdan CastroPas encore d'évaluation

- Civil Law SyllabusDocument8 pagesCivil Law SyllabusElmo DecedaPas encore d'évaluation

- Rule 58 Preliminary Injunction: Section 3: Grounds For The Issuance of Preliminary InjunctionDocument12 pagesRule 58 Preliminary Injunction: Section 3: Grounds For The Issuance of Preliminary InjunctionErnest Talingdan CastroPas encore d'évaluation

- 2017 Bar Syllabus Mercantile LawDocument15 pages2017 Bar Syllabus Mercantile LawErnest Talingdan CastroPas encore d'évaluation

- Meetings of Directors or Trustees, Stockholders orDocument9 pagesMeetings of Directors or Trustees, Stockholders orAmie Jane MirandaPas encore d'évaluation

- Trump Religious Exemption ProposalDocument46 pagesTrump Religious Exemption ProposalLaw&CrimePas encore d'évaluation

- Ra 876Document5 pagesRa 876Dandy CruzPas encore d'évaluation

- TITLE 3: Article 134-142: Criminal Law II Review Notes - Revised Penal CodeDocument10 pagesTITLE 3: Article 134-142: Criminal Law II Review Notes - Revised Penal CodeAizaFerrerEbina100% (14)

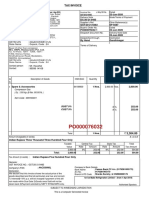

- Tax Invoice: Ice Make Refrigeration Limited - (From 1-Apr-2019)Document1 pageTax Invoice: Ice Make Refrigeration Limited - (From 1-Apr-2019)Sunil PatelPas encore d'évaluation

- 02 Perena v. ZarateDocument8 pages02 Perena v. ZaratePaolo Enrino PascualPas encore d'évaluation

- Lake County Sex Offender StatementDocument1 pageLake County Sex Offender StatementNewsNation DigitalPas encore d'évaluation

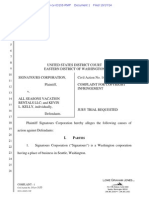

- 2.01 Signatours Corporation V All Seasons Vacation Rentals LLC ComplaintDocument6 pages2.01 Signatours Corporation V All Seasons Vacation Rentals LLC ComplaintCopyright Anti-Bullying Act (CABA Law)Pas encore d'évaluation

- Memorial For Respondent PDFDocument14 pagesMemorial For Respondent PDFshambhavi sinhaPas encore d'évaluation

- Professor Paula Giliker Vicarious Liability in The UK Supreme Court 2016 7 The UK Supreme Court Yearbook 152Document16 pagesProfessor Paula Giliker Vicarious Liability in The UK Supreme Court 2016 7 The UK Supreme Court Yearbook 152LouisChinPas encore d'évaluation

- Raghu Nayjas PDFDocument2 pagesRaghu Nayjas PDFManish R ShankarPas encore d'évaluation

- Pre Trial BriefDocument4 pagesPre Trial BriefAikee Varona Full100% (1)

- Tan Jua Sia vs. Yu Biao: For Digest: Negotiable Instruments By: Nicolas D. Aranilla, JRDocument4 pagesTan Jua Sia vs. Yu Biao: For Digest: Negotiable Instruments By: Nicolas D. Aranilla, JRNick AranillaPas encore d'évaluation

- Berbano Vs Barcelona (2003)Document9 pagesBerbano Vs Barcelona (2003)sjbloraPas encore d'évaluation

- Thayer Background Brief U.S. FONOPS, Vietnam and The South China SeaDocument2 pagesThayer Background Brief U.S. FONOPS, Vietnam and The South China SeaCarlyle Alan ThayerPas encore d'évaluation

- Alavado v. City Government of TaclobanDocument1 pageAlavado v. City Government of TaclobanJAMPas encore d'évaluation

- Boadu Corporate IdentityDocument13 pagesBoadu Corporate Identityatmoggy2003Pas encore d'évaluation

- Petition For NaturalizationDocument4 pagesPetition For NaturalizationbertspamintuanPas encore d'évaluation

- Siddharth Vishwakarma P 1.0Document17 pagesSiddharth Vishwakarma P 1.0siddharthPas encore d'évaluation

- Service Contract Agreement TemplateDocument3 pagesService Contract Agreement Templateanon_84814261675% (4)

- Persons and Family Law NotesDocument10 pagesPersons and Family Law NotesMaria Dana BrillantesPas encore d'évaluation

- DMLCIIDocument2 pagesDMLCIIVu Tung LinhPas encore d'évaluation

- Income Tax Rules for Estates and TrustsDocument2 pagesIncome Tax Rules for Estates and Trustsfrostysimbamagi meowPas encore d'évaluation

- CAPITALIZATION RULESDocument22 pagesCAPITALIZATION RULESIsabella Lin100% (3)

- THEORIESDocument15 pagesTHEORIES123Pas encore d'évaluation

- Bautista V Auto Plus TradersDocument8 pagesBautista V Auto Plus TradersMarrianne ReginaldoPas encore d'évaluation

- Certificate of Candidacy For Provincial Governor: Commission On ElectionsDocument2 pagesCertificate of Candidacy For Provincial Governor: Commission On ElectionsFlorence HibionadaPas encore d'évaluation

- Tedesco DepositionDocument115 pagesTedesco Depositionjfranco17410Pas encore d'évaluation

- Self Defense Rejected in Fatal Shooting CaseDocument2 pagesSelf Defense Rejected in Fatal Shooting Caseron dominic dagumPas encore d'évaluation

- The Age of Periclesbring Blue Book Page - Work OnDocument8 pagesThe Age of Periclesbring Blue Book Page - Work Onapi-26171952Pas encore d'évaluation