Vous aimerez peut-être aussi

- MAIN For Information SanbedaDocument129 pagesMAIN For Information SanbedaDesmond WilliamsPas encore d'évaluation

- FINI619 Internship Report MCBDocument56 pagesFINI619 Internship Report MCBAnsar UllahPas encore d'évaluation

- Qualified Audit ReportsDocument4 pagesQualified Audit ReportsHafinizam Nor AzmiPas encore d'évaluation

- Principles of Marketing - MGT301 Power Point Slides Lecture 7Document32 pagesPrinciples of Marketing - MGT301 Power Point Slides Lecture 7HaileabmarketingPas encore d'évaluation

- Assignment Strategic ManagementDocument5 pagesAssignment Strategic Managementmahbubroyal1555Pas encore d'évaluation

- SWOT Analysis: Singapore Airlines Use of Competitive Advantage For Growth (2018)Document3 pagesSWOT Analysis: Singapore Airlines Use of Competitive Advantage For Growth (2018)ashPas encore d'évaluation

- VIRTUSADocument6 pagesVIRTUSAVaibhav Chauhan100% (1)

- Dire Dawa University: College of Business and Economic Department of ManagementDocument20 pagesDire Dawa University: College of Business and Economic Department of ManagementEng-Mukhtaar CatooshPas encore d'évaluation

- Project Financial Appraisal - NumericalsDocument5 pagesProject Financial Appraisal - NumericalsAbhishek KarekarPas encore d'évaluation

- APM - Strategic Planning and Control: Rational Model / Mission / MendelowDocument3 pagesAPM - Strategic Planning and Control: Rational Model / Mission / Mendelowtaxathon thanePas encore d'évaluation

- Accounting For ManagersDocument224 pagesAccounting For Managershabtamu100% (1)

- Mba in HR M Course ContentDocument19 pagesMba in HR M Course ContentmgajenPas encore d'évaluation

- Space Matrix SampleDocument3 pagesSpace Matrix SampleAngelicaBernardoPas encore d'évaluation

- Project Proposal: Akhuwat's Business Model: Fighting Poverty With Interest-Free MicrofinanceDocument7 pagesProject Proposal: Akhuwat's Business Model: Fighting Poverty With Interest-Free MicrofinanceTaiba e ShaheenPas encore d'évaluation

- Role of Financial Institutions in PakistanDocument5 pagesRole of Financial Institutions in PakistanshurahbeelPas encore d'évaluation

- FinancialManagement MB013 QuestionDocument31 pagesFinancialManagement MB013 QuestionAiDLo50% (2)

- Rift Valley University Harar Campus Masters of Business Administration (MBA) Thesis Title Submitted By: Bedri MuktarDocument1 pageRift Valley University Harar Campus Masters of Business Administration (MBA) Thesis Title Submitted By: Bedri MuktarBedri M AhmeduPas encore d'évaluation

- BCG and Market ShareDocument3 pagesBCG and Market Sharesuccessor88100% (2)

- Demand EstimationDocument18 pagesDemand EstimationVital TejaPas encore d'évaluation

- What Is The SPACE Matrix Strategic Management Method?Document20 pagesWhat Is The SPACE Matrix Strategic Management Method?Waseem Mateen100% (1)

- Chapter Five The Nature of Strategy Analysis and ChoiceDocument10 pagesChapter Five The Nature of Strategy Analysis and ChoiceBedri M AhmeduPas encore d'évaluation

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument24 pagesInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownAarushi SharmaPas encore d'évaluation

- Write Up Zakaria SirDocument14 pagesWrite Up Zakaria Sirdinar aimcPas encore d'évaluation

- Allied Bank Limited: Strategic Management Case StudyDocument72 pagesAllied Bank Limited: Strategic Management Case StudySumAir KhanPas encore d'évaluation

- Project On Scope of Rural Marketing For Consumer Goods0Document121 pagesProject On Scope of Rural Marketing For Consumer Goods0madhur_geetikaPas encore d'évaluation

- FM Sheet 4 (JUHI RAJWANI)Document8 pagesFM Sheet 4 (JUHI RAJWANI)Mukesh SinghPas encore d'évaluation

- The Anatomy of Marketing Positioning StrategyDocument5 pagesThe Anatomy of Marketing Positioning Strategyapi-3753771Pas encore d'évaluation

- Final Project FertilizersDocument44 pagesFinal Project FertilizersFatmahmlkPas encore d'évaluation

- Market Segmentation of Askari BankDocument16 pagesMarket Segmentation of Askari BankOmair0% (1)

- Study of Ibrahim Group of CompaniesDocument29 pagesStudy of Ibrahim Group of CompaniescfmbaimsPas encore d'évaluation

- Gul Ahmed Annual Report 2007Document73 pagesGul Ahmed Annual Report 2007AISHASABAHATPas encore d'évaluation

- Zong-Project (Repaired)Document49 pagesZong-Project (Repaired)maria saleem100% (1)

- Mini Case StudiesDocument22 pagesMini Case StudiesAhsan RanaPas encore d'évaluation

- Muhammad Qaiser HBL ReportDocument21 pagesMuhammad Qaiser HBL Reportm qaiserPas encore d'évaluation

- Política FiscalDocument356 pagesPolítica FiscalAnuar AncheliaPas encore d'évaluation

- Ratio Analysis of Pakistan State Oil and SHELL PakistanDocument5 pagesRatio Analysis of Pakistan State Oil and SHELL PakistanKamran Ali AnsariPas encore d'évaluation

- Strategic ManagementDocument4 pagesStrategic ManagementA CPas encore d'évaluation

- Product Strategy of MobilinkDocument15 pagesProduct Strategy of Mobilinkzafran malikPas encore d'évaluation

- A Sample Case Study On Contemporary Issue by Global Assignment HelpDocument21 pagesA Sample Case Study On Contemporary Issue by Global Assignment HelpInstant Essay WritingPas encore d'évaluation

- International BusinessDocument51 pagesInternational BusinessDARSHAN CHAVANPas encore d'évaluation

- Iprofile - Time Warner Sample ProfileDocument49 pagesIprofile - Time Warner Sample ProfilegssinfotechPas encore d'évaluation

- Floor Plan KTVDocument1 pageFloor Plan KTVBrylle De GuzmanPas encore d'évaluation

- International BankingDocument37 pagesInternational Bankingvikas.kr.02100% (1)

- Department Ofmanagement StudiesDocument10 pagesDepartment Ofmanagement StudiesHarihara PuthiranPas encore d'évaluation

- Supply Chain Management - Mba Lecture Notes PresenrtationDocument64 pagesSupply Chain Management - Mba Lecture Notes PresenrtationAlper Orhun KilicPas encore d'évaluation

- Internship Report (Saman Kayani)Document38 pagesInternship Report (Saman Kayani)Mani ButtPas encore d'évaluation

- Marketing Plan Part I Executive SummaryDocument15 pagesMarketing Plan Part I Executive SummaryMae TomeldenPas encore d'évaluation

- Financial Reporting Final ProjectDocument7 pagesFinancial Reporting Final ProjectMehwish ButtPas encore d'évaluation

- Outline of StramaDocument6 pagesOutline of StramaTrish BustamantePas encore d'évaluation

- Marstrat Sesi 4Document5 pagesMarstrat Sesi 4BUNGA DENINAPas encore d'évaluation

- B4U GLOBAL Group of Companies (PDF) - 1Document40 pagesB4U GLOBAL Group of Companies (PDF) - 1عبدالسبحان بھمبھانیPas encore d'évaluation

- Chapter - 8 Management of ReceivablesDocument6 pagesChapter - 8 Management of ReceivablesadhishcaPas encore d'évaluation

- Fin621 Midterm Short Notes by Maha ShahDocument10 pagesFin621 Midterm Short Notes by Maha ShahRamzan100% (1)

- Project On Parag MilkDocument74 pagesProject On Parag MilkraisPas encore d'évaluation

- Winter Internship Program: Industry Analysis To Cater The Clients' Requirements For M&A, PE/VC Fund RaisingDocument31 pagesWinter Internship Program: Industry Analysis To Cater The Clients' Requirements For M&A, PE/VC Fund RaisingAVINASH JHAPas encore d'évaluation

- University of Gondar College of Business and Economics Department of Marketing ManagementDocument14 pagesUniversity of Gondar College of Business and Economics Department of Marketing ManagementMartha GetanehPas encore d'évaluation

- Islamic Banking Brochure 2019 Jul 19Document10 pagesIslamic Banking Brochure 2019 Jul 19MrMochtarPas encore d'évaluation

- Executive - AnswersDocument53 pagesExecutive - AnswersRakesh KushwahaPas encore d'évaluation

- Rural Banking in IndiaDocument2 pagesRural Banking in IndiaAmit SinhaPas encore d'évaluation

- Retail Banking Transformation Story Post Liberalized IndiaDocument41 pagesRetail Banking Transformation Story Post Liberalized IndiaPallavi Pallu80% (5)

- Human Resource Management ProjectDocument10 pagesHuman Resource Management ProjectNida ShahzadPas encore d'évaluation

- Assigment of RetailDocument9 pagesAssigment of RetailSubhani Khan33% (6)

- Demand Forecasting: Production and Operations ManagementDocument45 pagesDemand Forecasting: Production and Operations ManagementNida ShahzadPas encore d'évaluation

- Sales Management: Sales-Is Activity Related To Selling or The Amount of Goods or Services Sold in A GivenDocument12 pagesSales Management: Sales-Is Activity Related To Selling or The Amount of Goods or Services Sold in A GivenNida ShahzadPas encore d'évaluation

- Human Resource Management ProjectDocument10 pagesHuman Resource Management ProjectNida ShahzadPas encore d'évaluation

- Deloitte Cost OptimizationDocument32 pagesDeloitte Cost OptimizationVik DixPas encore d'évaluation

- Week 5 AssignmentDocument1 pageWeek 5 AssignmentSushmita Shivaram100% (1)

- SWDocument1 pageSWAnne BustilloPas encore d'évaluation

- Group 5 Mittal CaseDocument9 pagesGroup 5 Mittal CaseaaidanrathiPas encore d'évaluation

- Audit Internship Report Nida DKDocument28 pagesAudit Internship Report Nida DKShan Ali ShahPas encore d'évaluation

- Financial Markets and Services: Ishika Manisha JyotiDocument17 pagesFinancial Markets and Services: Ishika Manisha JyotiIshika GargPas encore d'évaluation

- Methods of Software AcquisitionDocument12 pagesMethods of Software AcquisitionSimranjeet Singh100% (4)

- WEEK 4 - Topic Overview - CN7021Document20 pagesWEEK 4 - Topic Overview - CN7021RowaPas encore d'évaluation

- Corporate Governance Government MeasuresDocument9 pagesCorporate Governance Government MeasurestawandaPas encore d'évaluation

- SBIR Program OverviewDocument13 pagesSBIR Program OverviewFernie1Pas encore d'évaluation

- Entry Strategies: Exporting Contractual Entry Modes Foreign Direct Investment (Document10 pagesEntry Strategies: Exporting Contractual Entry Modes Foreign Direct Investment (DianaProEraPas encore d'évaluation

- Introduction To Industrial Relations - Chapter IDocument9 pagesIntroduction To Industrial Relations - Chapter IKamal KatariaPas encore d'évaluation

- Service MarketingDocument21 pagesService MarketingKunwar AdityaPas encore d'évaluation

- Senior Project Engineering Manager in Chicago IL Resume Richard PrischingDocument2 pagesSenior Project Engineering Manager in Chicago IL Resume Richard PrischingRichardPrischingPas encore d'évaluation

- Activity 1:: Date Account Titles and Explanation P.R. Debit CreditDocument3 pagesActivity 1:: Date Account Titles and Explanation P.R. Debit Creditemem resuentoPas encore d'évaluation

- Job Vacancies in PPB GroupDocument10 pagesJob Vacancies in PPB GroupFarin MustafaPas encore d'évaluation

- BUS 5411 - Written Assignment Week 4Document2 pagesBUS 5411 - Written Assignment Week 4Yared AdanePas encore d'évaluation

- Business EthicsDocument11 pagesBusiness EthicsMD Saiful IslamPas encore d'évaluation

- PWC Global Investor Survey 2022Document6 pagesPWC Global Investor Survey 2022Khaled IbrahimPas encore d'évaluation

- Lukoil A-Vertically Integrated Oil CompanyDocument20 pagesLukoil A-Vertically Integrated Oil CompanyhuccennPas encore d'évaluation

- Economic Environment of Business Mini ProjectDocument19 pagesEconomic Environment of Business Mini Projectpankajkapse67% (3)

- The Systems Development Environment: True-False QuestionsDocument262 pagesThe Systems Development Environment: True-False Questionslouisa_wanPas encore d'évaluation

- Wepik Ethics in Business Navigating Challenges and Implementing Solutions 20230707055224HMaODocument8 pagesWepik Ethics in Business Navigating Challenges and Implementing Solutions 20230707055224HMaOSakthiPas encore d'évaluation

- Sub Contract AgreementDocument15 pagesSub Contract AgreementJenifer Londeka NgcoboPas encore d'évaluation

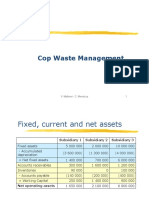

- Cop Waste Management SolutionDocument5 pagesCop Waste Management SolutionPaul GhanimehPas encore d'évaluation

- A. Find The Values of The Missing Variables, Which Are Defined As FollowsDocument3 pagesA. Find The Values of The Missing Variables, Which Are Defined As FollowsHermione Eyer - TanPas encore d'évaluation

- Alphasol International Group Profile: Tel: +251 114 701858 Fax: +251 114 702358 Mobile +251 920745948, EmailDocument16 pagesAlphasol International Group Profile: Tel: +251 114 701858 Fax: +251 114 702358 Mobile +251 920745948, EmailsachinoilPas encore d'évaluation

- Nestle GlobalizationDocument30 pagesNestle GlobalizationDaryll Peter Griffith60% (5)

- Unit 1Document38 pagesUnit 1Varsha SinghPas encore d'évaluation

- TESCO - Forum Assignment Marketing ManagementDocument7 pagesTESCO - Forum Assignment Marketing ManagementAnanthi Balu100% (1)