Vous aimerez peut-être aussi

- Indiabulls PILDocument64 pagesIndiabulls PILPGurus100% (1)

- Company Analysis: Hindustan Uniliver LTDDocument21 pagesCompany Analysis: Hindustan Uniliver LTDmaximus077Pas encore d'évaluation

- F&B ReportDocument52 pagesF&B ReportTulika BansalPas encore d'évaluation

- Plant Management TafskillsDocument4 pagesPlant Management TafskillsTHEOPHILUS ATO FLETCHERPas encore d'évaluation

- Retail Leadership Summit 2014: Emerging Consumer Segments in IndiaDocument55 pagesRetail Leadership Summit 2014: Emerging Consumer Segments in IndiarramprabhakarPas encore d'évaluation

- Itc Final ProjectDocument22 pagesItc Final ProjectSrijan Kumar MaitiPas encore d'évaluation

- Fast Moving Consumer Goods Sector Analysis Report: FMCG CompaniesDocument33 pagesFast Moving Consumer Goods Sector Analysis Report: FMCG CompaniesADITYA RANJANPas encore d'évaluation

- Personal Care Which Accounts For 50%, Healthcare Which Accounts For 31%Document16 pagesPersonal Care Which Accounts For 50%, Healthcare Which Accounts For 31%ADITYA RANJANPas encore d'évaluation

- Business Enviornment (KMB 201) : Imapct of Budget 2019 On GroupDocument21 pagesBusiness Enviornment (KMB 201) : Imapct of Budget 2019 On GroupManmohan SaxenaPas encore d'évaluation

- Strategy Maruti SuzukiDocument30 pagesStrategy Maruti SuzukiAjith SankaranPas encore d'évaluation

- FMCG SectorDocument37 pagesFMCG SectorJafar SibtainPas encore d'évaluation

- Industry Analysis NestleDocument20 pagesIndustry Analysis NestleSurendra BabuPas encore d'évaluation

- Fast Moving Consumer Goods (FMCG) : Sector ReportDocument12 pagesFast Moving Consumer Goods (FMCG) : Sector ReportRajat GuptaPas encore d'évaluation

- Retail Sector in IndiaDocument62 pagesRetail Sector in Indiapurval16110% (1)

- FMCG Sector Ppt.97-2003Document29 pagesFMCG Sector Ppt.97-2003Sourav SahaPas encore d'évaluation

- Quiz - Fintech, FMCG, ECommerceDocument341 pagesQuiz - Fintech, FMCG, ECommerceShomyo RoyPas encore d'évaluation

- Retail Transformation: Changing Your Performance Trajectory: CII National Retail Summit: 2016Document60 pagesRetail Transformation: Changing Your Performance Trajectory: CII National Retail Summit: 2016Durant DsouzaPas encore d'évaluation

- FMCG Sector - A Brief Analysis by Porter's 5 Fcactor ModelDocument17 pagesFMCG Sector - A Brief Analysis by Porter's 5 Fcactor ModelAMARTYA GHOSHPas encore d'évaluation

- FMCG Report May 20181Document32 pagesFMCG Report May 20181work mainPas encore d'évaluation

- CG199090 The Wine Park WineDocument12 pagesCG199090 The Wine Park WineDipanwitaPas encore d'évaluation

- Marketing Plan For IKEA IndiaDocument21 pagesMarketing Plan For IKEA IndiaHetPas encore d'évaluation

- Critical Analysis of Indian FMCG SectorDocument23 pagesCritical Analysis of Indian FMCG Sectordevenm89Pas encore d'évaluation

- FMCG - HulDocument29 pagesFMCG - HulRachna khuranaPas encore d'évaluation

- Product Management PraveenDocument12 pagesProduct Management Praveenash.rulzPas encore d'évaluation

- Fast-Moving Consumer Goods (FMCG) / Consumer Packaged Goods (CPG) : Products That Are Sold Quickly and at Relatively Low CostDocument5 pagesFast-Moving Consumer Goods (FMCG) / Consumer Packaged Goods (CPG) : Products That Are Sold Quickly and at Relatively Low CostYogesh Kumar DasPas encore d'évaluation

- Ifim Bussines School Bangalore: A ON Customer and Product Analysis of Panasonic India LCD, Led &plasmaDocument17 pagesIfim Bussines School Bangalore: A ON Customer and Product Analysis of Panasonic India LCD, Led &plasmaVinod Kumar100% (1)

- Chanda Kochhar SlidesDocument28 pagesChanda Kochhar SlidesPrabha IyerPas encore d'évaluation

- Finlatics Investment Banking Experience Program Project 2: Sustainable Fashion CompanyDocument5 pagesFinlatics Investment Banking Experience Program Project 2: Sustainable Fashion CompanyAKSHAY GHADGEPas encore d'évaluation

- A JST Investments Publication Reach Us HereDocument48 pagesA JST Investments Publication Reach Us HerejayPas encore d'évaluation

- SYNOPSISDocument21 pagesSYNOPSISSheeba khamPas encore d'évaluation

- Two Wheelers - Dealer Survey ReportDocument8 pagesTwo Wheelers - Dealer Survey Reportticktick100% (3)

- ADTimes 2020 ABFRLDocument9 pagesADTimes 2020 ABFRLgargshashankPas encore d'évaluation

- FMCG Industry - OutlineDocument5 pagesFMCG Industry - Outlineapi-3712367100% (1)

- Retail FormatsDocument24 pagesRetail FormatsHari__cabm100% (3)

- Agri RetailDocument19 pagesAgri RetailPrathap G MPas encore d'évaluation

- India: Retail & Consumer Arvind SinghalDocument14 pagesIndia: Retail & Consumer Arvind SinghalsreecegPas encore d'évaluation

- Vishruti Khandelwal PGDM - 1. 2019-1705-0001-0033Document17 pagesVishruti Khandelwal PGDM - 1. 2019-1705-0001-0033Vishruti KhandelwalPas encore d'évaluation

- Manthan Report - Retail SectorDocument23 pagesManthan Report - Retail SectorAtul sharmaPas encore d'évaluation

- Document Internship SweetyDocument26 pagesDocument Internship Sweetyom Prakash ReddyPas encore d'évaluation

- Micro Small and Medium Enterprise SectorDocument30 pagesMicro Small and Medium Enterprise SectorVitthal BhavsarPas encore d'évaluation

- The Great Indian ConsumerDocument65 pagesThe Great Indian Consumerjaikishanmakhija3763Pas encore d'évaluation

- OTP Presentation Non Editable - Brief 1Document17 pagesOTP Presentation Non Editable - Brief 1chinnaPas encore d'évaluation

- Group 1 - FRA Assignment - FinalDocument33 pagesGroup 1 - FRA Assignment - FinalGaurav KeswaniPas encore d'évaluation

- Kotak Mahindra StrategyDocument34 pagesKotak Mahindra StrategyShaddab AliPas encore d'évaluation

- DGT Group Project PPT - Group 10Document30 pagesDGT Group Project PPT - Group 10ayushi biswasPas encore d'évaluation

- Fast Moving Consumer Goods (FMCG) : June 2020Document30 pagesFast Moving Consumer Goods (FMCG) : June 2020Jasleen kaurPas encore d'évaluation

- Fast Moving Consumer Goods (FMCG) : March 2020Document31 pagesFast Moving Consumer Goods (FMCG) : March 2020Sourajit Biswas100% (1)

- Asianpaintppt 191211182449Document19 pagesAsianpaintppt 191211182449Meena MalchePas encore d'évaluation

- Consumer Durables April 2017Document45 pagesConsumer Durables April 2017Mayank SinghaniaPas encore d'évaluation

- Consumer Durables April 2017Document45 pagesConsumer Durables April 2017RASLEEN KAURPas encore d'évaluation

- Himalayan Package Drinking WaterDocument34 pagesHimalayan Package Drinking WaterSheikh Zain UddinPas encore d'évaluation

- Going For Gold by Creating Customers Who Create Customers BCGDocument60 pagesGoing For Gold by Creating Customers Who Create Customers BCGLucky TalwarPas encore d'évaluation

- FMCG August 2020Document30 pagesFMCG August 2020saty16Pas encore d'évaluation

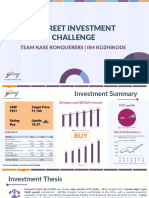

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainPas encore d'évaluation

- Retail in India: Towards Growth and ProfitabilityDocument23 pagesRetail in India: Towards Growth and ProfitabilityGaurav RathaurPas encore d'évaluation

- 1.1 Introduction To Retail in India: Today, The Flood of Products in The Market Coupled With A Wealthier, More InformedDocument52 pages1.1 Introduction To Retail in India: Today, The Flood of Products in The Market Coupled With A Wealthier, More InformedNamrata LakhotiaPas encore d'évaluation

- Vijaysales by Ketan ChauhanDocument60 pagesVijaysales by Ketan ChauhanKetan ChauhanPas encore d'évaluation

- Superkart: Agnerovera Round 3 SubmissionDocument14 pagesSuperkart: Agnerovera Round 3 SubmissionSALONI GOYALPas encore d'évaluation

- "Britannia Fundamental and Technical Analysis": Group-2Document27 pages"Britannia Fundamental and Technical Analysis": Group-2Vedantam GuptaPas encore d'évaluation

- Presentation On Food & Grocery Sector in India: by Arijit Ghosh, Saikat Biswas, Bidyut Mondal & Rounak BasuDocument20 pagesPresentation On Food & Grocery Sector in India: by Arijit Ghosh, Saikat Biswas, Bidyut Mondal & Rounak BasuRedback NationPas encore d'évaluation

- Aid for Trade in Asia and the Pacific: Promoting Economic Diversification and EmpowermentD'EverandAid for Trade in Asia and the Pacific: Promoting Economic Diversification and EmpowermentPas encore d'évaluation

- 2017 International Comparison Program for Asia and the Pacific: Purchasing Power Parities and Real Expenditures—Results and MethodologyD'Everand2017 International Comparison Program for Asia and the Pacific: Purchasing Power Parities and Real Expenditures—Results and MethodologyPas encore d'évaluation

- Cbjessco 13Document3 pagesCbjessco 13Fawaz ZaheerPas encore d'évaluation

- RFP For Corporate Engagement Platform PDFDocument28 pagesRFP For Corporate Engagement Platform PDFAnupriya Roy ChoudharyPas encore d'évaluation

- Best of Thekkady (Periyar) Recommended by Indian Travellers: Created Date: 27 December 2015Document8 pagesBest of Thekkady (Periyar) Recommended by Indian Travellers: Created Date: 27 December 2015sk_kannan26Pas encore d'évaluation

- Soal Dan Jawaban Audit IIDocument22 pagesSoal Dan Jawaban Audit IIsantaulinasitorusPas encore d'évaluation

- 5 GR No. 93468 December 29, 1994 NATU Vs TorresDocument9 pages5 GR No. 93468 December 29, 1994 NATU Vs Torresrodolfoverdidajr100% (1)

- 2022 Significant FEHB Plan ChangesDocument12 pages2022 Significant FEHB Plan ChangesFedSmith Inc.Pas encore d'évaluation

- Best Evidence Rule CasesDocument5 pagesBest Evidence Rule CasesRemy Rose AlegrePas encore d'évaluation

- 201805graphene PDFDocument204 pages201805graphene PDFMohammad RezkyPas encore d'évaluation

- Asmsc 1119 PDFDocument9 pagesAsmsc 1119 PDFAstha WadhwaPas encore d'évaluation

- Apayao Quickstat: Indicator Reference Period and DataDocument4 pagesApayao Quickstat: Indicator Reference Period and DataLiyan CampomanesPas encore d'évaluation

- DLL Sci 10 12-09-2022Document3 pagesDLL Sci 10 12-09-2022Lovely Shiena Cain AragoncilloPas encore d'évaluation

- Activity 2.1 Test Your Food Safety IQDocument3 pagesActivity 2.1 Test Your Food Safety IQAustin PricePas encore d'évaluation

- Garden Profile NDocument19 pagesGarden Profile NParitosh VermaPas encore d'évaluation

- Operating Instruction PMD55Document218 pagesOperating Instruction PMD55Dilip ARPas encore d'évaluation

- Firearm Laws in PennsylvaniaDocument2 pagesFirearm Laws in PennsylvaniaJesse WhitePas encore d'évaluation

- W01 358 7304Document29 pagesW01 358 7304MROstop.comPas encore d'évaluation

- Queue Using Linked ListDocument2 pagesQueue Using Linked ListHassan ZiaPas encore d'évaluation

- Welcome To Our Presentation: Submitted byDocument30 pagesWelcome To Our Presentation: Submitted byShamim MridhaPas encore d'évaluation

- Appointments & Other Personnel Actions Submission, Approval/Disapproval of AppointmentDocument7 pagesAppointments & Other Personnel Actions Submission, Approval/Disapproval of AppointmentZiiee BudionganPas encore d'évaluation

- UTAR Convocation Checklist For Graduands Attending Convocation (March 2019) - 1Document5 pagesUTAR Convocation Checklist For Graduands Attending Convocation (March 2019) - 1JoyleeeeePas encore d'évaluation

- FATCA W9 + Carta para Compartir Información (FATCA)Document2 pagesFATCA W9 + Carta para Compartir Información (FATCA)CarrilloyLawPas encore d'évaluation

- Introduction To MAX InternationalDocument48 pagesIntroduction To MAX InternationalDanieldoePas encore d'évaluation

- Ashik KP - Windows Engineer - 6 00 - Yrs - Bangalore LocationDocument4 pagesAshik KP - Windows Engineer - 6 00 - Yrs - Bangalore LocationmanitejaPas encore d'évaluation

- El Condor1 Reporte ECP 070506Document2 pagesEl Condor1 Reporte ECP 070506pechan07Pas encore d'évaluation

- Dahua Network Speed Dome & PTZ Camera Web3.0 Operation ManualDocument164 pagesDahua Network Speed Dome & PTZ Camera Web3.0 Operation ManualNiksayPas encore d'évaluation

- Materi Basic Safety #1Document32 pagesMateri Basic Safety #1Galih indrahutama100% (1)

- Asus P8Z68-V PRO GEN3 ManualDocument146 pagesAsus P8Z68-V PRO GEN3 ManualwkfanPas encore d'évaluation

- Unified HACKTBDocument15 pagesUnified HACKTBKali PentesterPas encore d'évaluation