Vous aimerez peut-être aussi

- Dhan Vriddhi English Sales BrochureDocument16 pagesDhan Vriddhi English Sales BrochureNimesh PrakashPas encore d'évaluation

- 4 InsurTechs Making Insurance Easily Accessible.Document6 pages4 InsurTechs Making Insurance Easily Accessible.Nimesh PrakashPas encore d'évaluation

- 6941 - Tenders For Banker's Indeminity Insurance PolicyDocument20 pages6941 - Tenders For Banker's Indeminity Insurance PolicyNimesh PrakashPas encore d'évaluation

- List of Banks IndiaDocument4 pagesList of Banks IndiaNimesh PrakashPas encore d'évaluation

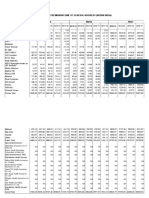

- 50 Segment-Wise Gross Direct Premium of General Insurers Within India1718Document6 pages50 Segment-Wise Gross Direct Premium of General Insurers Within India1718Nimesh PrakashPas encore d'évaluation

- 2015 Rims PresentationSessionICM006v2Document38 pages2015 Rims PresentationSessionICM006v2Nimesh PrakashPas encore d'évaluation

- 6941 - Tenders For Banker's Indeminity Insurance PolicyDocument20 pages6941 - Tenders For Banker's Indeminity Insurance PolicyNimesh PrakashPas encore d'évaluation

- How India Buys InsuranceDocument41 pagesHow India Buys InsuranceNimesh PrakashPas encore d'évaluation

- Questionnaire For LLP ClosureDocument1 pageQuestionnaire For LLP ClosureNimesh PrakashPas encore d'évaluation

- 6941 - Tenders For Banker's Indeminity Insurance PolicyDocument20 pages6941 - Tenders For Banker's Indeminity Insurance PolicyNimesh PrakashPas encore d'évaluation

- Cyber Risk Protector Insurance Proposal Form SummaryDocument6 pagesCyber Risk Protector Insurance Proposal Form SummaryNimesh PrakashPas encore d'évaluation

- Cyber Risk Protector Insurance Proposal Form SummaryDocument6 pagesCyber Risk Protector Insurance Proposal Form SummaryNimesh PrakashPas encore d'évaluation

- Name Headquarters City: Tata Consultancy Services MumbaiDocument13 pagesName Headquarters City: Tata Consultancy Services MumbaiNimesh PrakashPas encore d'évaluation

- CII RPL Application Form GuideDocument2 pagesCII RPL Application Form GuideNimesh Prakash100% (1)

- 65Document37 pages65Nimesh PrakashPas encore d'évaluation

- Book 1Document52 pagesBook 1Nimesh PrakashPas encore d'évaluation

- Feb2018/zip/27543388 TD Fil7Document2 pagesFeb2018/zip/27543388 TD Fil7Nimesh PrakashPas encore d'évaluation

- WctariffDocument127 pagesWctariffNio Kumar100% (1)

- 351 10 06 34 Final Janta Bank Final 1 68 03-08-2017Document68 pages351 10 06 34 Final Janta Bank Final 1 68 03-08-2017Nimesh PrakashPas encore d'évaluation

- Irda Mar08Document52 pagesIrda Mar08Nimesh PrakashPas encore d'évaluation

- QCR - Hosuing Society InsurancDocument2 pagesQCR - Hosuing Society InsurancNimesh PrakashPas encore d'évaluation

- BROCHURE Stockthroughput 2014 EmailDocument6 pagesBROCHURE Stockthroughput 2014 EmailNimesh PrakashPas encore d'évaluation

- Recharge Your Mobile and DTH Services OnlineDocument1 pageRecharge Your Mobile and DTH Services OnlineNimesh PrakashPas encore d'évaluation

- Stock Throughput PoliciesDocument39 pagesStock Throughput PoliciesrajasekharboPas encore d'évaluation

- E-Class Brochure For WEB - Sept 2011Document36 pagesE-Class Brochure For WEB - Sept 2011Nimesh PrakashPas encore d'évaluation

- Hul Casestudy g4 Group12Document14 pagesHul Casestudy g4 Group12Nimesh PrakashPas encore d'évaluation

- J. B. Boda Insurance Brokers Pvt. Ltd. The Ruby, 5th Floor, North West 29, Senapati Bapat Marg, Dadar (West) Mumbai - 400 028 IndiaDocument2 pagesJ. B. Boda Insurance Brokers Pvt. Ltd. The Ruby, 5th Floor, North West 29, Senapati Bapat Marg, Dadar (West) Mumbai - 400 028 IndiaNimesh PrakashPas encore d'évaluation

- E-Class Brochure For WEB - Sept 2011Document36 pagesE-Class Brochure For WEB - Sept 2011Nimesh PrakashPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Claw PPT - ProspectusDocument27 pagesClaw PPT - Prospectusitika DhawanPas encore d'évaluation

- Meezan Bank: Islamic Banking Services and Account TypesDocument41 pagesMeezan Bank: Islamic Banking Services and Account TypesBilal AhmedPas encore d'évaluation

- ALFONSO S. TAN, Petitioner vs. Securities and Exchange Commission G.R. No. 95696 March 3, 1992Document2 pagesALFONSO S. TAN, Petitioner vs. Securities and Exchange Commission G.R. No. 95696 March 3, 1992viviviolettePas encore d'évaluation

- NBF Cicc 302019Document1 134 pagesNBF Cicc 302019Tarun BhandariPas encore d'évaluation

- Core Lbo ModelDocument25 pagesCore Lbo Modelsalman_schonPas encore d'évaluation

- 91 SA Institutional Cautious Managed Fund Factsheet enDocument1 page91 SA Institutional Cautious Managed Fund Factsheet enXola Xhayimpi JwaraPas encore d'évaluation

- Uwrt 1103 - The Speed Traders - DejDocument2 pagesUwrt 1103 - The Speed Traders - Dejapi-403608510Pas encore d'évaluation

- Gross KlussmannDocument131 pagesGross KlussmannMotiram paudelPas encore d'évaluation

- Managerial Accounting Reviewer PreFinalsxDocument10 pagesManagerial Accounting Reviewer PreFinalsxGenelyn BalancarPas encore d'évaluation

- BASIC BOOKKEEPING COMPETENCIES HANDOUTDocument8 pagesBASIC BOOKKEEPING COMPETENCIES HANDOUTraquelPas encore d'évaluation

- CMM Short Dated Calc v2 PDFDocument5 pagesCMM Short Dated Calc v2 PDFtallindianPas encore d'évaluation

- CA Final SFM Compiler Ver 6.0Document452 pagesCA Final SFM Compiler Ver 6.0Accounts Primesoft100% (1)

- Presentation On DerevativeDocument19 pagesPresentation On DerevativeAnkitaParabPas encore d'évaluation

- LESSON 2 - Analyzing Business Transactions Part 1Document3 pagesLESSON 2 - Analyzing Business Transactions Part 1Anna JeramosPas encore d'évaluation

- Stock Broking Firms 2003Document41 pagesStock Broking Firms 2003sudipkudasPas encore d'évaluation

- David Nassar - Day Trading SmartDocument33 pagesDavid Nassar - Day Trading SmartLinneu BuenoPas encore d'évaluation

- Course Schedule and Cases 2-20-2021Document16 pagesCourse Schedule and Cases 2-20-2021Christian Ian LimPas encore d'évaluation

- Himadri Chemical Inv 5 2014 - 2016Document34 pagesHimadri Chemical Inv 5 2014 - 2016Poonam AggarwalPas encore d'évaluation

- Creation of a Leading Indonesian Energy GroupDocument41 pagesCreation of a Leading Indonesian Energy GroupCasual ThingPas encore d'évaluation

- 3.overview of NHAIDocument5 pages3.overview of NHAIBharat Reddy100% (1)

- Assignment AFMDocument13 pagesAssignment AFMKibrom GmichaelPas encore d'évaluation

- Standard Balance Sheet PT Cahaya AdamDocument1 pageStandard Balance Sheet PT Cahaya AdamAdam Al MukhaffiPas encore d'évaluation

- History of Credit Rating AgenciesDocument3 pagesHistory of Credit Rating AgenciesAzhar KhanPas encore d'évaluation

- Annaly Investor PresentationDocument22 pagesAnnaly Investor PresentationFelix PopescuPas encore d'évaluation

- Investment Banking Deal ProcessDocument25 pagesInvestment Banking Deal Processdkgrinder100% (1)

- RED MA Workshop - Key Features of The Sale and Purchase AgreementDocument18 pagesRED MA Workshop - Key Features of The Sale and Purchase AgreementGunupudi Venkata Raghuram100% (1)

- JSW Steel (JSTL In) : Q4FY19 Result UpdateDocument6 pagesJSW Steel (JSTL In) : Q4FY19 Result UpdatePraveen KumarPas encore d'évaluation

- MAF653 TEST 1 NOV 2022 QuestionDocument11 pagesMAF653 TEST 1 NOV 2022 QuestionAyunieazahaPas encore d'évaluation

- Causes and Effects of Demutualization of Financial ExchangesDocument49 pagesCauses and Effects of Demutualization of Financial Exchangesfahd_faux9282Pas encore d'évaluation

- Types of Market TransactionsDocument4 pagesTypes of Market Transactionsvinayjain221100% (2)