Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

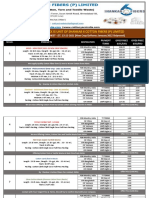

- PT Global Spintex Is Unit of Shankar 6 Cotton Fibers (P) LimitedDocument3 pagesPT Global Spintex Is Unit of Shankar 6 Cotton Fibers (P) LimitedcottontradePas encore d'évaluation

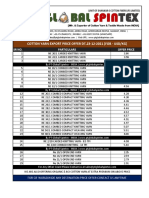

- 23 12 2021 Yarn Export Price OfferDocument1 page23 12 2021 Yarn Export Price OffercottontradePas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- 12-11-2021-Todays Export Price OfferDocument3 pages12-11-2021-Todays Export Price OffercottontradePas encore d'évaluation

- When People Rebel NotesDocument2 pagesWhen People Rebel NotesnutsakalolPas encore d'évaluation

- वाचा आणि आचरणात आणाDocument33 pagesवाचा आणि आचरणात आणाpankajp17Pas encore d'évaluation

- A Detailed Note On The Kashmir Issue Between Pakistan and IndiaDocument3 pagesA Detailed Note On The Kashmir Issue Between Pakistan and IndiaHadia Ahmed KafeelPas encore d'évaluation

- List of Companies of India Wikipedia The Free EncyclopediaDocument17 pagesList of Companies of India Wikipedia The Free Encyclopediaanish18tambePas encore d'évaluation

- Characteristics of the Indian Economy: Poverty, Agriculture Dependence, Low IncomeDocument11 pagesCharacteristics of the Indian Economy: Poverty, Agriculture Dependence, Low IncomeKrish SinghPas encore d'évaluation

- Websiteclassroom PDFDocument2 pagesWebsiteclassroom PDFanuj tattiPas encore d'évaluation

- Subject-Wise Prelims Test Series 2020 - 21: Leave No Stone Unturned Through EBS ApproachDocument58 pagesSubject-Wise Prelims Test Series 2020 - 21: Leave No Stone Unturned Through EBS ApproachSneha PavithranPas encore d'évaluation

- Indian AwardsDocument11 pagesIndian AwardsrajakumarkkrPas encore d'évaluation

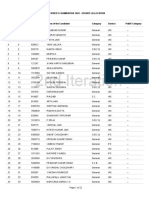

- CIVIL SERVICES EXAMINATION 2020 SERVICE ALLOCATION LISTDocument22 pagesCIVIL SERVICES EXAMINATION 2020 SERVICE ALLOCATION LISTAnkur Anand AgrawalPas encore d'évaluation

- @TeamBookCorner Class 10th Sample Papers @NTSECHATDocument8 pages@TeamBookCorner Class 10th Sample Papers @NTSECHATHameeda PPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Marine Products ExportDocument76 pagesMarine Products Exportpradeepsiib80% (5)

- Leather and Leather GoodsDocument56 pagesLeather and Leather GoodsYogesh SharmaPas encore d'évaluation

- Deccan Proposed SolutionDocument20 pagesDeccan Proposed SolutionAmigos Al CougarPas encore d'évaluation

- Hospital List As On 310713Document44 pagesHospital List As On 310713arbaz khanPas encore d'évaluation

- AS - WB - CB - EVS - V - India-Culture and HeritageDocument6 pagesAS - WB - CB - EVS - V - India-Culture and HeritagePrabha TPas encore d'évaluation

- Asoka The GreatDocument15 pagesAsoka The GreatShashank KulkarniPas encore d'évaluation

- Central Cabinet Ministers of India 2024Document19 pagesCentral Cabinet Ministers of India 2024Raghu Hanasavadi BasavarajappaPas encore d'évaluation

- Work Life Balance in India-IndiaDocument8 pagesWork Life Balance in India-IndiaM Muthukrishnan50% (2)

- NSS IIT Kharagpur Newsletter NSS Day EditionDocument6 pagesNSS IIT Kharagpur Newsletter NSS Day EditionGoutam SahaPas encore d'évaluation

- Test - 5 - Indian Culture - Test-1Document16 pagesTest - 5 - Indian Culture - Test-1Srikanth Harinadh BPas encore d'évaluation

- Downloads - 06072015 - List of Registered Homoeopathy Doctors With Concern Remark Updated Till 01-07-2015 Reg. No - 20001 - 25000 PDFDocument1 389 pagesDownloads - 06072015 - List of Registered Homoeopathy Doctors With Concern Remark Updated Till 01-07-2015 Reg. No - 20001 - 25000 PDFBabu MunkamuthakaPas encore d'évaluation

- Top 5 Historical Sites and MonumentsDocument2 pagesTop 5 Historical Sites and MonumentsVidhi RustagiPas encore d'évaluation

- LeadershipDocument110 pagesLeadershipAshok YadavPas encore d'évaluation

- The Arya Samaj Roots of Atal Bihari VajpayeeDocument2 pagesThe Arya Samaj Roots of Atal Bihari VajpayeeAnurag AryaPas encore d'évaluation

- Class 7 History Chapter 4 The Mughal Empire: Very Short Answers TypeDocument7 pagesClass 7 History Chapter 4 The Mughal Empire: Very Short Answers TypeTHANGAVEL S PPas encore d'évaluation

- Internal Security NCRB ReportDocument8 pagesInternal Security NCRB ReportZeba HasanPas encore d'évaluation

- Pak Affairs One Papers MCQS 16-03-2021Document1 pagePak Affairs One Papers MCQS 16-03-2021Raja NafeesPas encore d'évaluation

- Secunderabad Electric Trades AssociationDocument4 pagesSecunderabad Electric Trades AssociationRishab KumarPas encore d'évaluation

- KGFDocument3 pagesKGFVamsi ReddyPas encore d'évaluation

- Ram Janambhoomi vs. Babri Masjid Dispute ExplainedDocument16 pagesRam Janambhoomi vs. Babri Masjid Dispute ExplainedAnkit AroraPas encore d'évaluation