Vous aimerez peut-être aussi

- 03 Cash and Cash Equivalents (Student)Document27 pages03 Cash and Cash Equivalents (Student)Christina Dulay50% (2)

- Cash and Cash EquivalentsDocument33 pagesCash and Cash EquivalentsJohn kyle Abbago100% (2)

- Activity 1 - Cash and Cash EquivalentsDocument4 pagesActivity 1 - Cash and Cash EquivalentsSean Lester S. NombradoPas encore d'évaluation

- Allan and Irene Answer KeyDocument9 pagesAllan and Irene Answer KeyApril NaidaPas encore d'évaluation

- GROUP Members: Anog, Nove Angel: JMJ Marist Brothers Notre Dame of Dadiangas University Accountancy ProgramDocument2 pagesGROUP Members: Anog, Nove Angel: JMJ Marist Brothers Notre Dame of Dadiangas University Accountancy ProgramArlene GarciaPas encore d'évaluation

- Chapter 11 Answers RepportDocument12 pagesChapter 11 Answers RepportJudy56% (16)

- Problem 1Document8 pagesProblem 1KyleRhayneDiazCaliwagPas encore d'évaluation

- GROUP 6 Problem 3 7 To 3 9Document24 pagesGROUP 6 Problem 3 7 To 3 9Hans ManaliliPas encore d'évaluation

- 33Document2 pages33yes yesnoPas encore d'évaluation

- Martinez, Althea E. Abm 12-1 (Accounting 2)Document13 pagesMartinez, Althea E. Abm 12-1 (Accounting 2)Althea Escarpe MartinezPas encore d'évaluation

- Cash and Cash Equivalents - Problem 1-20Document9 pagesCash and Cash Equivalents - Problem 1-20Eunice PolicarpioPas encore d'évaluation

- Chapter 13-Cash ControlDocument25 pagesChapter 13-Cash ControlShaila MarceloPas encore d'évaluation

- Perida and Rhoda Answer KeyDocument5 pagesPerida and Rhoda Answer KeyApril NaidaPas encore d'évaluation

- AC1Document1 pageAC1Lyanna Mormont25% (4)

- Quiz 1. Conceptual Framework and Accounting Standards: PointsDocument21 pagesQuiz 1. Conceptual Framework and Accounting Standards: PointsMarcus MonocayPas encore d'évaluation

- Assignment AnswerDocument2 pagesAssignment AnswerMims ChiiiPas encore d'évaluation

- Required Ending Allowance For Doubtful AccountsDocument4 pagesRequired Ending Allowance For Doubtful AccountsAngelica SamontePas encore d'évaluation

- Guide To Proof of CashDocument3 pagesGuide To Proof of CashRose Ann Juleth LicayanPas encore d'évaluation

- Cash and Cash EquivalentsDocument7 pagesCash and Cash EquivalentsDianna DayawonPas encore d'évaluation

- Illustration Chapter 1 1Document7 pagesIllustration Chapter 1 1PrincesipiePas encore d'évaluation

- Cash EquivalentDocument9 pagesCash EquivalentMaria G. BernardinoPas encore d'évaluation

- Intermediate AccountingDocument6 pagesIntermediate AccountingMary Angeline LopezPas encore d'évaluation

- Reviewer Controlling Cash Part 1Document6 pagesReviewer Controlling Cash Part 1Mikey Irwin0% (2)

- Quiz VIII - ARDocument3 pagesQuiz VIII - ARBLACKPINKLisaRoseJisooJenniePas encore d'évaluation

- Petty Cash - Imprest and Fluctuating SystemDocument4 pagesPetty Cash - Imprest and Fluctuating SystemNika Bautista100% (1)

- Problem Set 2Document4 pagesProblem Set 2Michael Jay LingerasPas encore d'évaluation

- AdjustingDocument39 pagesAdjustingRica mae camon100% (1)

- (Studocu) Int Acc Chapter 2 - Valix, Robles, Empleo, MillanDocument4 pages(Studocu) Int Acc Chapter 2 - Valix, Robles, Empleo, MillanHufana, ShelleyPas encore d'évaluation

- FInancial Accounting and Reporting1C6Document19 pagesFInancial Accounting and Reporting1C6Yen YenPas encore d'évaluation

- Advance Payment of Revenues: Liability MethodDocument9 pagesAdvance Payment of Revenues: Liability MethodDan Ryan100% (1)

- Accounting Sample ProblemsDocument1 pageAccounting Sample ProblemsKeitheia QuidlatPas encore d'évaluation

- Cash and Cash Equivalent QuizesDocument4 pagesCash and Cash Equivalent QuizesGIRL100% (1)

- Financial Accounting Review Problem 1Document16 pagesFinancial Accounting Review Problem 1YukiPas encore d'évaluation

- 2 3 2017 ReceivablesDocument4 pages2 3 2017 ReceivablesMr. CopernicusPas encore d'évaluation

- 112 Seatwork1 ForStudentsDocument5 pages112 Seatwork1 ForStudentsJoventino NebresPas encore d'évaluation

- Proof of Cash Syria CompanyDocument4 pagesProof of Cash Syria CompanyCJ alandy100% (1)

- Bank Recon and PCFDocument2 pagesBank Recon and PCFAiza Ordoño0% (1)

- Chapter 2 - Cash and Cash Equivalents (Problems)Document2 pagesChapter 2 - Cash and Cash Equivalents (Problems)Lea Victoria PronuevoPas encore d'évaluation

- This Study Resource Was: NAME: - SECTION: - SCORE: - RATINGDocument6 pagesThis Study Resource Was: NAME: - SECTION: - SCORE: - RATINGMasashi KishimotoPas encore d'évaluation

- Inacc 1 Chap 3 Act PDFDocument12 pagesInacc 1 Chap 3 Act PDFSharmin Reula50% (2)

- Assignment and Quiz 2 Accounting For CashDocument5 pagesAssignment and Quiz 2 Accounting For CashGab BautroPas encore d'évaluation

- CashDocument7 pagesCashhellohello100% (1)

- ACCOUNTING 2 ReviewDocument4 pagesACCOUNTING 2 ReviewAhnJello100% (1)

- Accounting For Materials - 1Document2 pagesAccounting For Materials - 1Charles Tuazon50% (2)

- Prob Basic AcctDocument3 pagesProb Basic AcctSamuel Ferolino50% (2)

- Working Papers in InventoriesDocument17 pagesWorking Papers in InventoriesTrisha VillegasPas encore d'évaluation

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsFrancine Thea M. Lantaya100% (1)

- Le 1 Answer KeyDocument8 pagesLe 1 Answer KeyApril NaidaPas encore d'évaluation

- (03A) AR NR Quiz ANSWER KEYDocument8 pages(03A) AR NR Quiz ANSWER KEYKhai Ed PabelicoPas encore d'évaluation

- CFAS Chapter 8-9, 11 Financial StatementsDocument2 pagesCFAS Chapter 8-9, 11 Financial StatementsKaren CaelPas encore d'évaluation

- Accounts ReceivableDocument34 pagesAccounts ReceivableRose Aubrey A Cordova100% (1)

- FAR Freight ChargesDocument2 pagesFAR Freight ChargesJaybie John Palco Eralino100% (1)

- Group 3: 1. New Set of BooksDocument5 pagesGroup 3: 1. New Set of Bookschelsea kayle licomes fuentesPas encore d'évaluation

- Ia 2Document2 pagesIa 2Nadine SofiaPas encore d'évaluation

- Cash and Cash EquivalentsDocument50 pagesCash and Cash EquivalentsAnne EstrellaPas encore d'évaluation

- AIS Journal Entries and Adjusting EntriesDocument2 pagesAIS Journal Entries and Adjusting EntriesIeva Francheska Agustin83% (6)

- Chapter 2 Cash and Cash EquivalentsDocument10 pagesChapter 2 Cash and Cash EquivalentsShe SalazarPas encore d'évaluation

- Cash and CashDocument13 pagesCash and CashAnonymous WmvilCEFPas encore d'évaluation

- Cash and Cash Equivalents Problems 2.1 (Money Company)Document9 pagesCash and Cash Equivalents Problems 2.1 (Money Company)Renz AlconeraPas encore d'évaluation

- Solutions To Activity 1 A, 1B, 1C and 1DDocument2 pagesSolutions To Activity 1 A, 1B, 1C and 1DPrincess Mae ArabitPas encore d'évaluation

- Profitaility RatioDocument1 pageProfitaility Ratiokim wonpilPas encore d'évaluation

- Meriales, Patricia Anne S. Bsa-3. MNGT 413 2:30 MW FDocument6 pagesMeriales, Patricia Anne S. Bsa-3. MNGT 413 2:30 MW Fkim wonpilPas encore d'évaluation

- Systems Integration, Management Involvement and Quality of Internal Controls and AuditingDocument21 pagesSystems Integration, Management Involvement and Quality of Internal Controls and Auditingkim wonpilPas encore d'évaluation

- Informal Report Writing - 2 PDFDocument22 pagesInformal Report Writing - 2 PDFPankaj Gautam50% (2)

- Financial Performance Analysis of Exim Bank Ltd.Document54 pagesFinancial Performance Analysis of Exim Bank Ltd.Zannatul Ferdousi Alam YameemPas encore d'évaluation

- Bank Recon and Petty CashDocument44 pagesBank Recon and Petty CashJulienne UntalascoPas encore d'évaluation

- ACC 124 - Exercise 1 - Cash and Cash EquivalentsDocument4 pagesACC 124 - Exercise 1 - Cash and Cash EquivalentsChristine Mae GaloPas encore d'évaluation

- 01 Apr 2021 - 31 Mar 2022Document48 pages01 Apr 2021 - 31 Mar 2022Subhash JhaPas encore d'évaluation

- UGBS 205 Fundamentals of Accounting Methods: Week 8 - Bank Reconciliation StatementDocument16 pagesUGBS 205 Fundamentals of Accounting Methods: Week 8 - Bank Reconciliation StatementYaw Baah-BarimahPas encore d'évaluation

- Group 5 Final Written Report-Legal FormsDocument34 pagesGroup 5 Final Written Report-Legal FormsFederico Dipay Jr.Pas encore d'évaluation

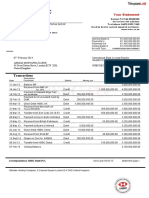

- HSBC Bank StatementDocument1 pageHSBC Bank Statementwilliams edwards78% (9)

- Bhs Inggris NickoDocument10 pagesBhs Inggris NickoKhoirul Fikri SmunjuPas encore d'évaluation

- Statement of Axis Account No:919010012738847 For The Period (From: 08-09-2020 To: 07-09-2021)Document2 pagesStatement of Axis Account No:919010012738847 For The Period (From: 08-09-2020 To: 07-09-2021)Sayan SarkarPas encore d'évaluation

- Module 1 CashDocument13 pagesModule 1 CashKim JisooPas encore d'évaluation

- Assignment No. 1 - Cash and Cash EquivalentsDocument5 pagesAssignment No. 1 - Cash and Cash EquivalentsVincent AbellaPas encore d'évaluation

- UblDocument93 pagesUblIfrah BatoolPas encore d'évaluation

- Allstate Liability MoanoDocument4 pagesAllstate Liability MoanoMichael ClorPas encore d'évaluation

- Comt Brochure 8 Days New FinalDocument12 pagesComt Brochure 8 Days New Finaljingluo educationPas encore d'évaluation

- Ujjivan SFB - 2020-AR PDFDocument300 pagesUjjivan SFB - 2020-AR PDFanil1820Pas encore d'évaluation

- SA's Best Value For You and Your FamilyDocument38 pagesSA's Best Value For You and Your FamilyKosie SmithPas encore d'évaluation

- DownloadDocument2 pagesDownloadSourav mPas encore d'évaluation

- Lesson 1 Cash and Cash EquivalentsDocument10 pagesLesson 1 Cash and Cash EquivalentsRica Lei N. DomingoPas encore d'évaluation

- HDFC Bank LoansDocument75 pagesHDFC Bank LoansSahil Sethi100% (2)

- Murali ReportDocument75 pagesMurali Reportsachin mohanPas encore d'évaluation

- Case Studies - Banking Law&PracticeDocument5 pagesCase Studies - Banking Law&PracticeRedSun50% (4)

- 2023 Pricing Brochure ABSADocument85 pages2023 Pricing Brochure ABSAkefiyalew BPas encore d'évaluation

- Cornerstone - Fintech Adoption in The USDocument29 pagesCornerstone - Fintech Adoption in The USPriti VarmaPas encore d'évaluation

- Customer Retention Strategies at HDFC BankDocument20 pagesCustomer Retention Strategies at HDFC BankHemantSharma100% (1)

- Hybride Troisieme Annee Revised Version ADocument31 pagesHybride Troisieme Annee Revised Version AAndria LarissaPas encore d'évaluation

- Curs de EnglezaDocument333 pagesCurs de Englezaates_inf497Pas encore d'évaluation

- Cash Flow StatmentDocument91 pagesCash Flow StatmentSathishmuPas encore d'évaluation

- PT CAP BasicBankingDocument3 pagesPT CAP BasicBankingRayan PaulPas encore d'évaluation

- Economics Project 1 Topic: Balance of Payment Name of Student: ANMOL Bhardwaj Class/Sec: XII-A Roll No: 41Document36 pagesEconomics Project 1 Topic: Balance of Payment Name of Student: ANMOL Bhardwaj Class/Sec: XII-A Roll No: 41weeolPas encore d'évaluation

- Project in C++ (Banking Management System)Document24 pagesProject in C++ (Banking Management System)Vinod Verma67% (55)