Vous aimerez peut-être aussi

- Final Defense PPT GoodluckDocument23 pagesFinal Defense PPT GoodluckJulie EstopacePas encore d'évaluation

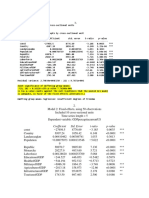

- Coefficient Std. Error T-Ratio P-ValueDocument5 pagesCoefficient Std. Error T-Ratio P-ValueJulie EstopacePas encore d'évaluation

- Accountancy Day - Reaction PaperDocument2 pagesAccountancy Day - Reaction PaperJulie EstopacePas encore d'évaluation

- Strategies in The Corporate WorldDocument66 pagesStrategies in The Corporate WorldJulie EstopacePas encore d'évaluation

- Module III 1Document1 pageModule III 1Julie EstopacePas encore d'évaluation

- AudProb - Cash and Cash EquivalentsDocument16 pagesAudProb - Cash and Cash EquivalentsJulie EstopacePas encore d'évaluation

- Julie F. Estopace Ivy H. Jariño Eddelyn J. Madriaga Joella Ann S. Pura Concept Paper in Accounting Thesis I BS in Accountancy IVDocument2 pagesJulie F. Estopace Ivy H. Jariño Eddelyn J. Madriaga Joella Ann S. Pura Concept Paper in Accounting Thesis I BS in Accountancy IVJulie EstopacePas encore d'évaluation

- Related StudyDocument1 pageRelated StudyJulie EstopacePas encore d'évaluation

- Designing Business Level StrategiesDocument58 pagesDesigning Business Level StrategiesJulie Estopace100% (1)

- Organizational Dependencies CronicoDocument11 pagesOrganizational Dependencies CronicoJulie EstopacePas encore d'évaluation

- DfflNanu Julie-WPS OfficeDocument1 pageDfflNanu Julie-WPS OfficeJulie EstopacePas encore d'évaluation

- 44444444-WPS OfficeDocument1 page44444444-WPS OfficeJulie EstopacePas encore d'évaluation

- Gotscombodd90we Wps OfficeDocument4 pagesGotscombodd90we Wps OfficeJulie EstopacePas encore d'évaluation

- AwuhDocument2 pagesAwuhJulie EstopacePas encore d'évaluation

- Aeb1 11809051Document28 pagesAeb1 11809051fatmaPas encore d'évaluation

- Yooowwww WPS OfficeDocument1 pageYooowwww WPS OfficeJulie EstopacePas encore d'évaluation

- huuyyyy-WPS OfficeDocument1 pagehuuyyyy-WPS OfficeJulie EstopacePas encore d'évaluation

- 44444444-WPS OfficeDocument1 page44444444-WPS OfficeJulie EstopacePas encore d'évaluation

- Heyyyyy WPS OfficeDocument1 pageHeyyyyy WPS OfficeJulie EstopacePas encore d'évaluation

- Yaa Na Ang Simbag PDFDocument54 pagesYaa Na Ang Simbag PDFJulie EstopacePas encore d'évaluation

- LTC Roque PDFDocument24 pagesLTC Roque PDFJulie EstopacePas encore d'évaluation

- THDH Vgjvxdhk22222n WPS OfficeDocument1 pageTHDH Vgjvxdhk22222n WPS OfficeJulie EstopacePas encore d'évaluation

- Table of ContentsDocument2 pagesTable of ContentsJulie EstopacePas encore d'évaluation

- Name of School Address of School Enrolled Subjects: Code Description Units Schedule Instructor Section EbookDocument1 pageName of School Address of School Enrolled Subjects: Code Description Units Schedule Instructor Section EbookJulie EstopacePas encore d'évaluation

- RIZAL As A FeministDocument14 pagesRIZAL As A FeministJulie EstopacePas encore d'évaluation

- LETTERS TO BE OPENED AFTER HIS DEATHDocument12 pagesLETTERS TO BE OPENED AFTER HIS DEATHJulie EstopacePas encore d'évaluation

- Pom (May Sales Forecast Na)Document12 pagesPom (May Sales Forecast Na)Julie EstopacePas encore d'évaluation

- Edss PDFDocument13 pagesEdss PDFJulie EstopacePas encore d'évaluation

- RIZAL The Man and The HeroDocument16 pagesRIZAL The Man and The HeroJulie Estopace100% (1)

- RIZAL As A FeministDocument14 pagesRIZAL As A FeministJulie EstopacePas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5782)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Understanding GAAP Accounting PrinciplesDocument4 pagesUnderstanding GAAP Accounting PrinciplesRihana Khatun67% (3)

- Illustration: Formation of Partnership Valuation of Capital A BDocument2 pagesIllustration: Formation of Partnership Valuation of Capital A BArian AmuraoPas encore d'évaluation

- 05 CAPM - ADocument73 pages05 CAPM - AHaoyang Pazzini YePas encore d'évaluation

- Chapter NineDocument10 pagesChapter NineAsif HossainPas encore d'évaluation

- Zomato IPO Allotment DetailsDocument2 pagesZomato IPO Allotment DetailsAmit PandeyPas encore d'évaluation

- FD Lecture XIII XIVDocument39 pagesFD Lecture XIII XIVVineet RanjanPas encore d'évaluation

- ResultsresultsDocument2 pagesResultsresultsamanda.sunartoPas encore d'évaluation

- PAS 27, Separate Financial StatementsDocument13 pagesPAS 27, Separate Financial Statementsjulia4razoPas encore d'évaluation

- Dynamic Trend Trading The SystemDocument151 pagesDynamic Trend Trading The Systemmangelbel674988% (26)

- (FM02) - Chapter 7 The Valuation of Ordinary SharesDocument12 pages(FM02) - Chapter 7 The Valuation of Ordinary SharesKenneth John TomasPas encore d'évaluation

- MF FundServ FactsheetDocument2 pagesMF FundServ FactsheetNahy Adel NadaPas encore d'évaluation

- Monopolistic Competition - MaterialsDocument12 pagesMonopolistic Competition - Materialsroshxsam1972Pas encore d'évaluation

- Morton Handley & CompanyDocument4 pagesMorton Handley & Companybusinessdoctor23Pas encore d'évaluation

- Project Management UnitDocument12 pagesProject Management UnitSyed JafferPas encore d'évaluation

- Asset Liabilities + Owner'S EquityDocument4 pagesAsset Liabilities + Owner'S EquitydenixngPas encore d'évaluation

- Cash Flow Part 2 To 7 Term 2 Sunil PandaDocument35 pagesCash Flow Part 2 To 7 Term 2 Sunil PandaAnupama SinghPas encore d'évaluation

- Beaver W 1968 The Information Content of Annual Earnings AnnouncementsDocument15 pagesBeaver W 1968 The Information Content of Annual Earnings AnnouncementsYuvendren LingamPas encore d'évaluation

- Revision Test Papers MAY, 2023: Final Course Group - IDocument172 pagesRevision Test Papers MAY, 2023: Final Course Group - IEDGE VENTURESPas encore d'évaluation

- 13 Activity 1Document2 pages13 Activity 1•MUSIC MOOD•Pas encore d'évaluation

- WSO Experienced Deals Resume Template-Transaction-Exp2 (1) 0Document2 pagesWSO Experienced Deals Resume Template-Transaction-Exp2 (1) 0jason.sevin02Pas encore d'évaluation

- 04 SandP Exhibit4 v2Document8 pages04 SandP Exhibit4 v2Nabeel KhanPas encore d'évaluation

- How Much Is The Minimum Stock Investment in The Philippines?Document4 pagesHow Much Is The Minimum Stock Investment in The Philippines?Laws HackerPas encore d'évaluation

- Notes On Corporation Law (Sec 1-9)Document8 pagesNotes On Corporation Law (Sec 1-9)davemarklazaga179Pas encore d'évaluation

- The 5 Basic Plays of Trading Options VS2Document18 pagesThe 5 Basic Plays of Trading Options VS2Piet AardsePas encore d'évaluation

- Note On Public IssueDocument9 pagesNote On Public IssueKrish KalraPas encore d'évaluation

- Principles of Corporate Finance 12th Edition Brealey Test BankDocument19 pagesPrinciples of Corporate Finance 12th Edition Brealey Test BankGloria Nicol100% (30)

- TRIAL Food Drink Marketplace Financial Model Excel Template v.1.0.122020Document90 pagesTRIAL Food Drink Marketplace Financial Model Excel Template v.1.0.122020motebangPas encore d'évaluation

- 4.dissolution of Partnership FirmDocument11 pages4.dissolution of Partnership Firmtripatjotkaur757Pas encore d'évaluation

- DSP Blackrock Tax Saver Fund KimDocument22 pagesDSP Blackrock Tax Saver Fund KimPRANUPas encore d'évaluation

- Illustration: Business Combination Achieved in StagesDocument26 pagesIllustration: Business Combination Achieved in StagesArlene Diane Orozco100% (1)