Vous aimerez peut-être aussi

- Articles of IncorporationDocument14 pagesArticles of IncorporationUlyssis RL Cariño100% (1)

- Latham & Watkins LLP Latham & Watkins LLP: Counsel To The Foreign RepresentativesDocument26 pagesLatham & Watkins LLP Latham & Watkins LLP: Counsel To The Foreign RepresentativesMichaelPatrickMcSweeneyPas encore d'évaluation

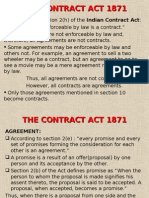

- The Contract Act 1871 (R)Document55 pagesThe Contract Act 1871 (R)manishparipagar100% (2)

- Debt Collection Article PDFDocument38 pagesDebt Collection Article PDFAlexandria BurrisPas encore d'évaluation

- 2016-05-10 FDCPA Case Law Review For April 2016Document3 pages2016-05-10 FDCPA Case Law Review For April 2016D. BushPas encore d'évaluation

- Smart Speed, Inc. By-LawsDocument7 pagesSmart Speed, Inc. By-LawsAira Dee SuarezPas encore d'évaluation

- TILA Shared PDFDocument8 pagesTILA Shared PDFGretchen Alunday SuarezPas encore d'évaluation

- Security Bank vs Cuenca: Novation Extinguished Surety's LiabilityDocument1 pageSecurity Bank vs Cuenca: Novation Extinguished Surety's LiabilityDione Klarisse GuevaraPas encore d'évaluation

- Financial Accounting Standards BoardDocument9 pagesFinancial Accounting Standards BoardTarun GuntnurPas encore d'évaluation

- Business Law Unit - IVDocument9 pagesBusiness Law Unit - IVKaran Veer SinghPas encore d'évaluation

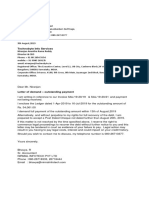

- Letter of Demand Outstanding PaymentDocument1 pageLetter of Demand Outstanding PaymentanjumPas encore d'évaluation

- Bankruptcy Act of 1984 Under Chapter 67 of The Brunei Darussalam Laws.Document11 pagesBankruptcy Act of 1984 Under Chapter 67 of The Brunei Darussalam Laws.Madison SheenaPas encore d'évaluation

- Brief Sample - SJM Debt Buyer Collection Case PDFDocument6 pagesBrief Sample - SJM Debt Buyer Collection Case PDFAndyPas encore d'évaluation

- Contracts Notes. 2.27.2013Document14 pagesContracts Notes. 2.27.2013Jairus AntonyPas encore d'évaluation

- Loan Agreement and Promissory NoteDocument6 pagesLoan Agreement and Promissory NoteDanielPas encore d'évaluation

- VanDyk Mortgage Fair Lending PolicyDocument2 pagesVanDyk Mortgage Fair Lending PolicyVanDyk Mortgage CorporationPas encore d'évaluation

- Ls - Confidentiality and Nondisclosure Agreement For ClientsDocument2 pagesLs - Confidentiality and Nondisclosure Agreement For ClientsHeinz MilitarPas encore d'évaluation

- C C C CCCCCCC CC CDocument4 pagesC C C CCCCCCC CC CAdriana Paola GuerreroPas encore d'évaluation

- SLAPP Motion Minkowanti-SlappDocument40 pagesSLAPP Motion Minkowanti-SlappDarren ChakerPas encore d'évaluation

- What Is A Treasury BondDocument12 pagesWhat Is A Treasury Bondmorris yenenehPas encore d'évaluation

- Sources of Credit InformationDocument2 pagesSources of Credit InformationR100% (1)

- Collection Agency AgreementDocument18 pagesCollection Agency AgreementJannah MagtaasPas encore d'évaluation

- Bankruptcy Intake FormDocument12 pagesBankruptcy Intake Formzack8182Pas encore d'évaluation

- 1a. Motion To DismissDocument7 pages1a. Motion To Dismiss1SantaFeanPas encore d'évaluation

- Disbursement Request FormDocument1 pageDisbursement Request FormbibincmPas encore d'évaluation

- Uscode-2015-Chapter 2a-Securities and Trust IndenturesDocument78 pagesUscode-2015-Chapter 2a-Securities and Trust IndenturesS Pablo AugustPas encore d'évaluation

- Habeas Corpus CasesDocument38 pagesHabeas Corpus CasesVernie BacalsoPas encore d'évaluation

- A BondDocument3 pagesA Bondnusra_t100% (1)

- Law On Public OfficersDocument218 pagesLaw On Public OfficersLex LimPas encore d'évaluation

- Basis For Loan Classification: (A) Objective CriteriaDocument9 pagesBasis For Loan Classification: (A) Objective Criteriahabib7hPas encore d'évaluation

- Fair Lending Laws OverviewDocument25 pagesFair Lending Laws OverviewPriya DasPas encore d'évaluation

- 3 Credit Bureaus Address - Google SearchDocument1 page3 Credit Bureaus Address - Google Searchemmanuelhood642Pas encore d'évaluation

- Tda066 PDFDocument13 pagesTda066 PDFjuanPas encore d'évaluation

- 2 Dex11.Htm Form of Underwriting Agreement: Homas Eisel Artners Acific Rest Ecurities NC Apital Arkets Orporation Owen ODocument30 pages2 Dex11.Htm Form of Underwriting Agreement: Homas Eisel Artners Acific Rest Ecurities NC Apital Arkets Orporation Owen OVidhan GuptaPas encore d'évaluation

- Securitization of BanksDocument31 pagesSecuritization of BanksKumar Deepak100% (1)

- Credit InstrumentsDocument21 pagesCredit InstrumentsJoann SacolPas encore d'évaluation

- File CH Tila Worksheet 07Document2 pagesFile CH Tila Worksheet 07Helpin HandPas encore d'évaluation

- Debt Vs EquityDocument4 pagesDebt Vs EquityNooraghaPas encore d'évaluation

- Assignment - Credit PolicyDocument10 pagesAssignment - Credit PolicyNilesh VadherPas encore d'évaluation

- State Request For Statements of InterestDocument3 pagesState Request For Statements of InterestThe Republican/MassLive.comPas encore d'évaluation

- Sample Thailand Usufruct ContractDocument7 pagesSample Thailand Usufruct ContractGayle Opsima-BiraoPas encore d'évaluation

- Weintraub v. QUICKEN LOANS, INC, 594 F.3d 270, 4th Cir. (2010)Document12 pagesWeintraub v. QUICKEN LOANS, INC, 594 F.3d 270, 4th Cir. (2010)Scribd Government DocsPas encore d'évaluation

- Woman Files Lawsuit To Prove She Is AliveDocument15 pagesWoman Files Lawsuit To Prove She Is AliveFindLawPas encore d'évaluation

- Non Performing AssetsDocument63 pagesNon Performing AssetsProf Dr Chowdari Prasad100% (4)

- Loan RestructuringDocument22 pagesLoan RestructuringNazmul H. PalashPas encore d'évaluation

- Public NoticeDocument3 pagesPublic NoticeHarsh ChaudharyPas encore d'évaluation

- Republic Act No. 11057: Title Declaration of PolicyDocument19 pagesRepublic Act No. 11057: Title Declaration of PolicyJoey Villas MaputiPas encore d'évaluation

- Banking Law Loans and AdvancesDocument35 pagesBanking Law Loans and AdvancesNisha SanoojPas encore d'évaluation

- CounterclaimDocument25 pagesCounterclaimRichie CollinsPas encore d'évaluation

- Kurenitz V Stellar Recovery Inc Debt Collection Minnesota FDCPA Mark L Heaney Heaney Law Firm LLCDocument10 pagesKurenitz V Stellar Recovery Inc Debt Collection Minnesota FDCPA Mark L Heaney Heaney Law Firm LLCghostgripPas encore d'évaluation

- Wage GarnishmentDocument2 pagesWage Garnishmentmsc12061980Pas encore d'évaluation

- Module 1 Credit FundamentalsDocument24 pagesModule 1 Credit FundamentalsCaroline Grace Enteria Mella100% (1)

- ECOA AnnotationsDocument4 pagesECOA AnnotationsvaughansavPas encore d'évaluation

- Equitable Mortgage ExplainedDocument6 pagesEquitable Mortgage ExplainedJoy TaglePas encore d'évaluation

- Short Sale Seminar Bakersfield, CADocument22 pagesShort Sale Seminar Bakersfield, CAMiguel GarciaPas encore d'évaluation

- NDA SampleDocument5 pagesNDA SampleHein Sithu KyawPas encore d'évaluation

- Presentation On Financial InstrumentsDocument20 pagesPresentation On Financial InstrumentsMehak BhallaPas encore d'évaluation

- LoansDocument64 pagesLoans9897856218Pas encore d'évaluation

- Rescued! 401k Plan Traps Business Owners Must Avoid and FixD'EverandRescued! 401k Plan Traps Business Owners Must Avoid and FixPas encore d'évaluation

- The Declaration of Independence: A Play for Many ReadersD'EverandThe Declaration of Independence: A Play for Many ReadersPas encore d'évaluation

- Wiley Series 24 Securities Licensing Exam Review 2019 + Test Bank: The General Securities Principal ExaminationD'EverandWiley Series 24 Securities Licensing Exam Review 2019 + Test Bank: The General Securities Principal ExaminationPas encore d'évaluation

- October 2023 CPI ReportDocument5 pagesOctober 2023 CPI ReportAnonymous UpWci5Pas encore d'évaluation

- Winners Edge Mountain Bike Cross Country National ChampionshipsDocument3 pagesWinners Edge Mountain Bike Cross Country National ChampionshipsAnonymous UpWci5Pas encore d'évaluation

- Order of Business - 6th March, 2024Document2 pagesOrder of Business - 6th March, 2024Anonymous UpWci5Pas encore d'évaluation

- Order of Business - 6th March, 2024Document2 pagesOrder of Business - 6th March, 2024Anonymous UpWci5Pas encore d'évaluation

- Senate - 2024 March 21Document2 pagesSenate - 2024 March 21Anonymous UpWci5Pas encore d'évaluation

- Order of Business - 28th February, 2024Document2 pagesOrder of Business - 28th February, 2024Anonymous UpWci5Pas encore d'évaluation

- Road Sobriety Checkpoint Notice 2024Document2 pagesRoad Sobriety Checkpoint Notice 2024Anonymous UpWci5Pas encore d'évaluation

- Winners Edge Mountain Bike Cross Country National ChampionshipsDocument3 pagesWinners Edge Mountain Bike Cross Country National ChampionshipsAnonymous UpWci5Pas encore d'évaluation

- Weekly Shipping March 23 2024Document1 pageWeekly Shipping March 23 2024Anonymous UpWci5Pas encore d'évaluation

- Senate - 2024 March 18Document3 pagesSenate - 2024 March 18Anonymous UpWci5Pas encore d'évaluation

- FinTech Year End Report 2023Document6 pagesFinTech Year End Report 2023Anonymous UpWci5Pas encore d'évaluation

- Senate - 2024 March 13Document3 pagesSenate - 2024 March 13Anonymous UpWci5Pas encore d'évaluation

- Bermuda Budget Snapshot 2024 - FinalDocument1 pageBermuda Budget Snapshot 2024 - FinalAnonymous UpWci5Pas encore d'évaluation

- Order of Business - 1st March, 2024Document2 pagesOrder of Business - 1st March, 2024Anonymous UpWci5Pas encore d'évaluation

- Senate - 2024 Feb 14Document3 pagesSenate - 2024 Feb 14Anonymous UpWci5Pas encore d'évaluation

- Road Sobriety Checkpoint Notice 2024Document2 pagesRoad Sobriety Checkpoint Notice 2024Anonymous UpWci5Pas encore d'évaluation

- Weekly Shipping February 3 2024Document1 pageWeekly Shipping February 3 2024Anonymous UpWci5Pas encore d'évaluation

- Weekly Shipping February 17 2024Document1 pageWeekly Shipping February 17 2024Anonymous UpWci5Pas encore d'évaluation

- Weekly Shipping January 20 2024Document1 pageWeekly Shipping January 20 2024Anonymous UpWci5Pas encore d'évaluation

- Weekly Shipping January 20 2024Document1 pageWeekly Shipping January 20 2024Anonymous UpWci5Pas encore d'évaluation

- Order of Business Friday, 10th November, 2023Document2 pagesOrder of Business Friday, 10th November, 2023Anonymous UpWci5Pas encore d'évaluation

- Road Sobriety Checkpoint Notice No. 9 2019Document2 pagesRoad Sobriety Checkpoint Notice No. 9 2019Anonymous UpWci5Pas encore d'évaluation

- Decision 37 2023 Ministry of Health Headquarters FINALDocument13 pagesDecision 37 2023 Ministry of Health Headquarters FINALAnonymous UpWci5Pas encore d'évaluation

- Butterfield Mile Trials Bermuda Dec 8 2023Document5 pagesButterfield Mile Trials Bermuda Dec 8 2023Anonymous UpWci5Pas encore d'évaluation

- June 2023 RSI ReportDocument4 pagesJune 2023 RSI ReportAnonymous UpWci5Pas encore d'évaluation

- Decision 34 2023 Bermuda Police ServiceDocument19 pagesDecision 34 2023 Bermuda Police ServiceAnonymous UpWci5Pas encore d'évaluation

- Decision 43 2023 Bermuda Police ServiceDocument11 pagesDecision 43 2023 Bermuda Police ServiceAnonymous UpWci5Pas encore d'évaluation

- Order of Business Friday, 10th November, 2023Document2 pagesOrder of Business Friday, 10th November, 2023Anonymous UpWci5Pas encore d'évaluation

- Butterfield Bermuda Championship Report 2022 FINALDocument17 pagesButterfield Bermuda Championship Report 2022 FINALAnonymous UpWci5Pas encore d'évaluation

- Road Sobriety Checkpoint Notice No 7 2023Document3 pagesRoad Sobriety Checkpoint Notice No 7 2023Anonymous UpWci5Pas encore d'évaluation

- TUTORIAL 1 SOLUTIONS MONEY BANKING FINANCIAL MARKETSDocument4 pagesTUTORIAL 1 SOLUTIONS MONEY BANKING FINANCIAL MARKETSVeronica MishraPas encore d'évaluation

- Chap 009Document20 pagesChap 009Ela PelariPas encore d'évaluation

- Law 549-Remedies (Bankruptcy) Tutorial Bankruptcy Notice (Group 3)Document6 pagesLaw 549-Remedies (Bankruptcy) Tutorial Bankruptcy Notice (Group 3)diannedensonPas encore d'évaluation

- Cpar - BLT 09.14.13Document14 pagesCpar - BLT 09.14.13Charry Ramos100% (1)

- Bjaj Auto Finance Ltd. FinalDocument55 pagesBjaj Auto Finance Ltd. Finalvishnu0751Pas encore d'évaluation

- Mutual Fund Performance ReportDocument88 pagesMutual Fund Performance ReportDarvesh SinghPas encore d'évaluation

- SuretyDocument2 pagesSuretyNiño Rey LopezPas encore d'évaluation

- ACCTNGDocument3 pagesACCTNGLynnie KimPas encore d'évaluation

- Replace Your Mortgage Ebook - No - Companion PDFDocument62 pagesReplace Your Mortgage Ebook - No - Companion PDFJeff Smith100% (2)

- CFPB v. Mackinnon, Et Al. 1:16-cv-00880-FPG-HKSDocument31 pagesCFPB v. Mackinnon, Et Al. 1:16-cv-00880-FPG-HKSPacer CasesPas encore d'évaluation

- The Government-Created Subprime Mortgage Meltdown by Thomas DiLorenzoDocument3 pagesThe Government-Created Subprime Mortgage Meltdown by Thomas DiLorenzodavid rockPas encore d'évaluation

- Spouses Wilfredo NDocument2 pagesSpouses Wilfredo NRogie ApoloPas encore d'évaluation

- 0823.HK The Link REIT 2009-2010 Annual ReportDocument198 pages0823.HK The Link REIT 2009-2010 Annual Reportwalamaking100% (1)

- What is a credit rating? Its types and agencies in IndiaDocument19 pagesWhat is a credit rating? Its types and agencies in IndiaParth MahajanPas encore d'évaluation

- Unit 6: Average Due Date: Learning OutcomesDocument21 pagesUnit 6: Average Due Date: Learning OutcomesAshish SultaniaPas encore d'évaluation

- CFA Level 1 Study GuideDocument40 pagesCFA Level 1 Study GuideTom RomanoPas encore d'évaluation

- Civil Procedure Rule 57 Preliminary AttachmentDocument36 pagesCivil Procedure Rule 57 Preliminary AttachmenttmaderazoPas encore d'évaluation

- Income Taxation Outline Prof. Neil Buchanan SPRING 2007 Basic Income Tax OutlineDocument28 pagesIncome Taxation Outline Prof. Neil Buchanan SPRING 2007 Basic Income Tax OutlinejhouvanPas encore d'évaluation

- DMCI Financial AssesmentDocument61 pagesDMCI Financial AssesmentRinna Jane Rivera BolandresPas encore d'évaluation

- FAR.3018 Loans and Receivables - Long TermDocument4 pagesFAR.3018 Loans and Receivables - Long TermJethro ConchaPas encore d'évaluation

- 01 - Henkel Overview (Solution)Document8 pages01 - Henkel Overview (Solution)/jncjdncjdnPas encore d'évaluation

- Chapter 3Document38 pagesChapter 3akmal_07Pas encore d'évaluation

- Xi Jinping Personally Halted Ant's IPO After Jack Ma Snubbed Government Leaders - Hacker NewsDocument20 pagesXi Jinping Personally Halted Ant's IPO After Jack Ma Snubbed Government Leaders - Hacker NewsJose Luis LoyaPas encore d'évaluation

- VILLAROEL Vs ESTRADA G.R. No. 47362 December 19, 1940Document1 pageVILLAROEL Vs ESTRADA G.R. No. 47362 December 19, 1940Anna NicerioPas encore d'évaluation

- Business Finance Week 1 To 3 Without Answer KeyDocument29 pagesBusiness Finance Week 1 To 3 Without Answer KeyKristel Anne Roquero Balisi100% (1)

- A Case Study of Profitability Analysis of Standard Chartered Bank Nepal LTDDocument16 pagesA Case Study of Profitability Analysis of Standard Chartered Bank Nepal LTDDiwesh Tamrakar100% (1)

- Jose v. Herrera vs. Leviste, G.R. No. 55744, February 28, 1985Document10 pagesJose v. Herrera vs. Leviste, G.R. No. 55744, February 28, 1985Fides DamascoPas encore d'évaluation

- Trans-Pacific Industrial v. CADocument1 pageTrans-Pacific Industrial v. CAKimPas encore d'évaluation

- Credit Risk Analysis of Canara Bank - A Case StudyDocument11 pagesCredit Risk Analysis of Canara Bank - A Case Studysharon0% (1)