Vous aimerez peut-être aussi

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Gender and Society Lecture Notes PDFDocument13 pagesGender and Society Lecture Notes PDFPsychelynne Maggay Nicolas100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Remedial Law Review List of CasesDocument11 pagesRemedial Law Review List of CasesPsychelynne Maggay Nicolas0% (1)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- ATTENDANCEDocument1 pageATTENDANCEPsychelynne Maggay NicolasPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Cases in Political LawDocument4 pagesCases in Political LawPsychelynne Maggay NicolasPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Demand LetterDocument2 pagesDemand LetterPsychelynne Maggay NicolasPas encore d'évaluation

- NAZARENO V City of DumagueteDocument2 pagesNAZARENO V City of DumaguetePsychelynne Maggay NicolasPas encore d'évaluation

- Ruzol VS SandiganbayanDocument26 pagesRuzol VS SandiganbayanPsychelynne Maggay NicolasPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Civ Wave 1Document4 pagesCiv Wave 1Psychelynne Maggay NicolasPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Krivenko v. Register of Deeds, GR No. L-630, Nov. 15, 194 Borromeo v. Descallar, GR No. 159310, Feb. 24, 2009Document2 pagesKrivenko v. Register of Deeds, GR No. L-630, Nov. 15, 194 Borromeo v. Descallar, GR No. 159310, Feb. 24, 2009Psychelynne Maggay NicolasPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- G.R. No. 189486 September 5, 2012 Simny G. Guy Et Al Vs Gilbert G. GuyDocument7 pagesG.R. No. 189486 September 5, 2012 Simny G. Guy Et Al Vs Gilbert G. GuyPsychelynne Maggay NicolasPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- G.R. No. L-34362 November 19, 1982 Modesta Calimlim vs. Hon. Pedro A. RamirezDocument3 pagesG.R. No. L-34362 November 19, 1982 Modesta Calimlim vs. Hon. Pedro A. RamirezPsychelynne Maggay NicolasPas encore d'évaluation

- UNICAN Vs NEADocument3 pagesUNICAN Vs NEAPsychelynne Maggay NicolasPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Affidavit of Revocation and RescissionDocument13 pagesAffidavit of Revocation and RescissionJohn Foster100% (6)

- CS General Info 11-26-02Document10 pagesCS General Info 11-26-02wealth2520Pas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Tax Flow ChartDocument2 pagesTax Flow ChartAutochthon GazettePas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- R.A. 8424 National Internal Revenue Code of 1997 and Its AmendmentsDocument319 pagesR.A. 8424 National Internal Revenue Code of 1997 and Its AmendmentsSonny MorilloPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Affidavit of Citizenship-Generic BDocument4 pagesAffidavit of Citizenship-Generic Bdsr_prophetPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Irs ExposedDocument14 pagesIrs ExposedTRISTARUSA100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Last Year Your Client The Rattameyers Were Featured On Surprise Home Makeover A Network Television Show in Which Families Are Chosen To Receive ADocument2 pagesLast Year Your Client The Rattameyers Were Featured On Surprise Home Makeover A Network Television Show in Which Families Are Chosen To Receive ADoreenPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- RMBSA v. HDMF (333 SCRA 777) : IssueDocument4 pagesRMBSA v. HDMF (333 SCRA 777) : IssueCleofe SobiacoPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

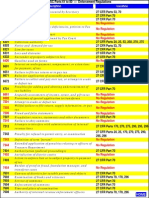

- Political Activity For A 501 C6Document66 pagesPolitical Activity For A 501 C6Barbara EspinosaPas encore d'évaluation

- A Primer On Production PaymentsDocument40 pagesA Primer On Production PaymentsST KnightPas encore d'évaluation

- Umali Vs EstanislaoDocument7 pagesUmali Vs EstanislaoKathleen Anne DangananPas encore d'évaluation

- ID: Office: Uilc: CCA - 2009022415150040 Number: 200912025 Release Date: 3/20/2009Document1 pageID: Office: Uilc: CCA - 2009022415150040 Number: 200912025 Release Date: 3/20/2009taxcrunchPas encore d'évaluation

- 2008 Spring Audit State Developments 2Document285 pages2008 Spring Audit State Developments 2rashidsfPas encore d'évaluation

- BIR Ruling (DA - (C-003) 020-10)Document2 pagesBIR Ruling (DA - (C-003) 020-10)amadieuPas encore d'évaluation

- Gary L. Stewart, Imperator of AMORC 1987-1990Document1 pageGary L. Stewart, Imperator of AMORC 1987-1990sauron385Pas encore d'évaluation

- H. R. LL: A BillDocument5 pagesH. R. LL: A Billakctan19946Pas encore d'évaluation

- Province of Misamis Oriental Vs Cagayan Electric PowerDocument4 pagesProvince of Misamis Oriental Vs Cagayan Electric PowerJDR JDRPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- USA V Jumroon PDFDocument7 pagesUSA V Jumroon PDFJustin OkunPas encore d'évaluation

- REG Study Guide 4-21-2013Document213 pagesREG Study Guide 4-21-2013Valerie ReadhimerPas encore d'évaluation

- Tax - BPI Vs CIR GR No 139736 October 17, 2005 DigestDocument9 pagesTax - BPI Vs CIR GR No 139736 October 17, 2005 DigestDyannah Alexa Marie RamachoPas encore d'évaluation

- Article in Bussiness LawDocument28 pagesArticle in Bussiness LawLey Evangelio HubayanPas encore d'évaluation

- Cagayan Electric Power vs. City of Cagayan de Oro G.R. No. 191761 November 14 2012Document9 pagesCagayan Electric Power vs. City of Cagayan de Oro G.R. No. 191761 November 14 2012MassabiellePas encore d'évaluation

- Iloilo Vs SmartDocument12 pagesIloilo Vs SmartKirsten Denise B. Habawel-VegaPas encore d'évaluation

- CFRxref PDFDocument4 pagesCFRxref PDFiamnumber8Pas encore d'évaluation

- (Ius Gentium_ Comparative Perspectives on Law and Justice 12) Karen B. Brown (auth.), Karen B. Brown (eds.)-A Comparative Look at Regulation of Corporate Tax Avoidance-Springer Netherlands (2012).pdfDocument386 pages(Ius Gentium_ Comparative Perspectives on Law and Justice 12) Karen B. Brown (auth.), Karen B. Brown (eds.)-A Comparative Look at Regulation of Corporate Tax Avoidance-Springer Netherlands (2012).pdfAsep KusnaliPas encore d'évaluation

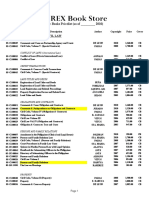

- Law Books Pricelist (As of - 2010)Document10 pagesLaw Books Pricelist (As of - 2010)Shim Lei R. ClimacoPas encore d'évaluation

- BPI vs. CIRDocument2 pagesBPI vs. CIRluckyPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- CR Vs MarubeniDocument15 pagesCR Vs MarubeniSudan TambiacPas encore d'évaluation

- 2021 Suwa - Shipyard - Machineries - Corp.20211108 12 MkhgioDocument4 pages2021 Suwa - Shipyard - Machineries - Corp.20211108 12 MkhgioLoren SanapoPas encore d'évaluation

- 31-CIR v. Batangas Transportation G.R. No. L-9692 January 6, 1958Document6 pages31-CIR v. Batangas Transportation G.R. No. L-9692 January 6, 1958wewPas encore d'évaluation