Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Financing:: 1. Role of Shareholders As StakeholdersDocument2 pagesFinancing:: 1. Role of Shareholders As Stakeholdersrammar147Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- WCPT9 Scientific Program Madrid 2022Document52 pagesWCPT9 Scientific Program Madrid 2022rammar147Pas encore d'évaluation

- Investment Scenario - : (A) FDI EQUITY INFLOWS (Equity Capital Components)Document1 pageInvestment Scenario - : (A) FDI EQUITY INFLOWS (Equity Capital Components)rammar147Pas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- A Coupled CFD Monte Carlo Method For Simulating Complex Aerosol Dynamics in Turbulent FlowsDocument14 pagesA Coupled CFD Monte Carlo Method For Simulating Complex Aerosol Dynamics in Turbulent Flowsrammar147Pas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Case Jonah Creighton: Ethics and Value Based LeadershipDocument16 pagesCase Jonah Creighton: Ethics and Value Based Leadershiprammar147Pas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- 2022 Rent Receipt 2Document1 page2022 Rent Receipt 2rammar147Pas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Volume 5 Issue 4 Paper 3Document6 pagesVolume 5 Issue 4 Paper 3Niku BandiPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Volume 5 Issue 4 Paper 3Document6 pagesVolume 5 Issue 4 Paper 3Niku BandiPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- ITC Product MixDocument47 pagesITC Product MixMohit Malviya67% (3)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

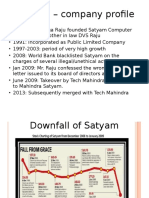

- Satyam CaseDocument4 pagesSatyam Caserammar147Pas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Financing:: 1. Role of Shareholders As StakeholdersDocument2 pagesFinancing:: 1. Role of Shareholders As Stakeholdersrammar147Pas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Leveraging: Case StudyDocument1 pageLeveraging: Case Studyrammar147Pas encore d'évaluation

- Case Study 1Document11 pagesCase Study 1Jaspal Singh100% (1)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Shielding CalculationDocument17 pagesShielding Calculationrammar147Pas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Flux Calculation Due To Non Uniform SourceDocument4 pagesFlux Calculation Due To Non Uniform Sourcerammar147Pas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Case Study 1Document11 pagesCase Study 1Jaspal Singh100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Dose Due To Cylindrical SourceDocument9 pagesDose Due To Cylindrical Sourcerammar147Pas encore d'évaluation

- Dose Due To Cylindrical SourceDocument9 pagesDose Due To Cylindrical Sourcerammar147Pas encore d'évaluation

- Dose Due To Cylindrical SourceDocument9 pagesDose Due To Cylindrical Sourcerammar147Pas encore d'évaluation

- Special RelativityDocument53 pagesSpecial RelativityAndrew Florit100% (2)

- Supersymmetry ReportDocument49 pagesSupersymmetry Reportrammar147Pas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Flux Calculation Due To Non Uniform SourceDocument4 pagesFlux Calculation Due To Non Uniform Sourcerammar147Pas encore d'évaluation

- 13 PPTGGDocument78 pages13 PPTGGأحمدآلزهوPas encore d'évaluation

- Semiconductor PN JunctionDocument19 pagesSemiconductor PN Junctionrammar147Pas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Fmradio 1111 PDFDocument7 pagesFmradio 1111 PDFVikiVikiPas encore d'évaluation

- Mco 07Document4 pagesMco 07rammar147Pas encore d'évaluation

- 1 - 0 Answers Progress: To Check YourDocument26 pages1 - 0 Answers Progress: To Check YourvimalbakshiPas encore d'évaluation

- Introduction To MarketingDocument18 pagesIntroduction To Marketingsabyasachi samalPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Power DomiLED InGaN DWZB UJG (3J8L) Catalogue-V1Document15 pagesPower DomiLED InGaN DWZB UJG (3J8L) Catalogue-V1Kuba KozerskiPas encore d'évaluation

- Question & Answer - Module 1 NACEDocument6 pagesQuestion & Answer - Module 1 NACEraghuvarma0% (1)

- Devlopment and Analysis of Natural Banana Fiber CompositeDocument3 pagesDevlopment and Analysis of Natural Banana Fiber CompositeEditor IJRITCCPas encore d'évaluation

- Demand Control Ventilation Benefits For Your Building: White Paper SeriesDocument6 pagesDemand Control Ventilation Benefits For Your Building: White Paper Serieshb_scribPas encore d'évaluation

- Informacion Tecnica Valvula Motora Gas de AltaDocument8 pagesInformacion Tecnica Valvula Motora Gas de AltaGuille MVPas encore d'évaluation

- TB 213 Engineering Guide On Earthing Systems in Power Stations - PeiDocument6 pagesTB 213 Engineering Guide On Earthing Systems in Power Stations - Peifgdfgdf0% (1)

- Cepe BomDocument8 pagesCepe BomRomeo AtienzaPas encore d'évaluation

- Dupont Tyvek BrochureDocument4 pagesDupont Tyvek BrochureAugustin MacoveiPas encore d'évaluation

- WTP 3032 Painting WorksDocument9 pagesWTP 3032 Painting WorksWan AnisPas encore d'évaluation

- Kitchen Mood BoardDocument9 pagesKitchen Mood BoardKelly CantaraPas encore d'évaluation

- Interbond 600 PDFDocument4 pagesInterbond 600 PDFTrịnh Minh KhoaPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Welcome Newcomer To SLPDocument10 pagesWelcome Newcomer To SLPnxgenoePas encore d'évaluation

- M1 Installation ManualDocument72 pagesM1 Installation ManualGary IrvingPas encore d'évaluation

- Practical Action How To Make Stabilised Earth BlocksDocument14 pagesPractical Action How To Make Stabilised Earth BlocksPeter W Gossner100% (1)

- Panasonic Bathroom Fan Heater Combo Service ManualDocument15 pagesPanasonic Bathroom Fan Heater Combo Service ManualddPas encore d'évaluation

- (PDF) UAP Doc 401-402Document17 pages(PDF) UAP Doc 401-402stanflynnPas encore d'évaluation

- CN 7001 Advanced Concrete Technology1Document3 pagesCN 7001 Advanced Concrete Technology1Karthik NatesanPas encore d'évaluation

- Alfa Laval Separator Course Specification PDFDocument9 pagesAlfa Laval Separator Course Specification PDFGerald Campañano100% (2)

- BoM For TransformerDocument24 pagesBoM For TransformeritsmercyadavPas encore d'évaluation

- Industrial Training Report: Department of Mechanical EngineeringDocument32 pagesIndustrial Training Report: Department of Mechanical EngineeringParul Chhabra67% (3)

- R3G310AJ3861 DigitalDocument11 pagesR3G310AJ3861 DigitalmucorPas encore d'évaluation

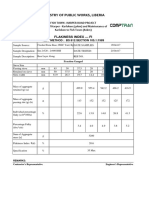

- Ministry of Public Works, Liberia: Flakiness Index - FiDocument2 pagesMinistry of Public Works, Liberia: Flakiness Index - FikwamePas encore d'évaluation

- Scada Specification Rdso DocumentDocument35 pagesScada Specification Rdso DocumentbhaskarjalanPas encore d'évaluation

- ACI 517 2 1992 Accelerated Curing of Concrete at Atmospheric Pressure PDFDocument17 pagesACI 517 2 1992 Accelerated Curing of Concrete at Atmospheric Pressure PDFHaniAminPas encore d'évaluation

- Parts List FerraraDocument8 pagesParts List Ferraramark_59Pas encore d'évaluation

- Switched Reluctance Motor 17 I TaeDocument114 pagesSwitched Reluctance Motor 17 I TaeAnonymous zzfx7mz3Pas encore d'évaluation

- VK-P Series Tsi Transducer Model Vk-143P Transducer Instruction ManualDocument53 pagesVK-P Series Tsi Transducer Model Vk-143P Transducer Instruction Manualravi_fdPas encore d'évaluation

- Excavator Sop PDFDocument1 pageExcavator Sop PDFhengky achmadPas encore d'évaluation

- Candidate Registration DetailsDocument229 pagesCandidate Registration Detailsphone2hirePas encore d'évaluation

- (Paper) Jack Down Construction MethodDocument6 pages(Paper) Jack Down Construction MethodShaileshRastogiPas encore d'évaluation