Vous aimerez peut-être aussi

- AICPA - CPA Reg 2017Document12 pagesAICPA - CPA Reg 2017Gene'sPas encore d'évaluation

- 2021 2nd AC - Acctg Gov Quiz 04Document4 pages2021 2nd AC - Acctg Gov Quiz 04Merliza JusayanPas encore d'évaluation

- FABM1 Quarter 1 Week 3Document47 pagesFABM1 Quarter 1 Week 3FERNANDO TAMZ2003Pas encore d'évaluation

- Questions & Answers: For Camp InvestorsDocument1 pageQuestions & Answers: For Camp Investorsapi-238524059Pas encore d'évaluation

- Business Tax Activity 1Document10 pagesBusiness Tax Activity 1Michael AquinoPas encore d'évaluation

- Mock Exam - Revision 1Document15 pagesMock Exam - Revision 1Quỳnh VõPas encore d'évaluation

- Coverage of The Tax "Gifts"Document3 pagesCoverage of The Tax "Gifts"Jeneth OrtuaPas encore d'évaluation

- DonorsDocument11 pagesDonorsboniglai50% (1)

- Tax ComprehensiveDocument11 pagesTax ComprehensiveDawn digolPas encore d'évaluation

- Basic Concept of Donation and Donor's TaxDocument20 pagesBasic Concept of Donation and Donor's TaxKarl BasaPas encore d'évaluation

- Business TaxDocument19 pagesBusiness TaxMichael AquinoPas encore d'évaluation

- Quiz Inter2Document2 pagesQuiz Inter2Dea Aulia AmanahPas encore d'évaluation

- NPO AssignmentDocument4 pagesNPO AssignmentZyrah Mae SaezPas encore d'évaluation

- B) in The Case of Gifts Made by A Nonresident Not A Citizen of The PhilippinesDocument23 pagesB) in The Case of Gifts Made by A Nonresident Not A Citizen of The PhilippinesNissi JonnaPas encore d'évaluation

- KatolDocument5 pagesKatoljemPas encore d'évaluation

- AFAR-non ProfitDocument21 pagesAFAR-non ProfitJessica Pama EstandartePas encore d'évaluation

- Quiz POPDocument2 pagesQuiz POPKarina RachmaPas encore d'évaluation

- Donors TaxDocument4 pagesDonors TaxRo-Anne LozadaPas encore d'évaluation

- CH 4 & 5 Extra Practic Summer 2023Document9 pagesCH 4 & 5 Extra Practic Summer 2023Ruth KatakaPas encore d'évaluation

- Test MidtermDocument4 pagesTest MidtermcirujeffPas encore d'évaluation

- Tax2 Bar QsDocument7 pagesTax2 Bar QsAlex RabanesPas encore d'évaluation

- Fundamentals of Financial AccountingDocument9 pagesFundamentals of Financial AccountingEmon EftakarPas encore d'évaluation

- Accounting Tutorial 1Document2 pagesAccounting Tutorial 1AmalinaIsaPas encore d'évaluation

- Howes Tax 2013 Charitable Contributions GuideDocument2 pagesHowes Tax 2013 Charitable Contributions GuideShawn M. CoxPas encore d'évaluation

- Western Leyte College of Ormoc, Inc. Prelim Exam in Taxation I October 10, 2020Document2 pagesWestern Leyte College of Ormoc, Inc. Prelim Exam in Taxation I October 10, 2020Marc William SorianoPas encore d'évaluation

- AssignmentDocument2 pagesAssignmentLois JosePas encore d'évaluation

- Taxation Law 1 Compiled QuestionsDocument4 pagesTaxation Law 1 Compiled QuestionsTiffany HuntPas encore d'évaluation

- Test QuestionsDocument24 pagesTest Questionsjmp8888Pas encore d'évaluation

- Harvard Financial Accounting Final Exam 3Document10 pagesHarvard Financial Accounting Final Exam 3Bharathi Raju25% (4)

- Condonation or Cancellation of IndebtednessDocument4 pagesCondonation or Cancellation of IndebtednessArceño, Advrelyn Frances C.Pas encore d'évaluation

- Home Fin HelpDocument14 pagesHome Fin HelpBharathi RajuPas encore d'évaluation

- Accounting For Non Profit Making Organisations PDFDocument23 pagesAccounting For Non Profit Making Organisations PDFrain06021992Pas encore d'évaluation

- 02 Exercises - Accounting For NPOs v2Document3 pages02 Exercises - Accounting For NPOs v2Peter Andre GuintoPas encore d'évaluation

- TAX 2 BAR Q&A For MidtermDocument5 pagesTAX 2 BAR Q&A For MidtermMike E DmPas encore d'évaluation

- Assignment No.2Document5 pagesAssignment No.2mohamed atlamPas encore d'évaluation

- Donor's TaxDocument5 pagesDonor's TaxKeithPas encore d'évaluation

- Harvard Financial Accounting Final Exam 3Document11 pagesHarvard Financial Accounting Final Exam 3Bharathi Raju0% (1)

- 1)Document2 pages1)Tom BinfieldPas encore d'évaluation

- Financial&managerial Accounting - 15e Williamshakabettner Chap 6Document15 pagesFinancial&managerial Accounting - 15e Williamshakabettner Chap 6mzqace100% (1)

- Mock Test 1Document20 pagesMock Test 1Quỳnh'ss Đắc'ssPas encore d'évaluation

- DT1Document5 pagesDT1iris claire gamadPas encore d'évaluation

- 1 The Jones Family Lost Its Home in A Fire: Unlock Answers Here Solutiondone - OnlineDocument1 page1 The Jones Family Lost Its Home in A Fire: Unlock Answers Here Solutiondone - Onlinetrilocksp SinghPas encore d'évaluation

- On The First Day of Year 4 The City Receives: Unlock Answers Here Solutiondone - OnlineDocument1 pageOn The First Day of Year 4 The City Receives: Unlock Answers Here Solutiondone - Onlinetrilocksp SinghPas encore d'évaluation

- Audit & Assurance 1 Test 1 2022Document3 pagesAudit & Assurance 1 Test 1 2022kp107416Pas encore d'évaluation

- Solutiondone 2-457Document1 pageSolutiondone 2-457trilocksp SinghPas encore d'évaluation

- DONORS TAX and ESTATE TAXDocument39 pagesDONORS TAX and ESTATE TAXmarjorie blancoPas encore d'évaluation

- Sample FinalDocument18 pagesSample FinalDavid MendietaPas encore d'évaluation

- Chapter 10 HWDocument6 pagesChapter 10 HWAlysha Harvey EAPas encore d'évaluation

- Question and Answer - 8Document30 pagesQuestion and Answer - 8acc-expertPas encore d'évaluation

- Accounting II-Review Chapters12,13,14 (8thed)Document10 pagesAccounting II-Review Chapters12,13,14 (8thed)JacKFrost1889Pas encore d'évaluation

- MidTerm ExamDocument15 pagesMidTerm ExamYonatan Wadler100% (2)

- Donors TaxDocument4 pagesDonors TaxTrisha Nicole FloresPas encore d'évaluation

- Policy5 Fundraising Legal and Ethical PracticesDocument2 pagesPolicy5 Fundraising Legal and Ethical PracticesWood River Land TrustPas encore d'évaluation

- Taxation 2023 QuestionsDocument5 pagesTaxation 2023 QuestionsjanaPas encore d'évaluation

- Tax 2 Reviewer LectureDocument13 pagesTax 2 Reviewer LectureShiela May Agustin MacarayanPas encore d'évaluation

- MSJG Chap 1 10 QuestionsDocument6 pagesMSJG Chap 1 10 QuestionsMar Sean Jan Gabiosa100% (2)

- 401(k) Plans Made Easy: Understanding Your 401(k) PlanD'Everand401(k) Plans Made Easy: Understanding Your 401(k) PlanPas encore d'évaluation

- J.K. Lasser's 1001 Deductions and Tax Breaks 2009: Your Complete Guide to Everything DeductibleD'EverandJ.K. Lasser's 1001 Deductions and Tax Breaks 2009: Your Complete Guide to Everything DeductibleÉvaluation : 3 sur 5 étoiles3/5 (1)

- The Encyclopedia of Real Estate Forms & Agreements: A Complete Kit of Ready-to-Use Checklists, Worksheets, Forms, and ContractsD'EverandThe Encyclopedia of Real Estate Forms & Agreements: A Complete Kit of Ready-to-Use Checklists, Worksheets, Forms, and ContractsPas encore d'évaluation

- 201 FormDocument16 pages201 FormJennylyn DoronioPas encore d'évaluation

- Manahan v. FloresDocument3 pagesManahan v. FloresbrownboomerangPas encore d'évaluation

- Gonzales Vs CaDocument2 pagesGonzales Vs CaReth GuevarraPas encore d'évaluation

- TOMAS LAO CONSTRUCTION VsDocument2 pagesTOMAS LAO CONSTRUCTION Vshime mej100% (2)

- Causes of Failure of League of Nations: 1. Absence of Great PowersDocument4 pagesCauses of Failure of League of Nations: 1. Absence of Great PowersTAYYAB ABBAS QURESHIPas encore d'évaluation

- Human Rights in Undp: Practice NoteDocument29 pagesHuman Rights in Undp: Practice NoteVipul GautamPas encore d'évaluation

- Plea BargainingDocument10 pagesPlea Bargainingtunkucute05Pas encore d'évaluation

- 9 - The Confederation and The Constitution, 1776 - 1790Document111 pages9 - The Confederation and The Constitution, 1776 - 1790dssguy99Pas encore d'évaluation

- Bail 23 A Sindh Arms Act HC KarachiDocument3 pagesBail 23 A Sindh Arms Act HC Karachilittle hopePas encore d'évaluation

- A Paramilitary Policing JuggernautDocument17 pagesA Paramilitary Policing JuggernautFranklinBarrientosRamirezPas encore d'évaluation

- Chapter-4: Programme of Law Reform (1999) Pp. 18 and 43Document72 pagesChapter-4: Programme of Law Reform (1999) Pp. 18 and 43Humanyu KabeerPas encore d'évaluation

- Catiis v. CADocument1 pageCatiis v. CAMia AngelaPas encore d'évaluation

- Areola Vs CADocument2 pagesAreola Vs CAEarlcen MinorcaPas encore d'évaluation

- Free Look Period:: Life Insurance Corporation of IndiaDocument2 pagesFree Look Period:: Life Insurance Corporation of IndiaDebendra nayakPas encore d'évaluation

- Sample Quiz 4 On ObliconDocument4 pagesSample Quiz 4 On ObliconRegina MuellerPas encore d'évaluation

- Sample Document: Prenuptial AgreementDocument3 pagesSample Document: Prenuptial AgreementEulaArias JuanPabloPas encore d'évaluation

- Background of Company LawDocument30 pagesBackground of Company LawsidaneyPas encore d'évaluation

- Lastra Professional EthicsDocument5 pagesLastra Professional EthicsFederico R LastraPas encore d'évaluation

- Order Granting Release of Austin Harrouff's Interview With The 'Dr. Phil Show'Document7 pagesOrder Granting Release of Austin Harrouff's Interview With The 'Dr. Phil Show'WXYZ-TV Channel 7 DetroitPas encore d'évaluation

- Flynote: HeadnoteDocument6 pagesFlynote: HeadnoteFrancis Phiri100% (1)

- Elliot Currie Su Left RealismDocument15 pagesElliot Currie Su Left RealismFranklinBarrientosRamirezPas encore d'évaluation

- Household Helpers Entitled To 13th Month Pay Under The LawDocument1 pageHousehold Helpers Entitled To 13th Month Pay Under The Lawyurets929Pas encore d'évaluation

- Tavaana Exclusive Case Study: The Velvet Revolution - A Peaceful End To Communism in CzechoslovakiaDocument9 pagesTavaana Exclusive Case Study: The Velvet Revolution - A Peaceful End To Communism in CzechoslovakiaTavaana E-InstitutePas encore d'évaluation

- Elisco Vs CADocument6 pagesElisco Vs CAjessapuerinPas encore d'évaluation

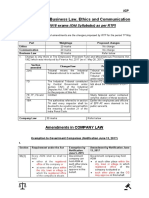

- Amendments in Business Law, Ethics and Communication: (For May 2018 Exams (Old Syllabubs) As Per RTP)Document3 pagesAmendments in Business Law, Ethics and Communication: (For May 2018 Exams (Old Syllabubs) As Per RTP)Neha jainPas encore d'évaluation

- Land Bank of The Philippines V Belle CorpDocument2 pagesLand Bank of The Philippines V Belle CorpDan Marco GriartePas encore d'évaluation

- Polity Study PlanDocument8 pagesPolity Study Plansarwat fatmaPas encore d'évaluation

- Ablaza v. RepublicDocument8 pagesAblaza v. Republiclavyne56Pas encore d'évaluation

- M.P.warehousng & Logistics Policy 2012 Rules - EnglishDocument6 pagesM.P.warehousng & Logistics Policy 2012 Rules - EnglishSantoshh MishhPas encore d'évaluation