Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Commercial Arithmetic PDFDocument8 pagesCommercial Arithmetic PDFagnelwaghelaPas encore d'évaluation

- User Guide - Pastel Partner Version 11Document232 pagesUser Guide - Pastel Partner Version 11erostyles100% (1)

- Iiqe Paper 3 Pastpaper 20200518Document20 pagesIiqe Paper 3 Pastpaper 20200518Tsz Ngong Ko100% (1)

- Primer On TrustsDocument15 pagesPrimer On TrustsAnkur LakhaniPas encore d'évaluation

- Donor's Tax TRAIN LAWDocument4 pagesDonor's Tax TRAIN LAWJenMarlon Corpuz Aquino100% (1)

- C.T.A. Case No. 9076 - Keansburg Marketing Corp. v. CIRDocument31 pagesC.T.A. Case No. 9076 - Keansburg Marketing Corp. v. CIRcaren kay b. adolfoPas encore d'évaluation

- IFRS Cover ArticleDocument2 pagesIFRS Cover ArticleerostylesPas encore d'évaluation

- F6zaf sg2012Document13 pagesF6zaf sg2012erostylesPas encore d'évaluation

- IFRS BookletDocument32 pagesIFRS BookleterostylesPas encore d'évaluation

- Director's Remuneration - PayeDocument11 pagesDirector's Remuneration - PayeerostylesPas encore d'évaluation

- 0 Rule Amendments 12 October 20071Document20 pages0 Rule Amendments 12 October 20071erostylesPas encore d'évaluation

- EMP101eV3.01020100630PUBLISHDocument7 pagesEMP101eV3.01020100630PUBLISHerostylesPas encore d'évaluation

- EMP101eApplicationforRegistrationPAYESDLUIFForm1Document5 pagesEMP101eApplicationforRegistrationPAYESDLUIFForm1erostylesPas encore d'évaluation

- SE-EXC-24 - Tobacco Industry - External PolicyDocument3 pagesSE-EXC-24 - Tobacco Industry - External PolicyerostylesPas encore d'évaluation

- EMP101eV3.01020100630PUBLISHDocument7 pagesEMP101eV3.01020100630PUBLISHerostylesPas encore d'évaluation

- ASPAYE05G3GuideforEmployersiroAllowancesRev02010.03.01Document12 pagesASPAYE05G3GuideforEmployersiroAllowancesRev02010.03.01erostylesPas encore d'évaluation

- VAT Guidelines 2010Document106 pagesVAT Guidelines 2010erostyles100% (1)

- ASPAYE05A8CalculationExamplesRelatingtoFringeBenefits1March2007Document4 pagesASPAYE05A8CalculationExamplesRelatingtoFringeBenefits1March2007erostylesPas encore d'évaluation

- ASPAYE05GuideforEmployersi.r.oEmployeesTax1March2006Document61 pagesASPAYE05GuideforEmployersi.r.oEmployeesTax1March2006erostylesPas encore d'évaluation

- VAT Guidelines 2010Document106 pagesVAT Guidelines 2010erostyles100% (1)

- ASPAYE05GuideForEmployersinrespectofEmployeesTax1March2007Document58 pagesASPAYE05GuideForEmployersinrespectofEmployeesTax1March2007erostylesPas encore d'évaluation

- 4912 TP01RegistrationasaTaxPractitionerorchangeofregisteredparticularsDocument2 pages4912 TP01RegistrationasaTaxPractitionerorchangeofregisteredparticularserostylesPas encore d'évaluation

- Difference Bill NewDocument76 pagesDifference Bill NewMuneeb Usmani100% (1)

- Manish Dua: Brand Manish Dua Questions For Ca-Cpt (Economics)Document48 pagesManish Dua: Brand Manish Dua Questions For Ca-Cpt (Economics)gagan vermaPas encore d'évaluation

- Whistleblower ComplaintDocument7 pagesWhistleblower ComplaintThe FederalistPas encore d'évaluation

- Analysis: Systems Tool For Urban PlanningDocument8 pagesAnalysis: Systems Tool For Urban PlanninglalecrimPas encore d'évaluation

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismARJUNPas encore d'évaluation

- Sept 2011 Part III InsightDocument67 pagesSept 2011 Part III InsightLegogie Moses AnoghenaPas encore d'évaluation

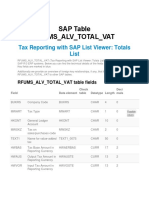

- RFUMSDocument2 pagesRFUMSSivakumar ThangarajanPas encore d'évaluation

- Klash Private Limited Balance Sheet and Profit Loss AccountDocument2 pagesKlash Private Limited Balance Sheet and Profit Loss AccountAbdullahPas encore d'évaluation

- 2011 PTD (Trib.) 936 PDFDocument13 pages2011 PTD (Trib.) 936 PDFMuhammad Ilyas ShafiqPas encore d'évaluation

- Tradução de Imposto de Renda (Faculdade)Document2 pagesTradução de Imposto de Renda (Faculdade)Jackson RodrigoPas encore d'évaluation

- AssesmentDocument12 pagesAssesmentMaya Keizel A.Pas encore d'évaluation

- Request For Transcript of Tax Return: Sign HereDocument2 pagesRequest For Transcript of Tax Return: Sign HereAnonymous OSyY7VPas encore d'évaluation

- Lazaro Hernandez Roque 6751 W Indian School RD PHOENIX, AZ 85033Document2 pagesLazaro Hernandez Roque 6751 W Indian School RD PHOENIX, AZ 85033Rielzaruxo Ka Rioelzarux Ko XPas encore d'évaluation

- Investment Analysis and Portfolio Management: Eighth Edition by Frank K. Reilly & Keith C. BrownDocument56 pagesInvestment Analysis and Portfolio Management: Eighth Edition by Frank K. Reilly & Keith C. BrownPayal MehtaPas encore d'évaluation

- Dawood KhanDocument2 pagesDawood KhanRana Sunny KhokharPas encore d'évaluation

- Offer LetterDocument4 pagesOffer LetterRavi TejaPas encore d'évaluation

- V1 Exam 1AMDocument19 pagesV1 Exam 1AMatmankhaiPas encore d'évaluation

- Estate TaxDocument4 pagesEstate TaxRichel888Pas encore d'évaluation

- RMC No. 80-2021Document2 pagesRMC No. 80-2021REX FABERPas encore d'évaluation

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruSubhendu NathPas encore d'évaluation

- ECONOMICS P1 M18 To J22 C.VDocument428 pagesECONOMICS P1 M18 To J22 C.VsukaPas encore d'évaluation

- 2023 02 06 Media Statement Minerals Council Pubishes Facts and Figures 2022Document3 pages2023 02 06 Media Statement Minerals Council Pubishes Facts and Figures 2022RehanPas encore d'évaluation

- Nature of Excise DutyDocument16 pagesNature of Excise DutyVinod PatelPas encore d'évaluation

- CEO CompensationDocument27 pagesCEO CompensationmummimPas encore d'évaluation

- Niti Aayog - Final Report - Transforming Indias Gold Market 2018 MarchDocument200 pagesNiti Aayog - Final Report - Transforming Indias Gold Market 2018 MarchD D KarelPas encore d'évaluation