Vous aimerez peut-être aussi

- Sample Contract To SellDocument3 pagesSample Contract To SellCandice Tongco-Cruz100% (4)

- Day 1Document11 pagesDay 1Abdullah EjazPas encore d'évaluation

- Module 1 - FA at FVDocument5 pagesModule 1 - FA at FVNorfaidah Didato GogoPas encore d'évaluation

- Voucher SystemDocument2 pagesVoucher Systemnatalie_sportyPas encore d'évaluation

- Foreign Currency TranslationDocument38 pagesForeign Currency TranslationAnmol Gulati100% (1)

- Ias 37 Provisions Contingent Liabilities and Contingent Assets SummaryDocument5 pagesIas 37 Provisions Contingent Liabilities and Contingent Assets SummaryChristian Dela Pena67% (3)

- Corporate Finance Theory and Practice 10th EditionDocument674 pagesCorporate Finance Theory and Practice 10th EditionrahafPas encore d'évaluation

- Isb540 - HiwalahDocument16 pagesIsb540 - HiwalahMahyuddin Khalid100% (1)

- Ramo 1-2019Document74 pagesRamo 1-2019Donato Vergara IIIPas encore d'évaluation

- IntangiblesDocument7 pagesIntangiblesWertdie stanPas encore d'évaluation

- Chapter - 8Document26 pagesChapter - 8Rathnakar SarmaPas encore d'évaluation

- Pas 20, 23Document32 pagesPas 20, 23Angela WaganPas encore d'évaluation

- Trade Receivable & AllowancesDocument7 pagesTrade Receivable & Allowancesmobylay0% (1)

- Cash Vs Accrual Accounting 1Document65 pagesCash Vs Accrual Accounting 1Nassir CeellaabePas encore d'évaluation

- Module1 - Foreign Currency Transaction and TranslationDocument3 pagesModule1 - Foreign Currency Transaction and TranslationGerome Echano0% (1)

- Chapter 18 IAS 2 InventoriesDocument6 pagesChapter 18 IAS 2 InventoriesKelvin Chu JYPas encore d'évaluation

- Toa Interim ReportingDocument17 pagesToa Interim ReportingEmmanuel SarmientoPas encore d'évaluation

- Chapter Two LatestDocument13 pagesChapter Two LatestOwolabi PetersPas encore d'évaluation

- M1 - Introduction To Valuation HandoutDocument6 pagesM1 - Introduction To Valuation HandoutPrince LeePas encore d'évaluation

- Accounting For Income TaxesDocument4 pagesAccounting For Income TaxesDivine CuasayPas encore d'évaluation

- Management Accounting Chap 003Document67 pagesManagement Accounting Chap 003kenha2000Pas encore d'évaluation

- IFRS 15 RevenueDocument8 pagesIFRS 15 RevenueEmezi Francis ObisikePas encore d'évaluation

- Depreciation Accounting PDFDocument42 pagesDepreciation Accounting PDFASIFPas encore d'évaluation

- PartnershipsDocument27 pagesPartnershipssamuel debebePas encore d'évaluation

- IAS 40 - Investment PropertyDocument6 pagesIAS 40 - Investment PropertyAllana NicdaoPas encore d'évaluation

- Audit II 7new - 3Document15 pagesAudit II 7new - 3Muktar Xahaa100% (1)

- Kinney 8e - CH 09Document17 pagesKinney 8e - CH 09Ashik Uz ZamanPas encore d'évaluation

- Financial Statements Are A Collection of SummaryDocument10 pagesFinancial Statements Are A Collection of Summarygbless ceasarPas encore d'évaluation

- IAS 1 Presentations of Financial StatementsDocument3 pagesIAS 1 Presentations of Financial StatementsPradyut KumarPas encore d'évaluation

- Impairment of Assets - IAS 36Document17 pagesImpairment of Assets - IAS 36charanteja9Pas encore d'évaluation

- Ias 20 Accounting For Government Grants and Disclosure of Government Assistance SummaryDocument5 pagesIas 20 Accounting For Government Grants and Disclosure of Government Assistance SummaryKenncyPas encore d'évaluation

- ch03 SM Leo 10eDocument72 pagesch03 SM Leo 10ePyae PhyoPas encore d'évaluation

- Financial Reporting and Changing PricesDocument6 pagesFinancial Reporting and Changing PricesFia RahmaPas encore d'évaluation

- Accounting Adjustments and Constructing The Financial StatementsDocument12 pagesAccounting Adjustments and Constructing The Financial StatementsKwaku DanielPas encore d'évaluation

- Property, Plant and EquipmentDocument6 pagesProperty, Plant and EquipmenthemantbaidPas encore d'évaluation

- IAS-16 (Property, Plant & Equipment)Document20 pagesIAS-16 (Property, Plant & Equipment)Nazmul HaquePas encore d'évaluation

- Risk ResponseDocument4 pagesRisk ResponseLevi AckermannPas encore d'évaluation

- Revenue From Contracts With CustomersDocument21 pagesRevenue From Contracts With Customersnot mePas encore d'évaluation

- Chapter 2 - Determinants of Interest RatesDocument3 pagesChapter 2 - Determinants of Interest RatesJean Stephany100% (1)

- EU Directive On Disclosure of Non-Financial and Diversity InformationDocument28 pagesEU Directive On Disclosure of Non-Financial and Diversity InformationLUCIAN GOGUPas encore d'évaluation

- Auditing Chapter 3Document38 pagesAuditing Chapter 3FarrukhsgPas encore d'évaluation

- Responsibility and Segment Accounting CRDocument24 pagesResponsibility and Segment Accounting CRAshy LeePas encore d'évaluation

- Section VI: NRV Vs Fair Value: ExampleDocument5 pagesSection VI: NRV Vs Fair Value: ExamplebinuPas encore d'évaluation

- Ias-40 - Investment PropertyDocument16 pagesIas-40 - Investment PropertyPue Das100% (2)

- Ch18 - 2 - Accounting For Revenue Recognition IssuesDocument45 pagesCh18 - 2 - Accounting For Revenue Recognition Issuesselvy anaPas encore d'évaluation

- Chapter One Accounting Principles and Professional PracticeDocument22 pagesChapter One Accounting Principles and Professional PracticeHussen Abdulkadir100% (1)

- Chap 24 - Investment in Associate - Basic Principle Fin Acct 1 - Barter Summary Team PDFDocument5 pagesChap 24 - Investment in Associate - Basic Principle Fin Acct 1 - Barter Summary Team PDFSuper JhedPas encore d'évaluation

- Cash Cash Equivalents: Philippine Accounting Standards 7 Statement of Cash FlowsDocument2 pagesCash Cash Equivalents: Philippine Accounting Standards 7 Statement of Cash FlowsTrisha AlaPas encore d'évaluation

- Week 1 Conceptual Framework For Financial ReportingDocument17 pagesWeek 1 Conceptual Framework For Financial ReportingSHANE NAVARROPas encore d'évaluation

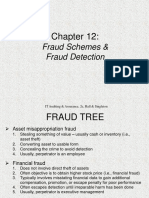

- Ch12 Fraud Scheme DetectionDocument18 pagesCh12 Fraud Scheme DetectionPanda BoarsPas encore d'évaluation

- WRD 27e - IE PPT - Ch03 - ADADocument60 pagesWRD 27e - IE PPT - Ch03 - ADAYuchen WangPas encore d'évaluation

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument38 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont Collegee s tPas encore d'évaluation

- Advance Chapter 1Document16 pagesAdvance Chapter 1abel habtamuPas encore d'évaluation

- Accounting Information SystemDocument24 pagesAccounting Information Systembea6089Pas encore d'évaluation

- Chapter 22Document19 pagesChapter 22Betelehem GebremedhinPas encore d'évaluation

- Effective Financial Statement Analysis Requires An Understanding of A Firm S Economic CharacteristicDocument1 pageEffective Financial Statement Analysis Requires An Understanding of A Firm S Economic CharacteristicM Bilal SaleemPas encore d'évaluation

- Impairment of AssetsDocument4 pagesImpairment of AssetsNath BongalonPas encore d'évaluation

- ch05 SM Leo 10eDocument31 pagesch05 SM Leo 10ePyae Phyo100% (2)

- Adv Fa I CH 1Document30 pagesAdv Fa I CH 1Addi Såïñt GeorgePas encore d'évaluation

- Borrowing Cost PDFDocument2 pagesBorrowing Cost PDFVillaruz Shereen MaePas encore d'évaluation

- Notre Dame University College of Business and Accountancy Cotabato CityDocument10 pagesNotre Dame University College of Business and Accountancy Cotabato CityKarenmae Casas IntangPas encore d'évaluation

- Income Tax: Year of Assessment 2009 - 2010 Return of Income - CompanyDocument6 pagesIncome Tax: Year of Assessment 2009 - 2010 Return of Income - CompanyYogeeta RughooPas encore d'évaluation

- Business Expense List: A. Expenses AmountDocument2 pagesBusiness Expense List: A. Expenses AmountMoutazMohsenPas encore d'évaluation

- Profit and Loss StatementDocument1 pageProfit and Loss StatementAladeenPas encore d'évaluation

- On MAT and AMT WRO0533356 - FinalDocument25 pagesOn MAT and AMT WRO0533356 - FinalOffensive SeriesPas encore d'évaluation

- DirectoryDocument2 pagesDirectoryapi-268301176Pas encore d'évaluation

- TallyPrime Essential Level 2Document26 pagesTallyPrime Essential Level 2Lavanya TPas encore d'évaluation

- SAP MiningDocument2 pagesSAP Miningsaikiran100% (1)

- Ra 6977Document12 pagesRa 6977Kobe MambaPas encore d'évaluation

- Z003800101201740141305080572 448187Document51 pagesZ003800101201740141305080572 448187Dian AnitaPas encore d'évaluation

- (Sarvesh Dhatrak) Derivatives in Stock Market and Their Importance in HedgingDocument79 pages(Sarvesh Dhatrak) Derivatives in Stock Market and Their Importance in Hedgingsarvesh dhatrakPas encore d'évaluation

- BobredDocument430 pagesBobredNikunj OlpadwalaPas encore d'évaluation

- Karla Company P-WPS OfficeDocument14 pagesKarla Company P-WPS OfficeKris Van HalenPas encore d'évaluation

- 2307 For EBS Private Individual Percenateg TaxDocument4 pages2307 For EBS Private Individual Percenateg TaxAGrace MercadoPas encore d'évaluation

- Jabatan Bendahari: Tarikh Kredit Debit Keterangan Nombor Rujukan KampusDocument1 pageJabatan Bendahari: Tarikh Kredit Debit Keterangan Nombor Rujukan KampusArief HakimiPas encore d'évaluation

- Coi Ay 22-23Document2 pagesCoi Ay 22-23vikash pandeyPas encore d'évaluation

- GA502166-New Policy Welcome LetterDocument1 pageGA502166-New Policy Welcome LetterNelly HPas encore d'évaluation

- List of Groups and Topic For Practical Assignment 1Document5 pagesList of Groups and Topic For Practical Assignment 1pareek gopalPas encore d'évaluation

- Rental AgreementDocument2 pagesRental AgreementKipyegon CheruiyotPas encore d'évaluation

- The - Faber.report CNBSDocument154 pagesThe - Faber.report CNBSWilly Pérez-Barreto MaturanaPas encore d'évaluation

- Employees' Provident Fund Scheme: (0.18 %)Document9 pagesEmployees' Provident Fund Scheme: (0.18 %)Shubhabrata BanerjeePas encore d'évaluation

- Suppose The Government Borrows 20 Billion More Next Year ThanDocument2 pagesSuppose The Government Borrows 20 Billion More Next Year ThanMiroslav GegoskiPas encore d'évaluation

- Testing Point FigureDocument4 pagesTesting Point Figureshares_leonePas encore d'évaluation

- School Building Valuation in Rural AreasDocument66 pagesSchool Building Valuation in Rural AreasMurthy BabuPas encore d'évaluation

- Financial Daily: Putrajaya Files Rm680M Forfeiture ActionDocument33 pagesFinancial Daily: Putrajaya Files Rm680M Forfeiture ActionPG ChongPas encore d'évaluation

- Transfer Pricing II: Rajan Baa 3257Document15 pagesTransfer Pricing II: Rajan Baa 3257Rajan BaaPas encore d'évaluation

- UntitledDocument3 pagesUntitledapi-234474152Pas encore d'évaluation

- Jean Keating and Jack SmithDocument10 pagesJean Keating and Jack SmithStephen Monaghan100% (2)

- Audit Problems CashDocument18 pagesAudit Problems CashYenelyn Apistar Cambarijan0% (1)

- Syllabus For Sap Fico TrainingDocument8 pagesSyllabus For Sap Fico TrainingManoj KumarPas encore d'évaluation