Vous aimerez peut-être aussi

- Logic and Critical ThinkingDocument24 pagesLogic and Critical ThinkingAhmed Ali Khan100% (1)

- Absorption & Marginal CostingDocument17 pagesAbsorption & Marginal CostingAhmed Ali KhanPas encore d'évaluation

- Absorption & Marginal Costing - Noor Alam (MC16-103)Document24 pagesAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- Absorption & Marginal Costing - Noor Alam (MC16-103)Document24 pagesAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Quest 1Document7 pagesQuest 1btetarbePas encore d'évaluation

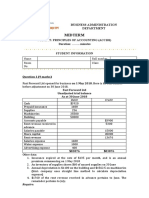

- Midterm: Hoa Lac Subject: Principles of Accounting (Acc101) Duration: .. Minutes Student InformationDocument2 pagesMidterm: Hoa Lac Subject: Principles of Accounting (Acc101) Duration: .. Minutes Student InformationNguyen Ngoc Minh Chau (K15 HL)Pas encore d'évaluation

- Ebook Cornerstones of Managerial Accounting Canadian 3Rd Edition Mowen Solutions Manual Full Chapter PDFDocument51 pagesEbook Cornerstones of Managerial Accounting Canadian 3Rd Edition Mowen Solutions Manual Full Chapter PDFxaviaalexandrawp86i100% (12)

- Accounts Form 4 - 2021Document51 pagesAccounts Form 4 - 2021gangstar sippas100% (1)

- Strategies Affecting Stock MarketDocument9 pagesStrategies Affecting Stock MarketAditya Kanchan BarasPas encore d'évaluation

- ACCT233 Tutorial 5 QuestionsDocument3 pagesACCT233 Tutorial 5 QuestionsDominic RobinsonPas encore d'évaluation

- Inflation AccountingDocument2 pagesInflation AccountingmehulPas encore d'évaluation

- Ias 40 QuestionsDocument6 pagesIas 40 QuestionsFrank AlexanderPas encore d'évaluation

- 2022 Financial StatementsDocument19 pages2022 Financial StatementsThe King's UniversityPas encore d'évaluation

- Audit SM CH 4 2022Document13 pagesAudit SM CH 4 2022andzie09876Pas encore d'évaluation

- MBA Corporate Finance Online Exam 05122020 025210pmDocument3 pagesMBA Corporate Finance Online Exam 05122020 025210pmminza siddiquiPas encore d'évaluation

- Definition of Accounting and FinanceDocument9 pagesDefinition of Accounting and FinanceSantos Lucas VintePas encore d'évaluation

- Accounting Formulas 1 PDFDocument5 pagesAccounting Formulas 1 PDFmianmobeenaslam80% (5)

- Chapter 3 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document24 pagesChapter 3 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarPas encore d'évaluation

- Act Module4 Cashflow Fabm 2 5.Document11 pagesAct Module4 Cashflow Fabm 2 5.DOMDOM, NORIEL O.Pas encore d'évaluation

- Capital Structure and Leverage: Multiple Choice: ConceptualDocument56 pagesCapital Structure and Leverage: Multiple Choice: ConceptualEngr Fizza AkbarPas encore d'évaluation

- Barksdale's Brewery Company - A Commercial Lending Case: Patrick Terry Edward C. Lawrence BackgroundDocument25 pagesBarksdale's Brewery Company - A Commercial Lending Case: Patrick Terry Edward C. Lawrence BackgroundBSA 1-CChelsee Rosemae MoraldePas encore d'évaluation

- Davao - Eagle - Com JOSEPHDocument6 pagesDavao - Eagle - Com JOSEPHablay logenePas encore d'évaluation

- Cost Accounting Question BankDocument6 pagesCost Accounting Question BankAnkit Goswami100% (1)

- CA Final AFM Q MTP 2 May 2024 Castudynotes ComDocument10 pagesCA Final AFM Q MTP 2 May 2024 Castudynotes Compabitrarijal1227Pas encore d'évaluation

- CF2 - Chapter 1 Cost of Capital - SVDocument58 pagesCF2 - Chapter 1 Cost of Capital - SVleducPas encore d'évaluation

- East Coast Yachts KeyDocument8 pagesEast Coast Yachts Keyreddevil911100% (1)

- Volume2 gv2Document702 pagesVolume2 gv2WikusPas encore d'évaluation

- Barth, M.E., Landsman, W.R. & Wahlen, J.M. (1995). Fair value accounting: Effects on banks’ earnings volatility, regulatory capital and value of contractual cash flows. Journal of Banking and Finance, 19, 577-605.Document29 pagesBarth, M.E., Landsman, W.R. & Wahlen, J.M. (1995). Fair value accounting: Effects on banks’ earnings volatility, regulatory capital and value of contractual cash flows. Journal of Banking and Finance, 19, 577-605.Marchelyn PongsapanPas encore d'évaluation

- Bracey Company Manufactures and Sells One ProductDocument2 pagesBracey Company Manufactures and Sells One ProductKailash KumarPas encore d'évaluation

- Cash Flow Part 2 To 7 Term 2 Sunil PandaDocument35 pagesCash Flow Part 2 To 7 Term 2 Sunil PandaAnupama SinghPas encore d'évaluation

- CFAB Accounting Chap02 Accounting EquationDocument38 pagesCFAB Accounting Chap02 Accounting EquationHoa NguyễnPas encore d'évaluation

- F1 CIMA Workbook Q PDFDocument169 pagesF1 CIMA Workbook Q PDFKhadija Rampurawala100% (1)

- A Comparison of IFRS, US GAAP and Belgian GAAPDocument100 pagesA Comparison of IFRS, US GAAP and Belgian GAAPVoicu Dragomir67% (3)

- Data Ratio-Analysis Group3Document13 pagesData Ratio-Analysis Group3Phúc Lê HoàngPas encore d'évaluation