Vous aimerez peut-être aussi

- Islamic Finance and Banking SystemDocument9 pagesIslamic Finance and Banking SystemSuhail RajputPas encore d'évaluation

- Islamic Banking OverviewDocument21 pagesIslamic Banking OverviewmudasirPas encore d'évaluation

- CandyDocument3 pagesCandyMuhammad Khuram ShahzadPas encore d'évaluation

- Islamic Banking AssignmentDocument3 pagesIslamic Banking AssignmentNadia BaigPas encore d'évaluation

- Chapter OneDocument8 pagesChapter OneZainab IbrahimPas encore d'évaluation

- PrinciplesDocument2 pagesPrinciplesIrshadUl HaqPas encore d'évaluation

- Islamic Finance IntroductionDocument5 pagesIslamic Finance Introductioneshaal naseemPas encore d'évaluation

- Chap 10Document2 pagesChap 10MuhammadWaseemPas encore d'évaluation

- Basics of Islamic BankingDocument6 pagesBasics of Islamic BankingMnk BhkPas encore d'évaluation

- Islamic Banking: A Brief Summary of The IndustryDocument6 pagesIslamic Banking: A Brief Summary of The IndustryAbimbola Adewale MonsurPas encore d'évaluation

- Salient Features of Islamic BankingDocument2 pagesSalient Features of Islamic BankingNoor Hafizah0% (2)

- Islamic Banking: Assigned By: Kundan Kumar 2K19/BBA/86 Assigned To: Ma'Am Paras ChannarDocument5 pagesIslamic Banking: Assigned By: Kundan Kumar 2K19/BBA/86 Assigned To: Ma'Am Paras ChannarKundan kumarPas encore d'évaluation

- Islamic Banking Myths and FactsDocument12 pagesIslamic Banking Myths and Factsthexplorer008Pas encore d'évaluation

- Chapter 5 Interest Free BankingDocument30 pagesChapter 5 Interest Free BankingSyed Irfan Bin Inayat100% (1)

- Islamic Banking System - EditedDocument5 pagesIslamic Banking System - EditedLubaba RazaPas encore d'évaluation

- Another ApproachDocument13 pagesAnother ApproachShameem ChoudharyPas encore d'évaluation

- Project IBF Submitted To: DR. Sabeen Khurram KhanDocument7 pagesProject IBF Submitted To: DR. Sabeen Khurram KhanSheikh AbdullahPas encore d'évaluation

- Project Report Bank Islami CompletedDocument64 pagesProject Report Bank Islami Completedsameer ahmedPas encore d'évaluation

- Islamic BankingpdfDocument6 pagesIslamic BankingpdfMD. IBRAHIM KHOLILULLAHPas encore d'évaluation

- Assignment On Islamic BankingDocument8 pagesAssignment On Islamic BankingRimsha LatifPas encore d'évaluation

- Islamic Banking: By: Soukaina Ikbal & Chaimae BenyahyaDocument10 pagesIslamic Banking: By: Soukaina Ikbal & Chaimae BenyahyaKenza HazzazPas encore d'évaluation

- Question 2: Foreign Listing Affect Cost of Capital of Company. Banking Interest FreeDocument8 pagesQuestion 2: Foreign Listing Affect Cost of Capital of Company. Banking Interest FreeAhmed HadiPas encore d'évaluation

- Meezan BankDocument40 pagesMeezan BankShahid Abdul100% (1)

- Meezan Bank LTDDocument53 pagesMeezan Bank LTDim.abid1Pas encore d'évaluation

- Islamic Bankin1Document16 pagesIslamic Bankin1Tariq BuzdarPas encore d'évaluation

- Banking On Sharia Principles: Islamic Banking and The Financial IndustryDocument3 pagesBanking On Sharia Principles: Islamic Banking and The Financial IndustryNaffay HussainPas encore d'évaluation

- Financial Contracts, Credit Risk and Performance of Islamic BankingDocument22 pagesFinancial Contracts, Credit Risk and Performance of Islamic BankingUmer KiyaniPas encore d'évaluation

- Meezan Bank Internship ReportDocument32 pagesMeezan Bank Internship ReportRanaAakashAhmadPas encore d'évaluation

- Islamic Banking And Finance for Beginners!D'EverandIslamic Banking And Finance for Beginners!Évaluation : 2 sur 5 étoiles2/5 (1)

- Assignment 1 Islamic Vs Conventional Banks Performance AnalysisDocument8 pagesAssignment 1 Islamic Vs Conventional Banks Performance AnalysisWali AfridiPas encore d'évaluation

- History of Islamic BankingDocument13 pagesHistory of Islamic Bankingkamran5264100% (3)

- Islamic Banking and Finance MBA (Finance) Abasyn University Peshawar. (Farman Qayyum)Document35 pagesIslamic Banking and Finance MBA (Finance) Abasyn University Peshawar. (Farman Qayyum)farman_qayyumPas encore d'évaluation

- Differences Between Islamic Bank and ConventionalDocument4 pagesDifferences Between Islamic Bank and ConventionalSanjida RintiPas encore d'évaluation

- Al BarskhaDocument86 pagesAl BarskhaMian MohsinPas encore d'évaluation

- My ReportDocument48 pagesMy ReportSaik Sadat Ibna IslamPas encore d'évaluation

- What Is The Difference Between Commercial Banking & Islamic BankingDocument19 pagesWhat Is The Difference Between Commercial Banking & Islamic BankingEEC PakistanPas encore d'évaluation

- Differences Between Islamic Banks & ConventionalDocument3 pagesDifferences Between Islamic Banks & ConventionalBushra KhanPas encore d'évaluation

- Relevance of Islamic Banking.: Presented By:-Abhinav Singh Nadeem Haidar Mukesh PandeyDocument9 pagesRelevance of Islamic Banking.: Presented By:-Abhinav Singh Nadeem Haidar Mukesh PandeyAbhinav RanaPas encore d'évaluation

- Uts B.inggris - M. Khoiril Falahis Shufi - 2102016009-2Document2 pagesUts B.inggris - M. Khoiril Falahis Shufi - 2102016009-2Falahis ShufiPas encore d'évaluation

- Islamic BankingDocument25 pagesIslamic Bankingmojoo2003Pas encore d'évaluation

- Revised Chapter 4Document21 pagesRevised Chapter 4kellydaPas encore d'évaluation

- Deposit Mobilization TechniquesDocument8 pagesDeposit Mobilization TechniquesFahad Bhuiyan100% (1)

- Formate - IJHSS - Historical Background of Islamic Banking in NigeriaDocument8 pagesFormate - IJHSS - Historical Background of Islamic Banking in Nigeriaiaset123Pas encore d'évaluation

- Islamic Banking Versus Commercial Banking:: Prospects & OpportunitiesDocument37 pagesIslamic Banking Versus Commercial Banking:: Prospects & OpportunitiesHanis HazwaniPas encore d'évaluation

- Classical Islamic BankingDocument75 pagesClassical Islamic BankingNida_Basheer_206Pas encore d'évaluation

- Comparison of Islamic and Conventional Banking System PresentationDocument18 pagesComparison of Islamic and Conventional Banking System PresentationZohaib AhmedPas encore d'évaluation

- What Is Islamic Banking: PrinciplesDocument7 pagesWhat Is Islamic Banking: PrinciplesMurad EltaherPas encore d'évaluation

- Special Topics in Banking & Finance CH 8Document15 pagesSpecial Topics in Banking & Finance CH 8karim kobeissiPas encore d'évaluation

- In The Name of Allah, Who Is The Most Beneficent and Most MercifulDocument10 pagesIn The Name of Allah, Who Is The Most Beneficent and Most MercifulMuhammad Rohail AkhtarPas encore d'évaluation

- Modes of Banking in PakistanDocument12 pagesModes of Banking in Pakistansara24391Pas encore d'évaluation

- Problems and Prospects of Islamic BankingDocument4 pagesProblems and Prospects of Islamic BankingKhamini Kathirvelu PillaiPas encore d'évaluation

- 098 - Essay Bhs - Inggris - Ahmad Mughni Al MubarokDocument5 pages098 - Essay Bhs - Inggris - Ahmad Mughni Al MubarokAhmad Mughni Al MubarokPas encore d'évaluation

- Assignment On of Islamic BankingDocument14 pagesAssignment On of Islamic BankingSanjani80% (5)

- Diferenciation Between The Islamic and Conventional BankDocument26 pagesDiferenciation Between The Islamic and Conventional BankyosifatPas encore d'évaluation

- Islamic BankingDocument3 pagesIslamic BankingmuneebalamPas encore d'évaluation

- What Is Islamic BankingDocument5 pagesWhat Is Islamic BankingMarium MughalPas encore d'évaluation

- A Comparison Between Reporting of Conventional Leasing and Islamic LeasingDocument23 pagesA Comparison Between Reporting of Conventional Leasing and Islamic LeasingNosh HashmiPas encore d'évaluation

- Islamic BankingDocument6 pagesIslamic BankingTanvir SazzadPas encore d'évaluation

- Takaful and Islamic Cooperative Finance for Beginners!D'EverandTakaful and Islamic Cooperative Finance for Beginners!Pas encore d'évaluation

- Cee Guide To LNGDocument2 pagesCee Guide To LNGNatalia Magaia CambaPas encore d'évaluation

- Derivatives (Fin402) : Assignment: EssayDocument5 pagesDerivatives (Fin402) : Assignment: EssayNga Thị NguyễnPas encore d'évaluation

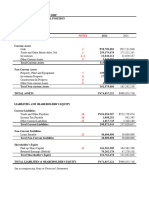

- Raymond Presentation FinalDocument23 pagesRaymond Presentation FinalAbizer KachwalaPas encore d'évaluation

- Lesson Six Homework-2Document3 pagesLesson Six Homework-2LiamPas encore d'évaluation

- 2005 Nicolet National Bank Annual ReportDocument16 pages2005 Nicolet National Bank Annual ReportNicolet BankPas encore d'évaluation

- Tarea 4 - Riesgo y Rendimiento Parte 1Document30 pagesTarea 4 - Riesgo y Rendimiento Parte 1Edgard Alberto Cuellar IriartePas encore d'évaluation

- Trans Canada Gold Corp. Signs Letter of Intent To Acquire The Gold Crow District Scale Gold and Magmatic Copper-Nickel-Cobalt ProjectDocument5 pagesTrans Canada Gold Corp. Signs Letter of Intent To Acquire The Gold Crow District Scale Gold and Magmatic Copper-Nickel-Cobalt ProjectTrans Canada Gold Corp. (TSX-V: TTG)Pas encore d'évaluation

- Competitive Mold MakerDocument6 pagesCompetitive Mold MakerMrLanternPas encore d'évaluation

- IFIC Bank Internship ReportDocument136 pagesIFIC Bank Internship ReportApplePas encore d'évaluation

- Bottled Water Strategy in UKDocument19 pagesBottled Water Strategy in UKshibin21Pas encore d'évaluation

- Case Study - : The Chubb CorporationDocument6 pagesCase Study - : The Chubb Corporationtiko bakashviliPas encore d'évaluation

- Samuelson, Economics, 17 Ed.: by RetnoDocument18 pagesSamuelson, Economics, 17 Ed.: by RetnoWilda Rahayu HamzahPas encore d'évaluation

- SyaratDocument9 pagesSyaratWan RidhwanPas encore d'évaluation

- The Brand Equity Approach To Marketing of Malaysian Palm ProductDocument138 pagesThe Brand Equity Approach To Marketing of Malaysian Palm ProductEndi SingarimbunPas encore d'évaluation

- Sea Rule 15c3 1 InterpretationsDocument236 pagesSea Rule 15c3 1 Interpretationsdestinylam123Pas encore d'évaluation

- Financial Ratio Analysis IDocument12 pagesFinancial Ratio Analysis IManvi Jain0% (1)

- Hitachi CaseDocument15 pagesHitachi CaseManish Goyal0% (1)

- Supply Chain Design and Analysis: Models and MethodsDocument22 pagesSupply Chain Design and Analysis: Models and MethodssankofakanianPas encore d'évaluation

- FIMA 30013 FS Analysis Premium FSDocument4 pagesFIMA 30013 FS Analysis Premium FSdcdeguzman.pup.pulilanPas encore d'évaluation

- Hour 2: Chris PuplavaDocument64 pagesHour 2: Chris PuplavaFinancial Sense100% (1)

- ClassIXEco. TBQ & Assign. (Ch-2) SolDocument11 pagesClassIXEco. TBQ & Assign. (Ch-2) SolSujitnkbpsPas encore d'évaluation

- Project ON Life Insurance Corporati ONDocument34 pagesProject ON Life Insurance Corporati ONVirendra JhaPas encore d'évaluation

- PWC Life Insurance Is Bought & Not SoldDocument30 pagesPWC Life Insurance Is Bought & Not Soldcybil36Pas encore d'évaluation

- Business Case For MDMDocument18 pagesBusiness Case For MDMvinay10356Pas encore d'évaluation

- Palmer v. Commissioner, 302 U.S. 63 (1937)Document7 pagesPalmer v. Commissioner, 302 U.S. 63 (1937)Scribd Government DocsPas encore d'évaluation

- Shg-Self Help GroupDocument56 pagesShg-Self Help Groupkaivalya chaaitanya ugale100% (2)

- Definitive Shopper Marketing GuideDocument91 pagesDefinitive Shopper Marketing GuideDemand Metric100% (2)

- Maruti Suzuki India Balance Sheet, Maruti Suzuki India Financial Statement & AccountsDocument3 pagesMaruti Suzuki India Balance Sheet, Maruti Suzuki India Financial Statement & Accountsankur51Pas encore d'évaluation

- 01 - Forex-Question BankDocument52 pages01 - Forex-Question BankSs DonthiPas encore d'évaluation

- ICT Sector Strategy and Investment Plan (2015 - 2020)Document83 pagesICT Sector Strategy and Investment Plan (2015 - 2020)Sulekha Bhattacherjee100% (2)