Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- A Plan Which Takes Care of Your Health As Well As Protects It Against Unforeseen EmergenciesDocument1 pageA Plan Which Takes Care of Your Health As Well As Protects It Against Unforeseen EmergenciesRKPas encore d'évaluation

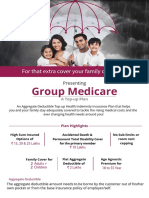

- Axis GroupMedicare E-Brochure (Top-Up)Document4 pagesAxis GroupMedicare E-Brochure (Top-Up)RKPas encore d'évaluation

- Health Pro Infinity BrochureDocument5 pagesHealth Pro Infinity BrochureRK0% (1)

- ETB Super Top Up GMC Mailer - Customer FacingDocument2 pagesETB Super Top Up GMC Mailer - Customer FacingRKPas encore d'évaluation

- LIM Interface SAPDocument2 pagesLIM Interface SAPRKPas encore d'évaluation

- PriingDocument2 pagesPriingRKPas encore d'évaluation

- HanuchankraDocument6 pagesHanuchankraRKPas encore d'évaluation

- Sri Venkateswara Swamy Vari Pooja Vidhanamu PDFDocument52 pagesSri Venkateswara Swamy Vari Pooja Vidhanamu PDFRKPas encore d'évaluation

- LIC Integrity PactDocument2 pagesLIC Integrity PactRKPas encore d'évaluation

- List of ExcludedDocument4 pagesList of ExcludedRKPas encore d'évaluation

- MC37-Display Rough-Cut Planning ProfileSOPDocument5 pagesMC37-Display Rough-Cut Planning ProfileSOPRKPas encore d'évaluation

- Sopflexible PlanningDocument23 pagesSopflexible PlanningAnonymous ODE4fS93Pas encore d'évaluation

- PriingDocument2 pagesPriingRKPas encore d'évaluation

- SOP&Flexible Planning ConfigDocument89 pagesSOP&Flexible Planning ConfigasifmubbuPas encore d'évaluation

- MC35-Create Rough-Cut Planning ProfileSOPDocument10 pagesMC35-Create Rough-Cut Planning ProfileSOPRKPas encore d'évaluation

- Premium Rates For Motor Third Party Liability 2018 19 PDFDocument5 pagesPremium Rates For Motor Third Party Liability 2018 19 PDFRKPas encore d'évaluation

- Sri Venkateswara Swamy Vari Pooja Vidhanamu PDFDocument52 pagesSri Venkateswara Swamy Vari Pooja Vidhanamu PDFRKPas encore d'évaluation

- IRDA Brochure PDFDocument24 pagesIRDA Brochure PDFRKPas encore d'évaluation

- Main PDF - IrdaDocument15 pagesMain PDF - IrdavinayakPas encore d'évaluation

- Physiomodalities Catlog NewDocument2 pagesPhysiomodalities Catlog NewRKPas encore d'évaluation

- Two Cover Bid SubmissionDocument40 pagesTwo Cover Bid SubmissionRKPas encore d'évaluation

- Insurance Regulatory & Development Authority Act: Module - 5Document12 pagesInsurance Regulatory & Development Authority Act: Module - 5RKPas encore d'évaluation

- Todays HoneywellDocument26 pagesTodays HoneywellIgor Ribeiro de SouzaPas encore d'évaluation

- Top Up Re-Application and Transfer of Amount FormDocument2 pagesTop Up Re-Application and Transfer of Amount FormRKPas encore d'évaluation

- Max Life Online Savings Plan Policy ProspectusDocument24 pagesMax Life Online Savings Plan Policy Prospectusvikas327Pas encore d'évaluation

- Sri Venkateswara Swamy Vari Pooja Vidhanamu PDFDocument52 pagesSri Venkateswara Swamy Vari Pooja Vidhanamu PDFRKPas encore d'évaluation

- Common Claim Form For - TN Flood 2015Document1 pageCommon Claim Form For - TN Flood 2015RKPas encore d'évaluation

- Jewellers Block Claim FormDocument3 pagesJewellers Block Claim FormRKPas encore d'évaluation

- Bankers Indemnity Claim FormDocument3 pagesBankers Indemnity Claim FormRKPas encore d'évaluation

- Zoning Regulations RMP2015Document69 pagesZoning Regulations RMP2015vivek7911Pas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Toll BridgesDocument9 pagesToll Bridgesapi-255693024Pas encore d'évaluation

- Code of EthicsDocument13 pagesCode of EthicsnelzerPas encore d'évaluation

- Skate Helena 02-06.01.2024Document1 pageSkate Helena 02-06.01.2024erkinongulPas encore d'évaluation

- Freemason's MonitorDocument143 pagesFreemason's Monitorpopecahbet100% (1)

- Drug Abuse and Addiction Effects On Human BodyDocument4 pagesDrug Abuse and Addiction Effects On Human BodyCriss Deea100% (1)

- Vayu Issue Vayu Issue III May Jun 2018Document116 pagesVayu Issue Vayu Issue III May Jun 2018vs_3457000Pas encore d'évaluation

- 1 Court Jurisdiction 1 Court JurisdictionDocument19 pages1 Court Jurisdiction 1 Court JurisdictionHermione Leong Yen KheePas encore d'évaluation

- Front Desk Staff-Giezel Bell Staff - Marc Client - Augustus Friend - AthenaDocument4 pagesFront Desk Staff-Giezel Bell Staff - Marc Client - Augustus Friend - Athenagener magbalitaPas encore d'évaluation

- Jayant CVDocument2 pagesJayant CVjayanttiwariPas encore d'évaluation

- PDHONLINE - Google SearchDocument2 pagesPDHONLINE - Google SearchThanga PandiPas encore d'évaluation

- Critical Analysis of The Concept of Plea Bargaining in IndiaDocument8 pagesCritical Analysis of The Concept of Plea Bargaining in IndiaSRUTHI KANNAN 2257024Pas encore d'évaluation

- English 6: Making A On An InformedDocument30 pagesEnglish 6: Making A On An InformedEDNALYN TANPas encore d'évaluation

- GEN ED Contemporary WorldDocument166 pagesGEN ED Contemporary WorldTom Fernando100% (1)

- Chernobyl Disaster: The Worst Man-Made Disaster in Human HistoryDocument13 pagesChernobyl Disaster: The Worst Man-Made Disaster in Human HistoryGowri ShankarPas encore d'évaluation

- Strategic Management CompleteDocument20 pagesStrategic Management Completeأبو ليلىPas encore d'évaluation

- Osayan - Argumentative Essay - PCDocument2 pagesOsayan - Argumentative Essay - PCMichaela OsayanPas encore d'évaluation

- 5.2.1 List of Placed Students VESIT NAAC TPCDocument154 pages5.2.1 List of Placed Students VESIT NAAC TPCRashmi RanjanPas encore d'évaluation

- Introduction To Marketing - KotlerDocument35 pagesIntroduction To Marketing - KotlerRajesh Patro0% (1)

- 7759 Cad-1Document2 pages7759 Cad-1Samir JainPas encore d'évaluation

- JustdiggitDocument21 pagesJustdiggityecith sanguinoPas encore d'évaluation

- TKAM ch1-5 Discussion QuestionsDocument14 pagesTKAM ch1-5 Discussion QuestionsJacqueline KennedyPas encore d'évaluation

- RHP Final Reviewer Galing Sa PDF Ni SirDocument37 pagesRHP Final Reviewer Galing Sa PDF Ni SirAilene PerezPas encore d'évaluation

- Present SimpleDocument5 pagesPresent SimpleNghi PhuongPas encore d'évaluation

- 07 DecisionTreeTasksWeek8Document5 pages07 DecisionTreeTasksWeek8Nebojša ĐukićPas encore d'évaluation

- Certificate of Transfer of ChargeDocument1 pageCertificate of Transfer of Chargemanirocgaming5Pas encore d'évaluation

- Invoice 141Document1 pageInvoice 141United KingdomPas encore d'évaluation

- Open Book Contract Management GuidanceDocument56 pagesOpen Book Contract Management GuidanceRoberto AlvarezPas encore d'évaluation

- 131RGApplication PDFDocument2 pages131RGApplication PDFMuhammad FarhanPas encore d'évaluation

- Sudan WikipediaDocument33 pagesSudan WikipediaUroš KrčadinacPas encore d'évaluation

- 2.-A-Journal & Ledger - QuestionsDocument3 pages2.-A-Journal & Ledger - QuestionsLibrarian 19750% (1)