Vous aimerez peut-être aussi

- Multifamily EbookDocument15 pagesMultifamily EbookLloydMandrellPas encore d'évaluation

- WHAT IS A BIRTH CERTIFICATE-Estate Equitable Title Receipt PDFDocument8 pagesWHAT IS A BIRTH CERTIFICATE-Estate Equitable Title Receipt PDFApril Clay75% (4)

- Ias 1 - IcanDocument51 pagesIas 1 - IcanLegogie Moses AnoghenaPas encore d'évaluation

- Practice HSC Papers General 2Document47 pagesPractice HSC Papers General 2DarrenPurtillWrightPas encore d'évaluation

- Sri Varma CE ReportDocument3 pagesSri Varma CE ReportRAJDECPas encore d'évaluation

- Toyota Astra Motor PaperDocument52 pagesToyota Astra Motor PaperFariz Alfan Azizi PermadiPas encore d'évaluation

- Basic Bookkeeping For EntrepreneursDocument36 pagesBasic Bookkeeping For EntrepreneursDanney EkaPas encore d'évaluation

- IAS Plus IAS 1, Presentati..Document10 pagesIAS Plus IAS 1, Presentati..Buddha BlessedPas encore d'évaluation

- PAS 1 With Notes - Pres of FS PDFDocument75 pagesPAS 1 With Notes - Pres of FS PDFFatima Ann GuevarraPas encore d'évaluation

- Ias 1 Presentation of Financial StatementsDocument42 pagesIas 1 Presentation of Financial StatementsEjaj-Ur-RahamanPas encore d'évaluation

- Wiley IFRS: Practical Implementation Guide and WorkbookD'EverandWiley IFRS: Practical Implementation Guide and WorkbookPas encore d'évaluation

- THESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementDocument46 pagesTHESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementVon Ianelle AguilaPas encore d'évaluation

- Summary of Ias 1Document8 pagesSummary of Ias 1g0025Pas encore d'évaluation

- Philippine Accounting Standards 1: PAS 1Document11 pagesPhilippine Accounting Standards 1: PAS 1yvetooot50% (4)

- Summary of IAS 1Document8 pagesSummary of IAS 1Vikash Hurrydoss100% (1)

- Ias 1 Presentation of Financial StatementsDocument6 pagesIas 1 Presentation of Financial Statementsa_michalczyk800% (2)

- P4-1: Consolidated Financials for Pea Corp and Subsidiary Sen CorpDocument21 pagesP4-1: Consolidated Financials for Pea Corp and Subsidiary Sen Corpnancy tomanda100% (1)

- Ias 1Document15 pagesIas 1ansaar9967% (3)

- Tugas Komputer AkuntansiDocument4 pagesTugas Komputer AkuntansiDwi RanggaPas encore d'évaluation

- Presentation of FSDocument2 pagesPresentation of FSTimmy KellyPas encore d'évaluation

- IAS 1 Preparation of FS PDFDocument12 pagesIAS 1 Preparation of FS PDFJohn Carlo SantianoPas encore d'évaluation

- Ias 1 7 8 10 ReviewerDocument13 pagesIas 1 7 8 10 ReviewerHazel Andrea Garduque LopezPas encore d'évaluation

- IAS 1 - Presentation of Financial StatementsDocument8 pagesIAS 1 - Presentation of Financial StatementsCaia VelazquezPas encore d'évaluation

- Objective of IAS 1: FrameworkDocument4 pagesObjective of IAS 1: FrameworkPatricia San PabloPas encore d'évaluation

- Pas 1,2,16Document17 pagesPas 1,2,16Cristopherson PerezPas encore d'évaluation

- Objective of IAS 1Document13 pagesObjective of IAS 1Katrina Faith Salonga BeoPas encore d'évaluation

- IAS 1 - Presentation of Financial StatementsDocument8 pagesIAS 1 - Presentation of Financial StatementsMarc Eric RedondoPas encore d'évaluation

- Objective of IAS 1Document4 pagesObjective of IAS 1Tin BatacPas encore d'évaluation

- Overview IASDocument12 pagesOverview IASButt ArhamPas encore d'évaluation

- Pas 1 Presentation of Financial StatementsDocument8 pagesPas 1 Presentation of Financial StatementsDivine Grace BravoPas encore d'évaluation

- Objective of IAS 1Document12 pagesObjective of IAS 1Emman P. ArimbuyutanPas encore d'évaluation

- Chapter 03 PAS 1 Presentation of Financial StatementsDocument12 pagesChapter 03 PAS 1 Presentation of Financial StatementsJoelyn Grace MontajesPas encore d'évaluation

- IAS DEtailsDocument101 pagesIAS DEtailsMorshedul AlamPas encore d'évaluation

- IAS 1 Objectives and RequirementsDocument62 pagesIAS 1 Objectives and RequirementsHAKUNA MATATAPas encore d'évaluation

- Ias 1Document10 pagesIas 1Pangem100% (1)

- Auditing PASDocument59 pagesAuditing PASjulie anne mae mendozaPas encore d'évaluation

- Philippine Accounting Standards 1 Presentation of Financial StatementsDocument10 pagesPhilippine Accounting Standards 1 Presentation of Financial StatementsJBPas encore d'évaluation

- Objective of PAS 1Document8 pagesObjective of PAS 1ROB101512Pas encore d'évaluation

- IAS 1 SummaryDocument17 pagesIAS 1 SummaryperuparambilPas encore d'évaluation

- IAS 1 Objective and RequirementsDocument7 pagesIAS 1 Objective and Requirementskristelle0marissePas encore d'évaluation

- Summary of Key IAS 1 Requirements (39Document18 pagesSummary of Key IAS 1 Requirements (39Mae Gamit LaglivaPas encore d'évaluation

- IAS 1 Financial Statement RequirementsDocument21 pagesIAS 1 Financial Statement RequirementsDEVINA GURRIAHPas encore d'évaluation

- PAS 1 Financial Statements OverviewDocument4 pagesPAS 1 Financial Statements OverviewPrincess ViePas encore d'évaluation

- Ias 1Document6 pagesIas 1Ruth Job L. SalamancaPas encore d'évaluation

- Explained: Based On Standards and Various Authors: Intermediate Accounting IIIDocument49 pagesExplained: Based On Standards and Various Authors: Intermediate Accounting IIIElijah Eartheah BanesPas encore d'évaluation

- Ias 1Document16 pagesIas 1ImrahPas encore d'évaluation

- IAS 1 - Presentation of Financial StatementsDocument12 pagesIAS 1 - Presentation of Financial StatementsnadeemPas encore d'évaluation

- Summary of Ias 1Document10 pagesSummary of Ias 1eloi94Pas encore d'évaluation

- Explanation Financial StatementsDocument3 pagesExplanation Financial StatementsitsmekuskusumaPas encore d'évaluation

- Ias 1Document3 pagesIas 1ash_muhammedPas encore d'évaluation

- Objective of IAS 1Document10 pagesObjective of IAS 1April IsidroPas encore d'évaluation

- Objective of IAS 1Document8 pagesObjective of IAS 1mahekshahPas encore d'évaluation

- 02 - IAS 1 Presentation of Financial Statements PDFDocument31 pages02 - IAS 1 Presentation of Financial Statements PDFmiaPas encore d'évaluation

- Ias 1 Presentation of Financial StatementsDocument9 pagesIas 1 Presentation of Financial StatementsmelissayplPas encore d'évaluation

- Unit3 CFAS PDFDocument12 pagesUnit3 CFAS PDFhellokittysaranghaePas encore d'évaluation

- IFRS 1 Presentation of Financial StatementsDocument14 pagesIFRS 1 Presentation of Financial StatementsCatherine RiveraPas encore d'évaluation

- Presentation of Financial StatementsDocument17 pagesPresentation of Financial StatementsFRANCIS IAN ALBARACIN IIPas encore d'évaluation

- Ias 1 Presentation of Financial Statements - A Closer Look: Munich Personal Repec ArchiveDocument15 pagesIas 1 Presentation of Financial Statements - A Closer Look: Munich Personal Repec Archiveaditya pandianPas encore d'évaluation

- Ifa TheoryDocument1 pageIfa TheoryShekh FaridPas encore d'évaluation

- IAS1:Presentation of Financial StatementsDocument2 pagesIAS1:Presentation of Financial StatementsSabrina LeePas encore d'évaluation

- Pas 1 Presentation of Financial Statements CfasDocument27 pagesPas 1 Presentation of Financial Statements CfasAMIEL TACULAOPas encore d'évaluation

- Notes To The Financial StatementsDocument4 pagesNotes To The Financial StatementsROB101512Pas encore d'évaluation

- Ias34 en PDFDocument9 pagesIas34 en PDFAgnieszka KsnPas encore d'évaluation

- Ias 1 Presentation of Financial StatementsDocument13 pagesIas 1 Presentation of Financial StatementsShahbaz MalikPas encore d'évaluation

- 84569159064Document3 pages84569159064fatimasani290Pas encore d'évaluation

- Overview of IAS 1Document15 pagesOverview of IAS 1Fazil DipuPas encore d'évaluation

- Wiley GAAP for Governments 2017: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsD'EverandWiley GAAP for Governments 2017: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsPas encore d'évaluation

- Wiley GAAP for Governments 2016: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsD'EverandWiley GAAP for Governments 2016: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsPas encore d'évaluation

- Codification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23D'EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23Pas encore d'évaluation

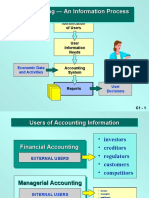

- Accounting - An Information Process Accounting - An Information ProcessDocument58 pagesAccounting - An Information Process Accounting - An Information ProcessBernadette Cunanan RamosPas encore d'évaluation

- (Amendments To IAS 16 and IAS 41), Which Applies To: Summary of IAS 41 ObjectiveDocument2 pages(Amendments To IAS 16 and IAS 41), Which Applies To: Summary of IAS 41 ObjectiveBernadette Cunanan RamosPas encore d'évaluation

- Cash Flow Statement TemplateDocument5 pagesCash Flow Statement Templatewaqas001Pas encore d'évaluation

- FrameworkDocument5 pagesFrameworkBernadette Cunanan Ramos0% (1)

- IFRS 9 RECOGNITION AND MEASUREMENT OF FINANCIAL INSTRUMENTSDocument12 pagesIFRS 9 RECOGNITION AND MEASUREMENT OF FINANCIAL INSTRUMENTSBernadette Cunanan RamosPas encore d'évaluation

- Performance Measurement in Decentralized Organizations: April 22, 2013Document53 pagesPerformance Measurement in Decentralized Organizations: April 22, 2013Mo KolapoPas encore d'évaluation

- IV Sem MBA - TM - Strategic Management Model Paper 2013Document2 pagesIV Sem MBA - TM - Strategic Management Model Paper 2013vikramvsuPas encore d'évaluation

- 2019briefer On KAPA As of 06102019Document16 pages2019briefer On KAPA As of 06102019JFAPas encore d'évaluation

- Soal Jawaban AKL CHP 1Document5 pagesSoal Jawaban AKL CHP 1Allpacino DesellaPas encore d'évaluation

- Accounting For Partnership - UnaDocument13 pagesAccounting For Partnership - UnaJastine Beltran - PerezPas encore d'évaluation

- Acciona Spain Investors DayDocument25 pagesAcciona Spain Investors DayVasiliy BogdanovPas encore d'évaluation

- Bank of America's Response To Cuomo's Fraud ChargesDocument61 pagesBank of America's Response To Cuomo's Fraud ChargesDealBookPas encore d'évaluation

- AUC Mining - Exploration & Mining Potential in Kamalenge, UgandaDocument21 pagesAUC Mining - Exploration & Mining Potential in Kamalenge, UgandaAfrican Centre for Media Excellence100% (3)

- Garcia Vs Boi GR No. 92024Document2 pagesGarcia Vs Boi GR No. 92024JayMichaelAquinoMarquezPas encore d'évaluation

- BASIX Relationship Management SheetDocument22 pagesBASIX Relationship Management SheetAnantha LakshmiPas encore d'évaluation

- Aircraft ValuationDocument4 pagesAircraft Valuationdjagger1Pas encore d'évaluation

- Rational or Irrational ManagersDocument5 pagesRational or Irrational ManagersIORDACHE GEORGEPas encore d'évaluation

- Principles of Risk Management and Insurance Chapter 1 Key ConceptsDocument11 pagesPrinciples of Risk Management and Insurance Chapter 1 Key ConceptsAhmed NaserPas encore d'évaluation

- Sapm Work NotesDocument138 pagesSapm Work NotesShaliniPas encore d'évaluation

- Quaid e Azam Solar ParkDocument8 pagesQuaid e Azam Solar ParkShahzad TabassumPas encore d'évaluation

- General Ledger and Reporting FinalDocument7 pagesGeneral Ledger and Reporting FinalJac KlynPas encore d'évaluation

- Fortress Investment Group 2008 Annual ReportDocument165 pagesFortress Investment Group 2008 Annual ReportAsiaBuyoutsPas encore d'évaluation

- BOP Components and TransactionsDocument6 pagesBOP Components and TransactionsAnitha GirigoudruPas encore d'évaluation

- Risk Tolerance and Strategic Asset ManagementDocument26 pagesRisk Tolerance and Strategic Asset ManagementMaestroanon100% (1)

- Ukraine Makes One Step Down in World Competitiveness RankingDocument2 pagesUkraine Makes One Step Down in World Competitiveness RankingRibi Daño-LunaPas encore d'évaluation

- Lafarge AR 2017Document173 pagesLafarge AR 2017Junwen LeePas encore d'évaluation