Vous aimerez peut-être aussi

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Presentation For Viva: Miss. Akshata Anil MasurkarDocument64 pagesPresentation For Viva: Miss. Akshata Anil MasurkarAkshata MasurkarPas encore d'évaluation

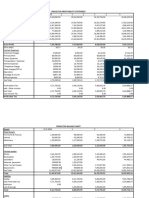

- (VIII) Chapter 3 (Financial Analysis and SWOT Analysis)Document14 pages(VIII) Chapter 3 (Financial Analysis and SWOT Analysis)Swami Yog BirendraPas encore d'évaluation

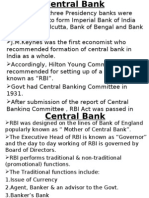

- Central BankDocument24 pagesCentral BankShailesh RathodPas encore d'évaluation

- How Data Analytics Is Transforming The Finance IndustryDocument17 pagesHow Data Analytics Is Transforming The Finance IndustrySandaPas encore d'évaluation

- Share NumerologyDocument24 pagesShare NumerologyDeepak SolankiPas encore d'évaluation

- Alagappa University, Karaikudi SYLLABUS UNDER CBCS PATTERN (W.e.f. 2011-12)Document26 pagesAlagappa University, Karaikudi SYLLABUS UNDER CBCS PATTERN (W.e.f. 2011-12)Mathan NaganPas encore d'évaluation

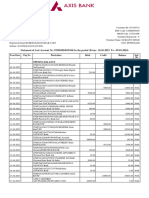

- Account STMT XX5184 09012024Document7 pagesAccount STMT XX5184 09012024Praveen SainiPas encore d'évaluation

- Amalsad CaseDocument16 pagesAmalsad CaseShobhan MeherPas encore d'évaluation

- IMPS Process FlowDocument12 pagesIMPS Process FlowThamil Inian100% (1)

- RA 10606-PhilHealth LawDocument10 pagesRA 10606-PhilHealth Lawleeashlee0% (1)

- The Philippine Financial System An OverviewDocument5 pagesThe Philippine Financial System An OverviewMark Francis Ng67% (3)

- The Next 20 Billion Digital MarketDocument4 pagesThe Next 20 Billion Digital MarketakuabataPas encore d'évaluation

- Group 2 Problem Set 1Document11 pagesGroup 2 Problem Set 1Nguyễn Thị Minh NgọcPas encore d'évaluation

- Know About Swiss Bank AccountDocument3 pagesKnow About Swiss Bank AccountJain DanendraPas encore d'évaluation

- SBCL To LeaseDocument27 pagesSBCL To LeaseGanesh100% (2)

- PM Lecture 7Document12 pagesPM Lecture 7Atharva BanarsePas encore d'évaluation

- Money, Banking and Finance Learning OutcomesDocument3 pagesMoney, Banking and Finance Learning OutcomesMuhammad ShahzadPas encore d'évaluation

- Standard Charter-Ad PlanDocument25 pagesStandard Charter-Ad Plansyed usman wazirPas encore d'évaluation

- 18 AppendixDocument9 pages18 Appendixsonia khuranaPas encore d'évaluation

- Capital FormationDocument76 pagesCapital FormationAnonymous 45z6m4eE7pPas encore d'évaluation

- The Electronic Clearing Service in IndiaDocument3 pagesThe Electronic Clearing Service in Indiamax_dcostaPas encore d'évaluation

- Bank Alfalah Case Study Presentation by Ali Raza Mi11MBA025Document35 pagesBank Alfalah Case Study Presentation by Ali Raza Mi11MBA025Ali RazaPas encore d'évaluation

- E7 - TreasuryRCM TemplateDocument30 pagesE7 - TreasuryRCM Templatenazriya nasarPas encore d'évaluation

- Sathyabama University Faculty of Business AdministrationDocument16 pagesSathyabama University Faculty of Business AdministrationGracyPas encore d'évaluation

- RBI NOTIFICATION ON TRA ACCOUNT IECD - No.16 - 08.12.01 - 2001-02 PDFDocument9 pagesRBI NOTIFICATION ON TRA ACCOUNT IECD - No.16 - 08.12.01 - 2001-02 PDFMayank ParekhPas encore d'évaluation

- Sachin DaneshwariDocument2 pagesSachin DaneshwariADARSH PATTARPas encore d'évaluation

- Aci Limited q1 Fs - 2022 23 - 13 11 2022Document20 pagesAci Limited q1 Fs - 2022 23 - 13 11 2022israt.reefaPas encore d'évaluation

- Fee Information Document: Service Fee General Account ServicesDocument8 pagesFee Information Document: Service Fee General Account ServicesAndreea SaftaPas encore d'évaluation

- Semantic DraftDocument409 pagesSemantic DraftGaneshPas encore d'évaluation

- AFM NotesDocument55 pagesAFM NotesrenesanitaPas encore d'évaluation