Vous aimerez peut-être aussi

- Jose Mexican RestaurantDocument4 pagesJose Mexican RestaurantYanyan RivalPas encore d'évaluation

- WP Business Analytics in BankingDocument8 pagesWP Business Analytics in BankingYanyan RivalPas encore d'évaluation

- IJHTAsixsigmaarticle - PDF Starwood HotelsDocument21 pagesIJHTAsixsigmaarticle - PDF Starwood HotelsYanyan RivalPas encore d'évaluation

- FI - UITF - BPI Money Market Fund - May 2017Document3 pagesFI - UITF - BPI Money Market Fund - May 2017Yanyan RivalPas encore d'évaluation

- Introduction To Management Syllabus 2nd Semester 2010-11-21phynoDocument3 pagesIntroduction To Management Syllabus 2nd Semester 2010-11-21phynoYanyan RivalPas encore d'évaluation

- Minutes of Meeting PICPA 12.20.2018 1Document2 pagesMinutes of Meeting PICPA 12.20.2018 1Yanyan RivalPas encore d'évaluation

- SampleDocument11 pagesSampleYanyan RivalPas encore d'évaluation

- Chapter 2 ReportDocument19 pagesChapter 2 ReportYanyan RivalPas encore d'évaluation

- ConsanguinityDocument1 pageConsanguinityYanyan RivalPas encore d'évaluation

- Edgar SIA Success StoryDocument5 pagesEdgar SIA Success StoryYanyan Rival100% (1)

- Chapter 4 - Pair ReportDocument2 pagesChapter 4 - Pair ReportYanyan RivalPas encore d'évaluation

- Consanguinity and Affinity Relationship ChartDocument1 pageConsanguinity and Affinity Relationship ChartYanyan RivalPas encore d'évaluation

- Pair Fieldwork Assignment No. 1Document5 pagesPair Fieldwork Assignment No. 1Yanyan RivalPas encore d'évaluation

- GateDocument1 pageGateYanyan RivalPas encore d'évaluation

- Math 1Document2 pagesMath 1Yanyan RivalPas encore d'évaluation

- Cre 1Document2 pagesCre 1Yanyan RivalPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Cape Communication Studies 2021Document10 pagesCape Communication Studies 2021raliegh100% (5)

- 1617 2ndS FX NBergoniaDocument11 pages1617 2ndS FX NBergoniaJames Louis BarcenasPas encore d'évaluation

- FC and CCDocument2 pagesFC and CCMIKHAEL MEDRANOPas encore d'évaluation

- Retirement Age To Be ExtendedDocument1 pageRetirement Age To Be ExtendedRh SamsserPas encore d'évaluation

- January 2018Document64 pagesJanuary 2018Eric SantiagoPas encore d'évaluation

- Dr.C.S.RANGARAJAN Vs UNIVERSITY OF MADRASDocument3 pagesDr.C.S.RANGARAJAN Vs UNIVERSITY OF MADRASCHETSUNPas encore d'évaluation

- Kiddie Tax 2021Document2 pagesKiddie Tax 2021Finn KevinPas encore d'évaluation

- Insurance Project Edited 1Document34 pagesInsurance Project Edited 1hareesh karrothuPas encore d'évaluation

- Performance Appraisal Letter FormatDocument8 pagesPerformance Appraisal Letter FormatHarry olardoPas encore d'évaluation

- UBS Global Wealth Report 2018 enDocument60 pagesUBS Global Wealth Report 2018 enDavid KwokPas encore d'évaluation

- Info LeafletasdasdasdasdDocument23 pagesInfo LeafletasdasdasdasdDon CryptoPas encore d'évaluation

- Employees Fps 1971Document22 pagesEmployees Fps 1971VasanthianbazhaganPas encore d'évaluation

- Dorice Urassa Research FinalDocument59 pagesDorice Urassa Research Finaljupiter stationeryPas encore d'évaluation

- 01 Time Value Questions 1-14Document2 pages01 Time Value Questions 1-14Amir GhasdiPas encore d'évaluation

- Instructions For Form 3520-A: Annual Information Return of Foreign Trust With A U.S. OwnerDocument4 pagesInstructions For Form 3520-A: Annual Information Return of Foreign Trust With A U.S. OwnerIRSPas encore d'évaluation

- Sure Start Maternity Grant: From The Social FundDocument11 pagesSure Start Maternity Grant: From The Social FundKenya GrigorePas encore d'évaluation

- Affidavit of UndertakingDocument1 pageAffidavit of UndertakingHaidisheena AllamaPas encore d'évaluation

- Acturarial Mathematics - BowersDocument780 pagesActurarial Mathematics - BowersEstefanía Luna Flores100% (1)

- Report FM FinalDocument31 pagesReport FM FinalSaif JillaniPas encore d'évaluation

- Erkurheleni Electricity TariffDocument280 pagesErkurheleni Electricity TariffclintlakeyPas encore d'évaluation

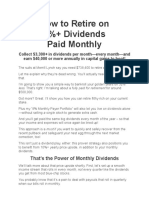

- Retire On Monthly DividendsDocument15 pagesRetire On Monthly DividendsDanaPas encore d'évaluation

- Oppenheimer CaseDocument3 pagesOppenheimer CaselxyxnxPas encore d'évaluation

- Sales Brochure - LIC S NGSCA - CleanDocument6 pagesSales Brochure - LIC S NGSCA - CleanPrakash kumarTripathiPas encore d'évaluation

- Global Benefits & Employment Guideline 2017 - SampleDocument73 pagesGlobal Benefits & Employment Guideline 2017 - Samplelixinyu liPas encore d'évaluation

- Isp 1300 PDFDocument8 pagesIsp 1300 PDFBintou DukureyPas encore d'évaluation

- Itr-1 Sahaj Individual Income Tax ReturnDocument5 pagesItr-1 Sahaj Individual Income Tax Returnchinna rajaPas encore d'évaluation

- Time Value of Money (Module 2)Document17 pagesTime Value of Money (Module 2)Yuvaraj RaoPas encore d'évaluation

- Departmental Test - November 2019 Session Paper Code-08Document16 pagesDepartmental Test - November 2019 Session Paper Code-08KESANAMPas encore d'évaluation

- Reply - EPFO Apex Court Contempt Petition - HPTDC Union PDFDocument22 pagesReply - EPFO Apex Court Contempt Petition - HPTDC Union PDFSudha100% (1)

- DLC PM 00433080000021462Document2 pagesDLC PM 00433080000021462Ranvir SinghPas encore d'évaluation