Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Answer Key Chapters 1 7Document40 pagesAnswer Key Chapters 1 7Sheila Mae Guerta Lacerona74% (38)

- Tax Banggawan2019 Ch.15-ADocument12 pagesTax Banggawan2019 Ch.15-ANoreen LeddaPas encore d'évaluation

- PDF To WordDocument5 pagesPDF To WordDharmesh DeshmukhPas encore d'évaluation

- ProjectDocument44 pagesProjectpawar182% (11)

- Income Tax SlabDocument26 pagesIncome Tax SlabDharmesh DeshmukhPas encore d'évaluation

- Part II Semester IIIDocument39 pagesPart II Semester IIIDharmesh DeshmukhPas encore d'évaluation

- Model Project 1Document67 pagesModel Project 1Dharmesh Deshmukh100% (1)

- Model Project 1Document71 pagesModel Project 1dineshshaPas encore d'évaluation

- Model Questionnaire 1Document12 pagesModel Questionnaire 1Dharmesh Deshmukh100% (1)

- Model Questionnaire 2Document13 pagesModel Questionnaire 2Dharmesh Deshmukh100% (1)

- Comparative Study of Private and Public Bank/icici& SbiDocument83 pagesComparative Study of Private and Public Bank/icici& SbiDharmesh Deshmukh80% (5)

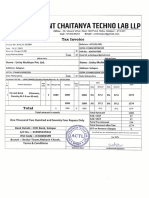

- Anant Chaitanya Techn0 Lab LLP: SalaltaDocument11 pagesAnant Chaitanya Techn0 Lab LLP: SalaltaGiridhari ChandrabansiPas encore d'évaluation

- Inv TG B1 92033426 101003789746 March 2023 PDFDocument4 pagesInv TG B1 92033426 101003789746 March 2023 PDFVara Prasad dasariPas encore d'évaluation

- TAX 06.2 - Fringe Benefit TaxDocument2 pagesTAX 06.2 - Fringe Benefit TaxMary Louise CamposanoPas encore d'évaluation

- Kalol Indian Farmers Fertiliser Co-Operative Limited Pay SlipDocument1 pageKalol Indian Farmers Fertiliser Co-Operative Limited Pay SlipSHAILESH PATELPas encore d'évaluation

- Chapter 3 PayrollDocument16 pagesChapter 3 PayrollAbdi Mucee TubePas encore d'évaluation

- Payslip 90002364 10 2020Document1 pagePayslip 90002364 10 2020souvik deyPas encore d'évaluation

- Public Finance Course Outline 2Document2 pagesPublic Finance Course Outline 2Wonde Biru0% (1)

- R12-Tables and ViewsDocument29 pagesR12-Tables and ViewsshikhaPas encore d'évaluation

- Medicard PH v. CirDocument2 pagesMedicard PH v. CirVon Lee De LunaPas encore d'évaluation

- IAS12 - Examples - SolutionDocument9 pagesIAS12 - Examples - SolutionTrần Nguyễn Tuệ MinhPas encore d'évaluation

- Week 8Document2 pagesWeek 8Nikunj D Patel100% (1)

- March 11 Pay Slip NewDocument2 pagesMarch 11 Pay Slip NewManish ShrivastavaPas encore d'évaluation

- Income TaxesDocument37 pagesIncome TaxesAngelaMariePeñarandaPas encore d'évaluation

- B91 Panchsheel Vihar, Behind Triveni Complex, Sheikh Sarai Phase I, New Delhi. 110017. India. Phone: +91.11.40511100 - WebsiteDocument1 pageB91 Panchsheel Vihar, Behind Triveni Complex, Sheikh Sarai Phase I, New Delhi. 110017. India. Phone: +91.11.40511100 - WebsiteRahul AryanPas encore d'évaluation

- April 2021 PAYSLIPDocument1 pageApril 2021 PAYSLIPPuja ParekhPas encore d'évaluation

- U.S. Individual Income Tax Return: Filing StatusDocument5 pagesU.S. Individual Income Tax Return: Filing Statuskristen kindlePas encore d'évaluation

- Tax 1 - Outline (Gross Income and Income Tax) Part1Document6 pagesTax 1 - Outline (Gross Income and Income Tax) Part1Katrina Marie OraldePas encore d'évaluation

- Taxation ProjectDocument12 pagesTaxation ProjectSagar DhanakPas encore d'évaluation

- S.No Amount /Fund/PTC/CRC/Conditional Grant Amount of Withholding Tax DeductedDocument5 pagesS.No Amount /Fund/PTC/CRC/Conditional Grant Amount of Withholding Tax Deductedtbtoxic6Pas encore d'évaluation

- Denis Martin Jacobo - RESEARCHDocument73 pagesDenis Martin Jacobo - RESEARCHjupiter stationeryPas encore d'évaluation

- Amara Raja Batteries LimitedDocument1 pageAmara Raja Batteries LimitedNani AnugaPas encore d'évaluation

- Supreme Assurance: Treasury Announces Clearance of VAT Refund BacklogDocument1 pageSupreme Assurance: Treasury Announces Clearance of VAT Refund BacklogJoseph OmwengaPas encore d'évaluation

- MUKANDDocument2 pagesMUKANDmakrand87Pas encore d'évaluation

- Chapter 14-Regular Income Taxation: IndividualsDocument28 pagesChapter 14-Regular Income Taxation: Individualsarjay matanguihan100% (2)

- Module - 1 Basic Concepts.Document11 pagesModule - 1 Basic Concepts.Dimple JainPas encore d'évaluation

- Obama Tax Fairness PlanDocument4 pagesObama Tax Fairness PlanJoe CuraPas encore d'évaluation

- Report of Receipts and Disbursements: FEC Form 3Document95 pagesReport of Receipts and Disbursements: FEC Form 3Jon RalstonPas encore d'évaluation

- Taxation Law Bar Review Lecture NotesDocument3 pagesTaxation Law Bar Review Lecture NotesIra AgtingPas encore d'évaluation