Vous aimerez peut-être aussi

- TDS PDFDocument71 pagesTDS PDFJ.S. RATHOD67% (3)

- Electronic Payment SystemDocument46 pagesElectronic Payment SystemNakul Chawda100% (2)

- Electronic Payment SystemDocument25 pagesElectronic Payment SystemTarun Garg100% (1)

- Mr. Abhishek Gupta Abhiraj Malik 1702517 CSE - 5 (A1)Document40 pagesMr. Abhishek Gupta Abhiraj Malik 1702517 CSE - 5 (A1)Yash KwatraPas encore d'évaluation

- Import Process Flow-FCLDocument9 pagesImport Process Flow-FCLZafani YaacobPas encore d'évaluation

- Practical Q Bcom Programme III YrDocument11 pagesPractical Q Bcom Programme III YrPhung Huyen NgaPas encore d'évaluation

- Electronic Payment System111Document43 pagesElectronic Payment System111negirakes100% (1)

- Epayment SeminarDocument5 pagesEpayment Seminardheeraj_ddPas encore d'évaluation

- Bank Terms RDocument16 pagesBank Terms RVinay SonkhiyaPas encore d'évaluation

- Project Report Atm SystemDocument11 pagesProject Report Atm SystemKendu BagraPas encore d'évaluation

- Innovation in Banking: A Review From The Point of View of Corporate GovernanceDocument35 pagesInnovation in Banking: A Review From The Point of View of Corporate GovernanceMj PorcionculaPas encore d'évaluation

- Bhavik BlackbookDocument29 pagesBhavik BlackbookBhavik khairPas encore d'évaluation

- Cheque Truncation ProjectDocument26 pagesCheque Truncation ProjectReema Dawra0% (1)

- Emergence of Payment Systems in The Age of Electronic Commerce: The State of ArtDocument6 pagesEmergence of Payment Systems in The Age of Electronic Commerce: The State of ArtThulhaj ParveenPas encore d'évaluation

- Procurement CardDocument5 pagesProcurement CardGuhanadh Padarthy100% (1)

- Electronic Payment SystemDocument23 pagesElectronic Payment SystemBiswajit Chowdhury100% (2)

- Overview of Mobile Payments WhitepaperDocument14 pagesOverview of Mobile Payments WhitepapertderuvoPas encore d'évaluation

- Internet Payment & BankingDocument30 pagesInternet Payment & BankingPreeti RanaPas encore d'évaluation

- 8.3. Developing Use-Case DiagramsDocument8 pages8.3. Developing Use-Case DiagramsDeep AdhikaryPas encore d'évaluation

- Online Payment ProtocolsDocument29 pagesOnline Payment ProtocolsKartik GuptaPas encore d'évaluation

- Unit-III - E-Commerce and Its ApplicationDocument90 pagesUnit-III - E-Commerce and Its ApplicationVasa VijayPas encore d'évaluation

- Design of A National Identity Card SystemDocument50 pagesDesign of A National Identity Card SystemDinomarshal PezumPas encore d'évaluation

- Functioning & Usage of Electric Money Transfers-Rtgs, Neft, Imps, UpiDocument18 pagesFunctioning & Usage of Electric Money Transfers-Rtgs, Neft, Imps, UpikanikaPas encore d'évaluation

- ATM Test Plan DocumentDocument8 pagesATM Test Plan Documentangel13419890% (2)

- P2P-Paid: A Peer-to-Peer Wireless Payment SystemDocument10 pagesP2P-Paid: A Peer-to-Peer Wireless Payment SystemValdi Adrian AbrarPas encore d'évaluation

- Citizen Card System AbstractDocument4 pagesCitizen Card System Abstractarv_ku100% (1)

- Mobilink-Network Partial List of PartnersDocument5 pagesMobilink-Network Partial List of PartnersEksdiPas encore d'évaluation

- EMTM 553: E-Commerce Systems: Lecture 8: Electronic Payment SystemsDocument59 pagesEMTM 553: E-Commerce Systems: Lecture 8: Electronic Payment SystemsD Attitude KidPas encore d'évaluation

- Electronic Commerce and E-Wallet: Abhay UpadhayayaDocument5 pagesElectronic Commerce and E-Wallet: Abhay UpadhayayaSavitha VjPas encore d'évaluation

- Mobile PaymentsDocument36 pagesMobile Paymentsadnan67Pas encore d'évaluation

- All About Swift Software in BanksDocument15 pagesAll About Swift Software in BanksDeepthi RavichandhranPas encore d'évaluation

- Rashmi Sharma - 11505Document29 pagesRashmi Sharma - 11505Kanika TandonPas encore d'évaluation

- Bank Account Management SystemDocument45 pagesBank Account Management SystemShivani Pandey ShilpiPas encore d'évaluation

- Visa 20100723Document28 pagesVisa 20100723brineshrimpPas encore d'évaluation

- Criminal MGMT SynopsisDocument6 pagesCriminal MGMT Synopsisnayakrahu100% (1)

- About e WalletDocument8 pagesAbout e WalletSavitha VjPas encore d'évaluation

- Payment SystemsDocument7 pagesPayment SystemsGanesh ShankarPas encore d'évaluation

- Banking Services Online and OfflineDocument39 pagesBanking Services Online and Offlineonkarskulkarni0% (1)

- ATM Case Study, Part 1: Object-Oriented Design With The UMLDocument46 pagesATM Case Study, Part 1: Object-Oriented Design With The UMLVaidehiBaporikarPas encore d'évaluation

- A Convenient Method For Securely Managing Passwords: J. Alex Halderman Brent Waters Edward W. FeltenDocument9 pagesA Convenient Method For Securely Managing Passwords: J. Alex Halderman Brent Waters Edward W. FeltenOanaMarcPas encore d'évaluation

- Internet Download Manager A Complete Guide - 2019 EditionD'EverandInternet Download Manager A Complete Guide - 2019 EditionPas encore d'évaluation

- Electronic Payment SystemDocument28 pagesElectronic Payment Systemnehapaspuleti4891100% (1)

- Banking Awareness ImportantDocument30 pagesBanking Awareness ImportantThirrunavukkarasu R RPas encore d'évaluation

- XBRL All Case StudiesDocument13 pagesXBRL All Case StudiesSadar CmPas encore d'évaluation

- Source Code - MethodDocument9 pagesSource Code - Methodnlpatel22Pas encore d'évaluation

- E Frauds in BankingDocument5 pagesE Frauds in BankingRajivPas encore d'évaluation

- Banking SoftwaresDocument3 pagesBanking Softwaressri3680Pas encore d'évaluation

- Syntax-Directed TranslationDocument38 pagesSyntax-Directed TranslationKristy SotoPas encore d'évaluation

- The Imperative of Online Payment System in Developing CountriesDocument7 pagesThe Imperative of Online Payment System in Developing CountriesInternational Journal of Innovative Science and Research TechnologyPas encore d'évaluation

- Industrial Training Report: " Twitter Bot "Document39 pagesIndustrial Training Report: " Twitter Bot "Kid On wayPas encore d'évaluation

- Commercial BankDocument7 pagesCommercial BankAnonymous lVpFnX3Pas encore d'évaluation

- Black BookDocument45 pagesBlack BookSagar Patil100% (1)

- Central Bank Digital CurrencyDocument28 pagesCentral Bank Digital CurrencyBlack JewPas encore d'évaluation

- Tecnology in BankingDocument6 pagesTecnology in BankingShakthi RaghaviPas encore d'évaluation

- Internet Banking 2Document82 pagesInternet Banking 2Sagar KavaPas encore d'évaluation

- Requirements Statement For Example ATM SystemDocument2 pagesRequirements Statement For Example ATM Systemsushil_programmerPas encore d'évaluation

- Electronic Payment SystemsDocument8 pagesElectronic Payment SystemsAbhishek NayakPas encore d'évaluation

- BIT 4107 Mobile Application DevelopmentDocument136 pagesBIT 4107 Mobile Application DevelopmentVictor NyanumbaPas encore d'évaluation

- AtmDocument31 pagesAtmAnonymous CbJxrs0% (2)

- E-Payment System On E-Commerce in India: Karamjeet Kaur, Dr. Ashutosh PathakDocument9 pagesE-Payment System On E-Commerce in India: Karamjeet Kaur, Dr. Ashutosh Pathakdharshinee1961Pas encore d'évaluation

- E Comm - Unit 3Document8 pagesE Comm - Unit 3prashanttendolkarPas encore d'évaluation

- Electronic Payment SystemDocument20 pagesElectronic Payment SystemTsz Yeung YipPas encore d'évaluation

- Chapter-6 Electronic Payment PDFDocument40 pagesChapter-6 Electronic Payment PDFSuman BhandariPas encore d'évaluation

- Book 1Document4 pagesBook 1Shafique Ahmed ArainPas encore d'évaluation

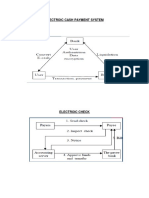

- Electroic Cash Payment SystemDocument1 pageElectroic Cash Payment SystemShafique Ahmed ArainPas encore d'évaluation

- Advanced Finan Accou Final - Shafique BR546647Document13 pagesAdvanced Finan Accou Final - Shafique BR546647Shafique Ahmed ArainPas encore d'évaluation

- Entrepreneurship Presentation - Shafique BR546647Document11 pagesEntrepreneurship Presentation - Shafique BR546647Shafique Ahmed ArainPas encore d'évaluation

- E Commerce 2nd Assign Ok (Repaired)Document19 pagesE Commerce 2nd Assign Ok (Repaired)Shafique Ahmed ArainPas encore d'évaluation

- E Commerce 2nd Assign Ok (Repaired)Document19 pagesE Commerce 2nd Assign Ok (Repaired)Shafique Ahmed ArainPas encore d'évaluation

- APA Format Q 5Document21 pagesAPA Format Q 5Shafique Ahmed ArainPas encore d'évaluation

- APA Format Q 5Document21 pagesAPA Format Q 5Shafique Ahmed ArainPas encore d'évaluation

- Accounts For Insurance Companies: 1. Title PageDocument17 pagesAccounts For Insurance Companies: 1. Title PageShafique Ahmed ArainPas encore d'évaluation

- Q No 2 PDFDocument2 pagesQ No 2 PDFShafique Ahmed ArainPas encore d'évaluation

- Direct Marketing PDFDocument33 pagesDirect Marketing PDFShafique Ahmed ArainPas encore d'évaluation

- Mba Thapar University Fee Structure 2019 21-18-02 2019 New 2Document5 pagesMba Thapar University Fee Structure 2019 21-18-02 2019 New 2ManyataChauhanPas encore d'évaluation

- Special Journals - Quiz 36Document8 pagesSpecial Journals - Quiz 36Joana TrinidadPas encore d'évaluation

- Personal Computer Case Study SolutionDocument3 pagesPersonal Computer Case Study Solutionfaraz ahmad khanPas encore d'évaluation

- CS Executive Old Paper 4 Tax Laws and Practice SA V0.3Document33 pagesCS Executive Old Paper 4 Tax Laws and Practice SA V0.3Raunak AgarwalPas encore d'évaluation

- E-Way Bill: Government of IndiaDocument1 pageE-Way Bill: Government of IndiaVIVEK N KHAKHARAPas encore d'évaluation

- Tax 2 Finals (Remedies To Cta)Document27 pagesTax 2 Finals (Remedies To Cta)Athena SalasPas encore d'évaluation

- B2B Ecostore - Billing Letter - January 2020 TEMPLATEDocument3 pagesB2B Ecostore - Billing Letter - January 2020 TEMPLATEkevin echiverriPas encore d'évaluation

- Plastic MoneyDocument11 pagesPlastic MoneyDILIP JAINPas encore d'évaluation

- Law-Of-Negotiable-Instruments - Abrham YohannesDocument171 pagesLaw-Of-Negotiable-Instruments - Abrham YohannesJøñë ÊphrèmPas encore d'évaluation

- Monitor BillDocument1 pageMonitor BillGulf JobsPas encore d'évaluation

- Contractor BillDocument4 pagesContractor BillMuhammad RiazPas encore d'évaluation

- North South University: ID# 181 1530 030 DegreeDocument1 pageNorth South University: ID# 181 1530 030 DegreeRashaduzzaman RiadPas encore d'évaluation

- PopipDocument2 pagesPopipRaj Kumar KPas encore d'évaluation

- Policy Details: Page 1 of 5Document5 pagesPolicy Details: Page 1 of 5pradeep s gillPas encore d'évaluation

- Tax Planning V/S Tax Management: Dr. Anindhya TiwariDocument18 pagesTax Planning V/S Tax Management: Dr. Anindhya TiwariJAGDISHWAR KUTIYALPas encore d'évaluation

- Sbi SaralDocument12 pagesSbi Saralmevrick_guyPas encore d'évaluation

- VAT Summary of Changes Under The TRAIN LawDocument4 pagesVAT Summary of Changes Under The TRAIN LawrafastilPas encore d'évaluation

- BIR Returns SummaryDocument7 pagesBIR Returns SummarySanta Dela Cruz NaluzPas encore d'évaluation

- Transitioning Into Sales Tax and Service TaxDocument6 pagesTransitioning Into Sales Tax and Service Taxkok kuan wongPas encore d'évaluation

- Slip Gaji Aril PDFDocument9 pagesSlip Gaji Aril PDFmuhidinPas encore d'évaluation

- EBS 122 Cum RCD FinanceDocument106 pagesEBS 122 Cum RCD FinanceMd MuzaffarPas encore d'évaluation

- Confirmation1Document2 pagesConfirmation1Ignas Getsema Agasi SuryaPas encore d'évaluation

- Accounting and Payroll Specialist Study TestDocument1 pageAccounting and Payroll Specialist Study TestSherlyana GunawanPas encore d'évaluation

- Statement: Please Note When Making Payment To Us Our Bank Account Details Remain UnchangedDocument1 pageStatement: Please Note When Making Payment To Us Our Bank Account Details Remain UnchangedDebyPas encore d'évaluation

- 2022 AllSlipsDocument3 pages2022 AllSlipsAshley LehmanPas encore d'évaluation

- Solved Latesha A Single Taxpayer Had The Following Income and DeductionsDocument1 pageSolved Latesha A Single Taxpayer Had The Following Income and DeductionsAnbu jaromiaPas encore d'évaluation

- BSP Memorandum No. M-2018-013Document2 pagesBSP Memorandum No. M-2018-013supremo10Pas encore d'évaluation