Vous aimerez peut-être aussi

- Chapter 6 Audit in Automated EnvironmentDocument16 pagesChapter 6 Audit in Automated Environmentchananakartik1Pas encore d'évaluation

- CH - 4 - Risk Assessment and Internal ControlDocument46 pagesCH - 4 - Risk Assessment and Internal ControlEkansh AgarwalPas encore d'évaluation

- 01 C2 Audit Strategy, Audit PlanningDocument5 pages01 C2 Audit Strategy, Audit PlanningRamesh AgarwalPas encore d'évaluation

- CH - 2 PDFDocument29 pagesCH - 2 PDFSonu SawantPas encore d'évaluation

- Audit 2021 Full BookDocument404 pagesAudit 2021 Full Bookashwani7789Pas encore d'évaluation

- CA Inter Audit For Nov 2020 by Neeraj Arora PDFDocument383 pagesCA Inter Audit For Nov 2020 by Neeraj Arora PDFGokarakonda Sandeep71% (7)

- CA Ipcc Audit m21 Book FVDocument405 pagesCA Ipcc Audit m21 Book FVKC XitizPas encore d'évaluation

- Meaning of PervasiveDocument4 pagesMeaning of PervasiveKetan BohraPas encore d'évaluation

- CH - 3 PDFDocument41 pagesCH - 3 PDFSonu SawantPas encore d'évaluation

- 03 C3 Audit Documentation and Audit EvidenceDocument6 pages03 C3 Audit Documentation and Audit EvidenceRamesh AgarwalPas encore d'évaluation

- 01 Introduction & Chapter-1Document45 pages01 Introduction & Chapter-1Ritam chaturvediPas encore d'évaluation

- Bank AuditDocument10 pagesBank AuditUrvi MishraPas encore d'évaluation

- Certifiable Software Applications 2: Support ProcessesD'EverandCertifiable Software Applications 2: Support ProcessesPas encore d'évaluation

- Basics Audit Neeraj AroraDocument22 pagesBasics Audit Neeraj Aroradaniya manojPas encore d'évaluation

- Complex IT Environment Security A Complete Guide - 2019 EditionD'EverandComplex IT Environment Security A Complete Guide - 2019 EditionPas encore d'évaluation

- IT Asset Management Security A Complete Guide - 2020 EditionD'EverandIT Asset Management Security A Complete Guide - 2020 EditionPas encore d'évaluation

- Sa 260Document5 pagesSa 260vishal mishraPas encore d'évaluation

- IT Environment Security A Complete Guide - 2019 EditionD'EverandIT Environment Security A Complete Guide - 2019 EditionPas encore d'évaluation

- Security IoT Containers A Complete Guide - 2019 EditionD'EverandSecurity IoT Containers A Complete Guide - 2019 EditionPas encore d'évaluation

- IT Asset Management ITAM A Complete Guide - 2020 EditionD'EverandIT Asset Management ITAM A Complete Guide - 2020 EditionPas encore d'évaluation

- SA 220 - Quality Control For An Audit of Financial StatementsDocument8 pagesSA 220 - Quality Control For An Audit of Financial StatementsmohanPas encore d'évaluation

- Java™ Programming: A Complete Project Lifecycle GuideD'EverandJava™ Programming: A Complete Project Lifecycle GuidePas encore d'évaluation

- CompTIA CASP+ CAS-004 Exam Guide: A-Z of Advanced Cybersecurity Concepts, Mock Exams, Real-world Scenarios with Expert Tips (English Edition)D'EverandCompTIA CASP+ CAS-004 Exam Guide: A-Z of Advanced Cybersecurity Concepts, Mock Exams, Real-world Scenarios with Expert Tips (English Edition)Pas encore d'évaluation

- IP Multimedia Subsystem A Complete Guide - 2020 EditionD'EverandIP Multimedia Subsystem A Complete Guide - 2020 EditionPas encore d'évaluation

- IT Asset Management System A Complete Guide - 2020 EditionD'EverandIT Asset Management System A Complete Guide - 2020 EditionPas encore d'évaluation

- CH 3Document27 pagesCH 3PRINCE SULTANIA Umeschandra CollegePas encore d'évaluation

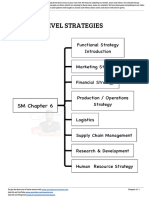

- Inter SM Functional Level Strategies Notes PDFDocument16 pagesInter SM Functional Level Strategies Notes PDFDr MG BIJU MUKUNDANPas encore d'évaluation

- Security Of Computer Systems A Complete Guide - 2020 EditionD'EverandSecurity Of Computer Systems A Complete Guide - 2020 EditionPas encore d'évaluation

- Due Diligence NotesDocument5 pagesDue Diligence NotesRashmi AminPas encore d'évaluation

- CH - 8 - Analytical Procedure (Sa 520)Document10 pagesCH - 8 - Analytical Procedure (Sa 520)Ekansh AgarwalPas encore d'évaluation

- Chapter 15 SummaryDocument5 pagesChapter 15 Summaryapi-638322504Pas encore d'évaluation

- The First Security Engineer's 100-Day ChecklistDocument21 pagesThe First Security Engineer's 100-Day ChecklistIvan PopovPas encore d'évaluation

- CompTIA A+ Certification All-in-One Exam Guide: How to pass the exam without over studying!D'EverandCompTIA A+ Certification All-in-One Exam Guide: How to pass the exam without over studying!Évaluation : 1 sur 5 étoiles1/5 (3)

- Creative Youth Agency PlatformDocument10 pagesCreative Youth Agency PlatformWagaanaAlexPas encore d'évaluation

- IT Security Management A Complete Guide - 2020 EditionD'EverandIT Security Management A Complete Guide - 2020 EditionPas encore d'évaluation

- SEQA Session 6 Software ReliabilityDocument107 pagesSEQA Session 6 Software Reliability14Sarthak KarkeraPas encore d'évaluation

- Auditing Information Systems: Enhancing Performance of the EnterpriseD'EverandAuditing Information Systems: Enhancing Performance of the EnterprisePas encore d'évaluation

- Attendance Management System PDFDocument69 pagesAttendance Management System PDFSingh JanmejayPas encore d'évaluation

- Software System Safety A Complete Guide - 2020 EditionD'EverandSoftware System Safety A Complete Guide - 2020 EditionPas encore d'évaluation

- Nagios Tutorial PDFDocument38 pagesNagios Tutorial PDFBishnu BashyalPas encore d'évaluation

- Placement ConsultancyDocument69 pagesPlacement ConsultancymanikmathiPas encore d'évaluation

- SM Notes Neeraj Arora Sir PDFDocument142 pagesSM Notes Neeraj Arora Sir PDFAnjali khanchandani100% (7)

- CSC577 - Chapter 1 - Introduction To SEDocument35 pagesCSC577 - Chapter 1 - Introduction To SEstar primePas encore d'évaluation

- Caro 21Document15 pagesCaro 21ashwani7789Pas encore d'évaluation

- Regional Mathematical Olympiad-2017 Results Region - Mumbai: Sr. No PRMO Roll NoDocument1 pageRegional Mathematical Olympiad-2017 Results Region - Mumbai: Sr. No PRMO Roll NoMuraliPas encore d'évaluation

- Problem 5: - On Side AC of Circle of Point A Is Defined Similarly. Prove That ADocument1 pageProblem 5: - On Side AC of Circle of Point A Is Defined Similarly. Prove That AMuraliPas encore d'évaluation

- Class Xii Second Preboard PaperDocument6 pagesClass Xii Second Preboard PaperMuraliPas encore d'évaluation

- Solution of Triangle: Sine RuleDocument41 pagesSolution of Triangle: Sine RuleMuraliPas encore d'évaluation

- 520386Document3 pages520386MuraliPas encore d'évaluation

- 588208Document6 pages588208MuraliPas encore d'évaluation

- Functional Equations: Olympiad CornerDocument6 pagesFunctional Equations: Olympiad CornerMuraliPas encore d'évaluation

- Paper - 6: Auditing and Assurance: © The Institute of Chartered Accountants of IndiaDocument14 pagesPaper - 6: Auditing and Assurance: © The Institute of Chartered Accountants of IndiaMuraliPas encore d'évaluation

- Regional Coordinators 2018Document8 pagesRegional Coordinators 2018MuraliPas encore d'évaluation

- Monthly Corporate Action Tracker: - Dossier of Key Corporate Actions in October, 2018Document20 pagesMonthly Corporate Action Tracker: - Dossier of Key Corporate Actions in October, 2018MuraliPas encore d'évaluation

- Weekly Olympiad 1 PDFDocument1 pageWeekly Olympiad 1 PDFMuraliPas encore d'évaluation

- Sample OMR Sheet Marking PDFDocument1 pageSample OMR Sheet Marking PDFMuraliPas encore d'évaluation

- RMO 2010 Results Telangana PDFDocument3 pagesRMO 2010 Results Telangana PDFMuraliPas encore d'évaluation

- The Pigeonhole Principle PDFDocument5 pagesThe Pigeonhole Principle PDFMurali100% (1)

- PS7 PDFDocument11 pagesPS7 PDFMuraliPas encore d'évaluation

- NMSF PRE RMO 2018 Registration Form PDFDocument2 pagesNMSF PRE RMO 2018 Registration Form PDFMuraliPas encore d'évaluation

- Cooperative Subordinate Special Rules PDFDocument20 pagesCooperative Subordinate Special Rules PDFRathnakraja50% (2)

- Audit of The Water Sharing Plan For The Barwon-Darling Unregulated and Alluvial Water Sources 2012Document70 pagesAudit of The Water Sharing Plan For The Barwon-Darling Unregulated and Alluvial Water Sources 2012The Sydney Morning HeraldPas encore d'évaluation

- Internal Audit Exam For Auditors Getting Ready To Be QualifiedDocument6 pagesInternal Audit Exam For Auditors Getting Ready To Be QualifiedYahya Chiguer75% (4)

- Iso Iec 17020 2012 For Inspection BodiesDocument15 pagesIso Iec 17020 2012 For Inspection Bodieswalid walidPas encore d'évaluation

- Swiggy - Data Protection Implementation Timelines - Fiduciaries QuestionnaireDocument6 pagesSwiggy - Data Protection Implementation Timelines - Fiduciaries QuestionnaireAditya RoyPas encore d'évaluation

- ACCT402 Auditing and Assurance Concepts and Application 1Document9 pagesACCT402 Auditing and Assurance Concepts and Application 1Miles SantosPas encore d'évaluation

- Auditing in CIS EnvironmentBIT006WFAsystemssecurityDocument28 pagesAuditing in CIS EnvironmentBIT006WFAsystemssecurityJohn David Alfred EndicoPas encore d'évaluation

- Accounting 1 (Abm)Document7 pagesAccounting 1 (Abm)ALLIYAH JONES PAIRATPas encore d'évaluation

- HDFC FirstDocument20 pagesHDFC FirstTotmolPas encore d'évaluation

- Nonconformity ReportDocument3 pagesNonconformity ReportkumaravPas encore d'évaluation

- ISO-TS 16949 IQA Course MaterialDocument31 pagesISO-TS 16949 IQA Course Materialazadsingh1Pas encore d'évaluation

- Iso 22000 ManualDocument62 pagesIso 22000 ManualPrakash Rathod100% (7)

- ChallengesAuditingJune2006 PDFDocument16 pagesChallengesAuditingJune2006 PDFFachrurroziPas encore d'évaluation

- Auditors Independence 2Document10 pagesAuditors Independence 2bac22-pdzinkambaniPas encore d'évaluation

- ACCA F8 Audit & AssuranceDocument7 pagesACCA F8 Audit & AssuranceMingPas encore d'évaluation

- BSA Program ChecklistDocument4 pagesBSA Program ChecklistEunice Bawaan DominePas encore d'évaluation

- Chapter 6Document4 pagesChapter 6Huda tarekPas encore d'évaluation

- Trial Questions On AuditDocument4 pagesTrial Questions On AuditDaniel AmoahPas encore d'évaluation

- GMP Audit Checklist (As Per Who Guidelines) Page 1 of 32 Inspection Of: DateDocument32 pagesGMP Audit Checklist (As Per Who Guidelines) Page 1 of 32 Inspection Of: DateNavdeep Chaudhary100% (1)

- BBC History Magazine: MonthlyDocument4 pagesBBC History Magazine: MonthlyRichard HolguínPas encore d'évaluation

- Anti-Freeze Solutions For Sprinkler Systems in PDFDocument23 pagesAnti-Freeze Solutions For Sprinkler Systems in PDFhumshkhPas encore d'évaluation

- ACC451 Chapter 5 PowerpointDocument7 pagesACC451 Chapter 5 PowerpointMichael BurfordPas encore d'évaluation

- ILO Guidelines On Occupational Safety Systems PDFDocument130 pagesILO Guidelines On Occupational Safety Systems PDFVM100% (1)

- Activity Sheet - Module 3Document3 pagesActivity Sheet - Module 3Chris JacksonPas encore d'évaluation

- 2007 SOX 404 Testing Guidelines FINALDocument83 pages2007 SOX 404 Testing Guidelines FINALMichelle CheregoPas encore d'évaluation

- Risks Associated With DDPDocument16 pagesRisks Associated With DDPrachelPas encore d'évaluation

- Audit Under FiscalDocument108 pagesAudit Under FiscalAjay PanwarPas encore d'évaluation

- HULDocument32 pagesHULspraveenatlPas encore d'évaluation

- Audit Criteria: AC7122-P REV. BDocument10 pagesAudit Criteria: AC7122-P REV. BNamelezz ShadowwPas encore d'évaluation

- Presentation About NADCAPDocument22 pagesPresentation About NADCAPAnonymous gFcnQ4goPas encore d'évaluation