Vous aimerez peut-être aussi

- Tax Deduction at SourceDocument5 pagesTax Deduction at SourceSarayu BhardwajPas encore d'évaluation

- TDS TediousDocument30 pagesTDS Tediousxavier albuquerquePas encore d'évaluation

- Tax Deducted at SourceDocument29 pagesTax Deducted at SourceAmbar Pratik MishraPas encore d'évaluation

- Tax Deducted at Source - I: KPPM & AssociatesDocument63 pagesTax Deducted at Source - I: KPPM & AssociatesSaksham JoshiPas encore d'évaluation

- Tax Deducted at SourceDocument29 pagesTax Deducted at SourceChaitany Joshi0% (2)

- CA-Ashok-Mehta - PPT - Income TaxDocument88 pagesCA-Ashok-Mehta - PPT - Income TaxAbinash DasPas encore d'évaluation

- TDS 3Document16 pagesTDS 3payal AgrawalPas encore d'évaluation

- TDS Rates and Important DatesDocument3 pagesTDS Rates and Important DatesSadhvi BansalPas encore d'évaluation

- Tax Deducted at Source (TDS)Document7 pagesTax Deducted at Source (TDS)Rupali SinghPas encore d'évaluation

- Tax Deducted at Source: - Presented By: CA Prabhat Kumar Tandon Fca, Disa (Icai)Document20 pagesTax Deducted at Source: - Presented By: CA Prabhat Kumar Tandon Fca, Disa (Icai)shefalijais6491Pas encore d'évaluation

- For Tds On Non SalaryDocument39 pagesFor Tds On Non SalaryicahimanshumehtaPas encore d'évaluation

- Module 1 E - Filing of ReturnsDocument8 pagesModule 1 E - Filing of Returnsshivani singhPas encore d'évaluation

- Tax Deduction at SourceDocument62 pagesTax Deduction at SourcePallavisweet100% (1)

- Tax Deducted at SourceDocument10 pagesTax Deducted at SourcesreedevivcnPas encore d'évaluation

- Tds (Tax Deduction at Source) Presented byDocument17 pagesTds (Tax Deduction at Source) Presented byPooja JaiswalPas encore d'évaluation

- Introduction To TDS:-: Tax Deducted at SourceDocument3 pagesIntroduction To TDS:-: Tax Deducted at Sourcepadmanabha14Pas encore d'évaluation

- AX Educted at Ource - I: KPPM & AssociatesDocument67 pagesAX Educted at Ource - I: KPPM & AssociatesSaksham JoshiPas encore d'évaluation

- Tax Reform For Acceleration and Inclusion (Train) Republic Act No. 10963Document39 pagesTax Reform For Acceleration and Inclusion (Train) Republic Act No. 10963JAMIAH HULIPASPas encore d'évaluation

- All About Tax Deducted at Source (TDS) - Taxguru - inDocument11 pagesAll About Tax Deducted at Source (TDS) - Taxguru - inwaqtkeebaatein12Pas encore d'évaluation

- Tax Planning and ProceduresDocument32 pagesTax Planning and ProceduresSujata DongrePas encore d'évaluation

- TDS Rates and ReturnsDocument3 pagesTDS Rates and ReturnsKashishKumarPas encore d'évaluation

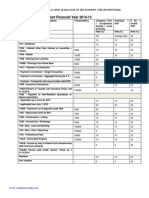

- TDS Rate Financial Year 13-14Document10 pagesTDS Rate Financial Year 13-14Heena AgrePas encore d'évaluation

- TDS - TCSDocument55 pagesTDS - TCSBeing HumanePas encore d'évaluation

- Tax Deducted at Source IMPORTANT POINTSDocument2 pagesTax Deducted at Source IMPORTANT POINTSnABSAMNPas encore d'évaluation

- Overview of TDS: by C.A. Manish JathliyaDocument21 pagesOverview of TDS: by C.A. Manish JathliyaHasan Babu KothaPas encore d'évaluation

- Tax Deduction at SourceDocument4 pagesTax Deduction at SourcevishalsidankarPas encore d'évaluation

- TDSDocument18 pagesTDSPratik NaikPas encore d'évaluation

- TDS TRS GST (2) 20211228151919Document38 pagesTDS TRS GST (2) 20211228151919Rishi PriyadarshiPas encore d'évaluation

- Tds Rate Chart Fy 2014-15 Ay 2015-16Document26 pagesTds Rate Chart Fy 2014-15 Ay 2015-16shivashankari86Pas encore d'évaluation

- TDS - IT Act (09-03-2024)Document16 pagesTDS - IT Act (09-03-2024)santhoshgopal2005Pas encore d'évaluation

- TDS On SalariesDocument3 pagesTDS On SalariesSpUnky RohitPas encore d'évaluation

- Payment in Excess of Rs. 1,20,000/-Per Annum Payment in Excess of Rs. 1,20,000/ - Per AnnumDocument1 pagePayment in Excess of Rs. 1,20,000/-Per Annum Payment in Excess of Rs. 1,20,000/ - Per AnnumMadhan RajPas encore d'évaluation

- TDS Tax Deduction at Source: Prepared By: Visharad ShuklaDocument25 pagesTDS Tax Deduction at Source: Prepared By: Visharad ShuklaPriyanshi GandhiPas encore d'évaluation

- Tax Deducted at SourceDocument5 pagesTax Deducted at Sourceshubhra_jais6888Pas encore d'évaluation

- Section 194J: Fees For Professional or Technical ServicesDocument24 pagesSection 194J: Fees For Professional or Technical ServicesSAURABH TIBREWALPas encore d'évaluation

- Tax Reform For Acceleration and Inclusion (Train) Republic Act No. 10963Document47 pagesTax Reform For Acceleration and Inclusion (Train) Republic Act No. 10963Reiden VizcarraPas encore d'évaluation

- For Assessment Year - 2011 - 12 TDS Rates Chart Rates of TDS For Major Nature of Payments For The Financial Year 2010-11Document6 pagesFor Assessment Year - 2011 - 12 TDS Rates Chart Rates of TDS For Major Nature of Payments For The Financial Year 2010-11Savoir PenPas encore d'évaluation

- What Is Tax Deducted at SourceDocument6 pagesWhat Is Tax Deducted at SourcejdonPas encore d'évaluation

- SEMINAR ON NGAsDocument63 pagesSEMINAR ON NGAsHelen Joy Grijaldo JuelePas encore d'évaluation

- Tds - Tax Deducted at Source: FCA Vishal PoddarDocument22 pagesTds - Tax Deducted at Source: FCA Vishal PoddarPalak PunjabiPas encore d'évaluation

- Vivad Se Vishwas Tax 2025Document17 pagesVivad Se Vishwas Tax 2025Juzer JiruPas encore d'évaluation

- TDS Return FilingDocument34 pagesTDS Return FilingCABRAJJHAPas encore d'évaluation

- Unit 5 TaxDocument15 pagesUnit 5 TaxVijay GiriPas encore d'évaluation

- Ba0150030, Tax AssignmentDocument7 pagesBa0150030, Tax Assignmentprakhar bhattPas encore d'évaluation

- Tax Planning and ManagementDocument12 pagesTax Planning and Managementayushi chandraPas encore d'évaluation

- Tax Planning and Financial Management Decisions: CA Aarti PatkiDocument50 pagesTax Planning and Financial Management Decisions: CA Aarti PatkiRahul SinghPas encore d'évaluation

- TDS Practical Issues TARDocument31 pagesTDS Practical Issues TARHemanshu SolankiPas encore d'évaluation

- Overview of TDS: Who Shall Deduct Tax at Source?Document37 pagesOverview of TDS: Who Shall Deduct Tax at Source?pradeep_ravi_7Pas encore d'évaluation

- Tax UpdatesDocument79 pagesTax UpdatesFreijiah SonPas encore d'évaluation

- The Rigours of TDS - An OverviewDocument31 pagesThe Rigours of TDS - An OverviewShaleenPatniPas encore d'évaluation

- Employment Vs HiringDocument29 pagesEmployment Vs Hiringnaulele robertPas encore d'évaluation

- Tax Deducted at Source UnitDocument13 pagesTax Deducted at Source Unitsatyanarayan dashPas encore d'évaluation

- All About TDSDocument10 pagesAll About TDSAnimesh Kumar TilakPas encore d'évaluation

- Intro of TdsDocument6 pagesIntro of Tdsshivani singhPas encore d'évaluation

- TDS & TCSDocument3 pagesTDS & TCSRajashree DasPas encore d'évaluation

- Monthly Percentage Tax ReturnDocument3 pagesMonthly Percentage Tax ReturnAu B ReyPas encore d'évaluation

- Tds Rate Chart Fy 2014-15 Ay 2015-16 Tds Due Dates #SimpletaxindiaDocument11 pagesTds Rate Chart Fy 2014-15 Ay 2015-16 Tds Due Dates #Simpletaxindiashivashankari86Pas encore d'évaluation

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsD'Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsPas encore d'évaluation

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeD'Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeÉvaluation : 1 sur 5 étoiles1/5 (1)

- 1040 Exam Prep: Module I: The Form 1040 FormulaD'Everand1040 Exam Prep: Module I: The Form 1040 FormulaÉvaluation : 1 sur 5 étoiles1/5 (3)

- 01Document2 pages01ishtee894Pas encore d'évaluation

- 1234449Document19 pages1234449Jade MarkPas encore d'évaluation

- NowDocument14 pagesNowYugant RajPas encore d'évaluation

- MCB-AH Corp Presentation Sept 12 PDFDocument30 pagesMCB-AH Corp Presentation Sept 12 PDFlordraiPas encore d'évaluation

- Submitted To: DR - Shokat Malik (HOD) : AssignmentDocument8 pagesSubmitted To: DR - Shokat Malik (HOD) : AssignmentAtia KhalidPas encore d'évaluation

- Effect of Naira Devaluation On Small and Medium Scale Enterprises in Nigeria 1Document68 pagesEffect of Naira Devaluation On Small and Medium Scale Enterprises in Nigeria 1Kapeel Leemani100% (1)

- Micro Financing HistoryDocument62 pagesMicro Financing HistoryVincent KonoteyPas encore d'évaluation

- ARRA Realty Copr vs. Guaranty Corp Insurance AgencyDocument22 pagesARRA Realty Copr vs. Guaranty Corp Insurance Agencyshirlyn cuyongPas encore d'évaluation

- RELATIVE SYNONYMS & ANTONYMS SHORTCUTS PREPARATION IBPS EXAM PAPERS - HTTP - Ibps - Ibpsexams PDFDocument19 pagesRELATIVE SYNONYMS & ANTONYMS SHORTCUTS PREPARATION IBPS EXAM PAPERS - HTTP - Ibps - Ibpsexams PDFshalinicse27Pas encore d'évaluation

- Risk Management Presentation January 14 2013Document206 pagesRisk Management Presentation January 14 2013George LekatisPas encore d'évaluation

- 633862581-21 Solution (ArtnershipDocument36 pages633862581-21 Solution (ArtnershipPhilip K BugaPas encore d'évaluation

- PDF BahramDocument3 pagesPDF Bahramxfzm99mr8rPas encore d'évaluation

- Standby Letter Credit ExplanationDocument8 pagesStandby Letter Credit Explanationanujanair3146100% (1)

- Negotiable Instruments Act 2034 1977Document26 pagesNegotiable Instruments Act 2034 1977Ashish Singh NegiPas encore d'évaluation

- E-Internship Report 1Document13 pagesE-Internship Report 1Avani TomarPas encore d'évaluation

- Security Bank: History of The CompanyDocument6 pagesSecurity Bank: History of The CompanyKathlyn Cher SarmientoPas encore d'évaluation

- Valuation Objective QuestionsDocument13 pagesValuation Objective QuestionsRubina Hannure75% (8)

- 39 Caro 2003 ChecklistDocument13 pages39 Caro 2003 ChecklistAnkushKumarPas encore d'évaluation

- The Surat Dist. Co-Op BankDocument94 pagesThe Surat Dist. Co-Op BankVijay Gohil0% (3)

- Annexure I Project Details DateDocument4 pagesAnnexure I Project Details DateAshish SinghaniaPas encore d'évaluation

- A Project Report: On Study of Microfinance (Self-Help Groups)Document7 pagesA Project Report: On Study of Microfinance (Self-Help Groups)Rupal Rohan DalalPas encore d'évaluation

- Investigacion Del Deutsche BankDocument14 pagesInvestigacion Del Deutsche BankJaumePas encore d'évaluation

- Law of Banking and Security: Dr. Zulkifli HasanDocument25 pagesLaw of Banking and Security: Dr. Zulkifli HasanQuofi SeliPas encore d'évaluation

- SMC ProjectDocument34 pagesSMC Projectpiyush solankiPas encore d'évaluation

- 1 Huang Xingren 79m Signed CpuDocument4 pages1 Huang Xingren 79m Signed CpuМухаммед АлиPas encore d'évaluation

- New Text DocumentDocument3 pagesNew Text Documentngtkoanh100% (1)

- Problem 3Document3 pagesProblem 3Joyce GijsenPas encore d'évaluation

- Dao Heng Bank Inc. Etc vs. Spouse Laigo DigestDocument1 pageDao Heng Bank Inc. Etc vs. Spouse Laigo DigestLuz Celine CabadingPas encore d'évaluation

- FAQDocument58 pagesFAQvivekluvinPas encore d'évaluation

- Negotiable Instrument ReviewerDocument21 pagesNegotiable Instrument ReviewerThor83% (6)